A Comprehensive Guide To Guaranteed Life Insurance

Updated on Mar 7, 2025 • 7 min read

Seniors can use guaranteed life insurance to ensure they have coverage, regardless of health concerns. In fact, many seniors believe guaranteed policies are the only way to ensure proper life insurance coverage, but this isn’t the case.

Also called guaranteed issue life insurance or guaranteed acceptance life insurance, guaranteed life insurance can be a great choice for seniors with major preexisting health concerns but may not be necessary for those in good health. Many final expense insurance providers’ underwriting guidelines have seniors in mind, so you could be eligible for a non-guaranteed policy, even with some preexisting medical conditions.

Final Expense Benefits is here to help you understand guaranteed life insurance and if it is necessary to cover your needs.

Contact us at (866) 786-0725 to learn more about your final expense insurance options or check our free online quoting tool for personalized pricing estimates.

What Is Guaranteed Life Insurance?

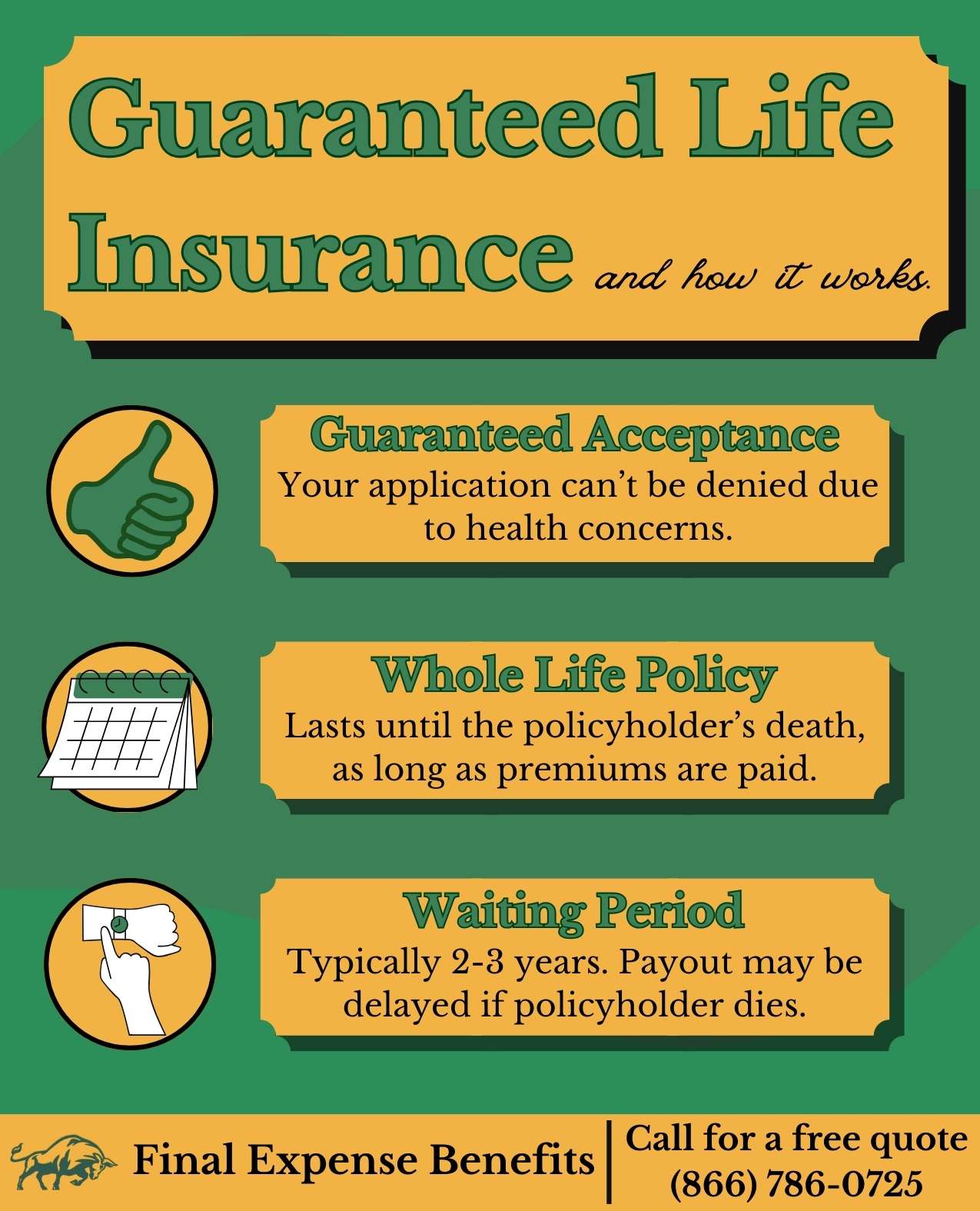

Guaranteed life insurance is a type of whole life insurance that doesn’t consider medical conditions when applicant eligibility is determined. Some providers refer to guaranteed life insurance as guaranteed issue life insurance or guaranteed acceptance life insurance.

