Final Expense Benefits' Guide To Buying Burial Insurance For Your Parents

“Can I buy life insurance for my parents?”

The answer is yes, you can buy life insurance for your parents. In fact, it’s a very simple process and adds almost nothing to your monthly expenses.

Depending on the coverage amount, plan, and type of coverage, you could insure your parents with Burial Insurance for just $22/month in as little as 72 hours.

Read on to see if buying Burial Insurance for your parents is going to be the right choice for you and your family.

What is Burial Insurance?

First of all, Burial Insurance exists as a whole life insurance policy meant to aid in the ability of your family to cover any end-of-life expenses, such as buying a burial plot, conducting a proper ceremony, cremation, what have you. You may have heard terms like Final Expense Insurance, Burial Insurance, Funeral Insurance, Preneed Insurance, etc., all existing as a synonym for Burial Insurance.

It’s important to note that this form of insurance is not a standard whole life policy, but rather a specific fund meant to mitigate funeral expenses and can successfully coexist with any other standard whole life insurance policy. There is no actual restriction regarding the Burial Insurance Policy, though, as the money is meant for funeral expenses but can be used at the discretion of the beneficiary for whatever they see fit. Generally, buying Burial Insurance for your Parents would cap out at a coverage amount of $50,000, but in some cases may provide more than this.

The focal point of this form of insurance is that it generates a large payout relatively quickly to the amount of time spent adhering to the policy and premiums. Another massive selling point in providing Burial Insurance for your parents would be that this form of insurance does not require a formal medical examination, further easing the process.

Do I Even Need Burial Insurance?

Although not as “crucial” as your average whole-life policy, we at Final Expense Benefits do recommend at least weighing your options when buying Burial Insurance for your parents. According to the National Funeral Directors Association (NFDA), the average cost of a funeral without a vault is just under $7,500, and with the vault rises to almost $9,000. The most extravagant funerals can get up to $20,000 as well.

Consider this, could you cover unexpected funeral expenses right this second? Would you remain in good financial health? If the answer is anything but a resounding yes, a Burial Insurance plan may be the right choice for you. This is why most Burial Insurance policies are by default set to $10,000 and serve as the premiere option when buying Burial Insurance for your parents.

Other alternatives include your everyday whole life policy, as well as preneed funeral insurance, although the latter isn’t highly recommended as Burial Insurance pays the coverage amount to a beneficiary rather than the funeral home itself. This could be important depending on the circumstances, as life is ever-changing and the funds may be deemed more necessary elsewhere.

Burial Insurance vs

Other Insurance Types

Burial Insurance is often more of a short-term policy vs your average Whole Life Insurance plan, which is not to say this is anything inherently negative. Burial Insurance is very similar to other like-minded policies. Burial Insurance aims to provide you with a stable amount of coverage, often times way less than that of a whole life insurance policy, with a minimized monthly premium as a result.

Simplified

Guaranteed

This form of Burial Insurance implies a guaranteed acceptance rate, regardless of your health status or other factors. The catch involves a higher premium, as well as an introductory period, usually remaining under 2 years before full policy benefit is fully provided. This policy also boasts the lowest relative proportion of monthly premium to coverage amount, justified by its guaranteed acceptance rate.

Pre-Need

The odd one out, this form of Burial Insurance exists almost as a contract between you and a funeral home provider, instructing the payout to go to said home in the case of untimely circumstances.

Does Burial Insurance Interfere with Medicaid or Medicare?

In short, No. Especially when you buy Burial Insurance for your parents in your name. In doing so, these assets are not even technically in the possession of your parents, as Burial Insurance does not hold a monetary value until the payout is being processed.

This isn’t to say the Burial Insurance you bought your parents isn’t worth what was stated, but rather the money is not able to be freely moved and transferred between accounts until the beneficiary receives his money.

This is important because Medicaid’s questions will attempt to infer any assets owned by your parents, as well as a transaction audit.

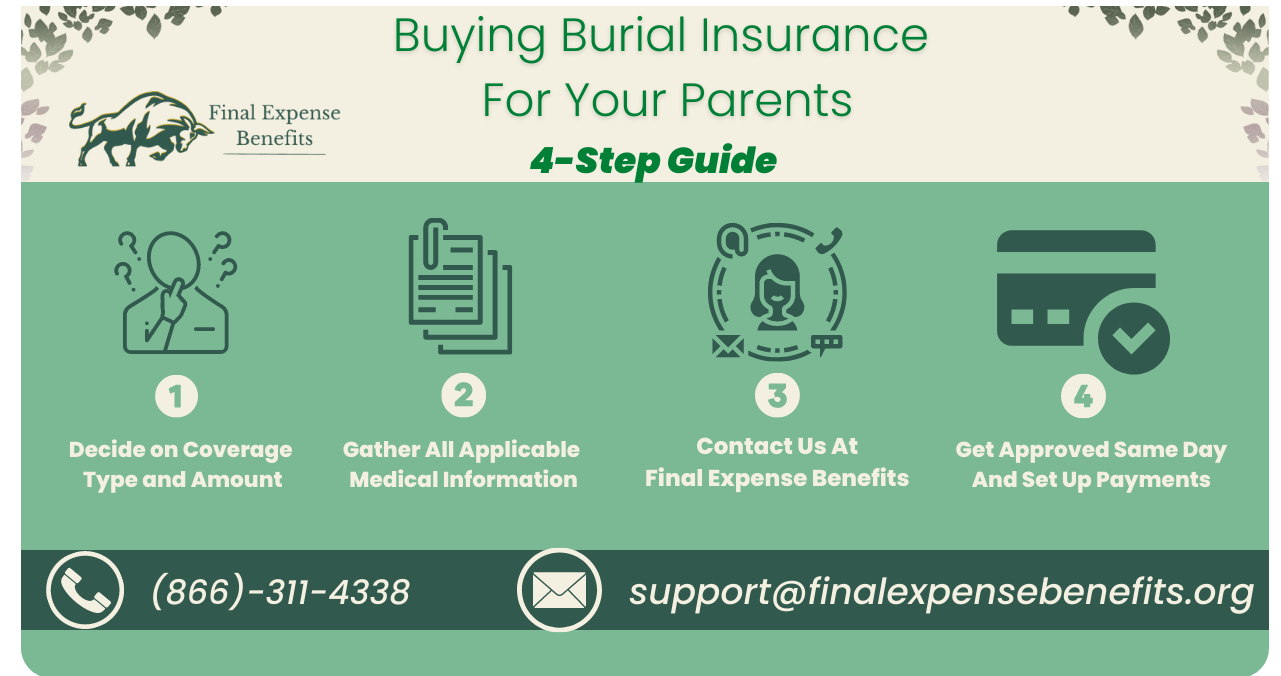

The Step by Step

Decide On Coverage

The first step when you buy Burial Insurance for your parents is to decide your desired coverage amount, usually beginning at $10,000, and maxing out at $50,000. This may be the step you decide to gather the opinion of whomever you decide to get the plan for, as the next steps require some background information from them.

Acquire Medical History

Debatably the most important part when buying Life Insurance for your parents, this is the step that determines your maximum coverage amount, premium, etc. A few of the key questions asked of you will involve said person’s medical history, list of medications, the presence of pre-existing conditions, height, weight, and tobacco use.

Contact us!

Once you have the appropriate documentation and plan set, we at Final Expense Benefits will work tirelessly to connect you with the coverage that best meets the needs of you and your beneficiaries. Our list of vendors contains over 51 different organizations, all ranked and diagnosed based on what coverage type they best fit.

Our number is (866)-311-4338, where agents are prepared to help M-F 9-5.

Get Approved

Once approved, set up automatic payments or whatever method you prefer… and done!

We recommend keeping a copy of any documentation in your records.

What Would My Premium Look Like?

When buying Burial Insurance for your parents, an extra premium is probably on the forefront of your mind. Can I handle this extra monthly expense? Is it even worth it? Can’t I just wait?

Well, we’re happy to tell you that if begun early enough, you can receive a Burial Insurance plan for your parents for as little as $22/month. Attached below is a sample table meant to illustrate your potential options when purchasing Burial Insurance for your parents.

Best Burial Insurance Rates for $10,000

| Company | 50 y/o Male | 50 y/o Female | 60 y/o Male | 60 y/o Female | 70 y/o Male | 70 y/o Female |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$51 |

$40 |

$73 |

$58 |

|

|

$39 |

$34 |

$52 |

$41 |

$86 |

$65 |

|

|

$30 |

$24 |

$43 |

$32 |

$74 |

$53 |

|

|

$36 |

$30 |

$47 |

$37 |

$81 |

$60 |

|

|

$55 |

$38 |

$68 |

$53 |

$106 |

$80 |

These figures were obtained from the NFDA and are estimates only. For a detailed quote, please contact an agent.