Guaranteed life insurance can be a great choice for seniors in poor health. But it’s not the only choice.

Guaranteed plans often costs much more than others with underwriting, but just because a policy has health requirements doesn’t mean you won’t qualify. Many policies have underwriting requirements that are forgiving of health concerns.

In addition, guaranteed policies always have a waiting period of at least two years. This means your beneficiaries’ benefit payouts will be reduced until its end.

Guaranteed Life Insurance Waiting Period

Guaranteed acceptance life insurance policies always require a waiting period, typically two to three years. If the policyholder dies within this time, payouts are reduced. Some guaranteed issue life insurance policies only pay back a return of paid premiums plus a small percentage of interest.

Others pay a modified death benefit, which may only pay a percentage of the benefit over the waiting period’s first couple years. Each provider handles benefit payouts differently, so it’s a good idea to fully understand your provider’s payout structure.

This is a major benefit to working with a brokerage like Final Expense Benefits. Our expert agents can help you understand each provider’s payout policies and pick the best plan for your needs.

Unfortunately, every guaranteed plan has a mandatory waiting period. If you’re in dire health and want to get coverage, be proactive and secure it ahead of time.

But what should you do if you don’t want to worry about a waiting period? Can you get guaranteed life insurance with no waiting period?

Guaranteed Life Insurance with No Waiting Period

No insurer provides guaranteed life insurance with no waiting period. A major reason why guaranteed issue life insurance has a waiting period and a modified payout structure is to reduce the insurer’s risk in providing the policyholder coverage.

Policies without waiting periods generally manage this risk by restricting applicants by health condition. Insurers would have no way to manage risk on a policy that provides guaranteed coverage with no waiting period. Because of this, no such policies exist and likely never will.

Other Types of Guaranteed Life Insurance

If you’re looking for guaranteed coverage, you can only get whole life or final expense insurance. No providers offer guaranteed term life or universal life insurance. These types of life insurance often have stricter eligibility requirements, so insurers never offer them as guaranteed acceptance policies.

Guaranteed Life Insurance Pros & Cons

Pros

Applicants can’t be denied due to medical history

The major selling point of guaranteed issue life insurance is that applicants can’t be denied due to medical history. If you have a major preexisting health condition, guaranteed acceptance life insurance may be your only option.

Can buy small amounts of coverage for final expenses

We recommend final expense insurance because of its versatility. Guaranteed plans are often available with a death benefit as low as $2,000, so you can use these policies to fit your end-of-life expense plan to your needs.

Fast application process

Because underwriting processes are quick for guaranteed policies, many providers offer same-day approval. You can also apply for guaranteed acceptance life insurance plans directly with many providers, though it may still be best to go through a brokerage to ensure you get the best coverage at no extra cost.

No questionnaire or medical exam

Health concerns aren’t a part of underwriting guidelines for guaranteed policies, so applicants don’t need to worry about undergoing a medical exam or taking a health questionnaire.

Coverage available up to age 85

Some providers allow applicants up to age 85 for guaranteed plans. Just remember that rates for applicants at advanced ages can be quite expensive.

Cons

Waiting period

All guaranteed plans require a two to three-year waiting period before payouts.

Higher premiums

Because of the risk associated with insuring people with health concerns, guaranteed policies are always more expensive than a comparable non-guaranteed policy.

Low benefit maximums

Most guaranteed issue life insurance death benefits max out around $25,000 to $30,000, though some providers offer coverage up to $50,000.

Few riders

Life insurance riders can be a great way to customize your coverage, but providers rarely offer many rider options for guaranteed policies.

Who Should Use Guaranteed Life Insurance?