Burial Insurance Companies to Avoid

Colonial Penn

You may have come across advertising featuring the tagline, “pay just 9.95/month for coverage!” which isn’t inherently untrue, although this contains a few catches as one might expect. Colonial Penn doesn’t offer coverage in monetary amounts, but rather, in “units”. A singular unit adjusts its price as you age, beginning at just over $2,000 for a 50 yr old female, wherein that same female’s unit would adjust to just $620 at age 80, a significant decrease. The maximum coverage amount regarding units is 12 units with Colonial Penn, totaling around $25,000 for said 50 yr/old female mentioned above. The age range offered by Colonial Penn is 50-85 and is offered to all US states except NY. The waiting period for this Insurance Company is two years. This coverage does not expire, it only degrades.

Globe Life

Globe Life is a very prolific force in the Insurance world, existing for almost 75 years at this point. Globe Life offers a wide range of coverage, beginning at $5,000 and rounding off at $100,000 of maximum coverage. They also offer a wide range of coverage options, beginning with children’s whole life insurance all the way to Final Expense Insurance for seniors. Globe Life is available in all states and does not have a waiting period for their policy. The reason we recommend avoiding Globe Life, involves their incrementally increasing rates, introducing itself at a very low rate and slowly but surely gaining traction every five years when the price of the policy is increased. Globe Life policies also expire as soon as you reach age 90, providing beneficiaries with no stability if this age is outlived. This means, that the longer the policy exists, the more the threat looms that it will expire as well as the fact that you will continue to pay increasing rates, making this the most unappealing option when purchasing burial insurance for your parents.

AARP

Similar to Globe Life, AARP has remained a recognizable name in the industry for an extremely long time. The coverage offered by globe life depends, but the range is very wide overall, capping out at $100,000. AARP offers services in all 50 states, and usually does not contain a waiting period. Also similar to Globe Life, AARP policies expire at age 80, and if untimely experiences occur beneficiaries will receive nothing if death occurs after this age. This is an extremely unappealing option when purchasing burial insurance for your parents, as an expiration date provides nothing but extra stress.

Lincoln Heritage

Again, a very big name in the industry, Lincoln Heritage provides a very wide range of coverage options for any age. They offer services in all 50 US states and does not contain any policies that expire. Their coverage options are somewhat low, capping out at $35,000 for its maximum amount. Not a terrible idea if maximum coverage isn’t mandatory, although we recommend avoiding this company when buying Burial Insurance for your parents, as their overall rates exist at a much higher premium than almost all other Insurance Companies in the same jurisdiction.

What Not to Do When Applying for Burial Insurance

The only two inherent recommendations we have regarding burial insurance and your parents is to gain and uphold consent from those that you wish to insure, as well as gather your resources accordingly and weigh your options through proper research so that you may be prepared.

There are a plethora of insurance companies marketing their policies towards concerned individuals attempting to insure their parents, specifically to those that may not understand policy details or those that are impulsive in their purchases. Weighing your options, and comparing coverage details is going to be crucial in acquiring the most affordable and secure coverage option for you and your family.

If denied coverage, the MIB, or the Medical Information Bureau, may mark your claim status as previously denied and refuse to insure you. The way they infer this information is on the questionnaire, where you may be asked a y/n question regarding if you’ve applied for insurance in the last 12 months.

Conclusion

Overall, buying Life Insurance for your Parents has never been easier and barely puts a dent in your monthly expenses. Unless your assets completely outweigh any funeral expenses, we recommend purchasing Burial Insurance for your parents as soon as you reasonably see fit. There’s almost no overlap in coverage and only provides beneficiaries with a surplus in the event of any untimely circumstances.

If you are looking for insurance for yourself or a loved one, we at Final Expense Benefits partner with over 20 carriers such as:

Reduce the stress involved with life insurance and let us do all of the heavy lifting for you. You can reach us at 1 (866) 311-4338, and we’re open from 9-5, Monday through Friday.

Frequently Asked Questions

Can I insure both my mom and dad?

Absolutely, although a policy insures only one person at any time. Multiple policies may be taken out for both parents if requested.

Can I buy burial insurance for my parents without their consent?

Unfortunately, you cannot, as a signature as well as authorization is required. If forged, and found out by the insurance company, this is punishable by law and is a federal offense.

What's the best age to buy burial insurance for my parents?

We at Final Expense Benefits would argue that there isn’t a “best age” to begin purchasing Burial Insurance for your parents, but rather, as early as feasible possible regarding the circumstances. Aka, as soon as you feel compelled to do so.

Can I buy Burial Insurance for my 70 yr/old parent?

Generally, the cap for Burial Insurance is 85 but again, this depends on the aspects stated above. Some policies can even insure those that are 90 years old, although this is rare.