Guaranteed life insurance has several drawbacks, but it is still the best way to provide coverage to people with health concerns that preclude them from other life insurance options. Health concerns and conditions that would render you ineligible for any non-guaranteed coverage include:

- AIDS or HIV

- Alzheimer’s or Dementia

- Cancer or cancer treatment within last two years

- Currently in a hospital, nursing home, or nursing facility

- In a hospice care facility

- Undergoing home hospice / nursing care

- Alcohol or drug abuse within last two years (including treatment centers)

- Terminal illness of any kind

- Wheelchair-bound due to illness or disease

If you have any of these health concerns, guaranteed policies are likely your only option.

How Much Does Guaranteed Life Insurance Cost?

Guaranteed issue life insurance costs significantly higher than similar non-guaranteed options. Below are rates for guaranteed issue policies with $10,000 death benefits from some of our top providers:

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$91 |

$86 |

$115 |

$101 |

$157 |

$129 |

|

|

$61 |

$42 |

$74 |

$59 |

$115 |

$87 |

These figures are estimates only, based on a $10,000 guaranteed issue final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our final expense insurance options, call us at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m. ET.

Alternatives to Guaranteed Life Insurance

If you aren’t affected by any of the conditions listed above, you are likely eligible for coverage by non-guaranteed plans. No-wait final expense insurance is very accessible, even with health concerns. If you’re not eligible for a no-wait plan, you can probably qualify for a graded plan with lower premiums than a comparable guaranteed policy.

1

No-Wait Final Expense Insurance

No-wait final expense plans have stricter eligibility requirements than guaranteed life insurance, but you may be surprised to see how lenient medical underwriting can be. Many final expense policies, even those with no waiting period, are “simplified issue,” which means medical questions, requirements, and underwriting are streamlined. Some policies may require a medical exam.

The biggest benefit to a no-wait policy is the price. Rates can be significantly lower for a no-wait policy. Here are sample rates for a $10,000 policy for a non-smoking applicant with no pre-existing conditions from our top providers.

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

|

|

$34 |

$29 |

$50 |

$40 |

$82 |

$56 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

2

Graded / Modified Final Expense Insurance

While guaranteed plans often pay benefits in a modified structure, not all modified final expense insurance plans are guaranteed. However, modified plans are about as close to guaranteed as you can get without being guaranteed policies.

Modified plans with a waiting period accept most health conditions, and if you don’t qualify for a no-wait plan, you have a pretty good chance of qualifying for a modified plan. Most non-guaranteed, modified final expense policies have much lower rates than similar guaranteed plans. Unlike guaranteed plans, many carriers like United Home Life offer extensive customization on graded ones.

Below are sample monthly rates for our top-rated graded final expense providers, all calculated with a $10,000 graded policy for a non-smoking applicant with no preexisting conditions. Note that rates may vary due to included insurance riders, preexisting condition policies, etc.:

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$49 |

$39 |

$78 |

$60 |

$122 |

$91 |

|

|

$45 |

$39 |

$76 |

$53 |

$145 |

$89 |

|

|

$40 |

$30 |

$57 |

$43 |

$87 |

$64 |

|

|

$38 |

$30 |

$59 |

$46 |

$105 |

$79 |

|

|

$44 |

$32 |

$60 |

$49 |

$93 |

$75 |

|

|

$59 |

$56 |

$85 |

$76 |

$142 |

$110 |

These figures are estimates only, based on a $10,000 graded / modified final expense insurance policy with no additional applicant pre-existing conditions.

If you’re interested in these or any of our other final expense options, call Final Expense Benefits at (866) 786-0725.

Final Thoughts

Guaranteed life insurance is pricey but can be quite helpful for those who need it. Thankfully, most carriers offer final expense insurance with seniors in mind and accept applicants with many preexisting health concerns.

Final Expense Benefits is here to help you get the best available coverage at a great rate. We can help you find a policy that fits your needs with the best rates, customization, and coverage available.

FAQ

Can you get guaranteed acceptance life insurance with no waiting period?

Unfortunately, no guaranteed policy has no waiting period.

What does guaranteed life insurance mean?

Guaranteed acceptance life insurance means that providers accept any applicant, regardless of health history.

Can you have more than one guaranteed life insurance policy?

Like any other final expense insurance policy, you can have as many guaranteed policies as you want, as long as you keep up with monthly premium payments.

How do you get guaranteed life insurance?

Guaranteed plans typically have a streamlined application process. You can often apply directly on provider websites or through life insurance agencies.