Kemper Life Insurance Review: Everything You Need To Know Before Purchasing

Updated on Jan 9, 2025 • 6 min read

Kemper Life Insurance has provided life insurance to Americans for over 30 years, but how do their services measure up? Is Kemper Life Insurance worth your time and money? Final Expense Benefits is dedicated to providing transparency so you can make an informed decision when it comes to your life insurance plan. We will discuss the benefits, drawbacks, and financial strength of Kemper Life Insurance. When it comes to protecting you and your loved ones, Final Expense Benefits has you covered. Continue reading to learn more about Kemper Life Insurance, or call Final Expense Benefits at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET to ask questions and to find a plan that works for you. Our free online quoting tool is available 24/7 for you to receive a free estimate.

The amount of options in the life insurance market can be overwhelming. That’s why Final Expense Benefits is here to help. As a trusted life insurance brokerage, Final Expense Benefits can help you find a reliable policy that covers your needs from a reputable provider.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more.

What is Kemper Life Insurance?

Kemper Life Insurance was founded in 1990 under the name Unitrin, Inc. The company was founded to replicate the success of Teledyne, an industrial conglomerate founded by Henry Singleton and George Kozmetsky.

Unitrin shares were priced at $31.25 a share upon debut on the NASDAQ stock market. Unitrin split insurance services into three subgroups: life, property, and consumer insurance.

In 2010, Unitrin purchased the rights to the name “Kemper” and began operating under that name in 2011.

The Kemper Life Insurance headquarters is located in Chicago, IL. The company currently owns $13 billion in assets and was named by Forbes as one of the best insurance companies of 2025.

Coverage Options With Kemper Life Insurance

Kemper Term Life Insurance

Term life insurance is also referred to as standard coverage, or “pure” life insurance.

You are typically provided with a length of time, during which you are guaranteed payment as stated by the death benefit if the policyholder dies during this period. An individual can pay for coverage for a predetermined period of time.

Kemper offers three options for term life coverage, including, 10, 20, or 30 years. Coverage options for Kemper Term Life Insurance range from $25,000 – $250,000. Unlike Whole Life insurance, when the term period ends, the benefits of the policy also end.

If the policyholder is alive at the end of the term, you can renew for an additional term, or convert the existing coverage to permanent coverage.

Term life insurance usually has an affordable introductory price point given the amount of coverage provided. A medical exam is typically required for this form of insurance.

Plans with higher death benefits will typically cost more per month. The monthly payment is called the premium.

Life insurance comes in three major forms: final expense insurance (also known as burial insurance), term life insurance, and whole life insurance. Each type’s purpose and intended market are different.

Kemper Guaranteed Issue Life Insurance

Guaranteed Issue Life Insurance is a type of whole life insurance that accepts applicants regardless of their status. This option is closest to a standard final expense insurance.

Guaranteed issue life insurance requires no medical examination or background check. This is a great option for individuals who may otherwise be ineligible for standard life insurance, such as someone with a health issue.

Applicants between three and eighty may already be approved, provided they are not terminally ill, residing in hospice, a care facility, a hospital, nursing home, or receiving home health care.

Guaranteed issue policies from Kemper also offer guaranteed rates, so it accumulates cash and loan value over time for its beneficiaries. Premiums are level throughout the policy’s payment period.

Best $10,000 Burial Insurance Companies

If you’re looking for a policy with $10,000 in coverage that remains instated throughout the remainder of your life at the premium you locked in at, then we’d like to recommend a few names that may be of interest to you and your wallet.

Here are the expected monthly premiums for Final Expense Insurance for a healthy, non-smoking individual from our top providers:

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

Kemper Accident and Health Insurance

Accident and health insurance prevents policyholders from being negatively affected by unexpected medical bills. This plan provides treatment options or financial relief to those who are impacted.

Accident and health insurance can help cover expenses such as hospital stays, surgical, or other medical costs.

Kemper will provide lump-sum benefits that help to cover costs associated with the first occurrence of heart attacks and cancer. This plan covers first occurrence heart attacks, unforeseen accidents, and first diagnosis of cancer.

Kemper Life Insurance Ratings For Credit and Customer Service Satisfaction

A.M. Best Rating

Their ranking system is meant to help understand their overall quality. They use a letter ranking system, which varies from A+ to F. The rating is determined by management, performance, financial flexibility, and shareholder safety.

Kemper was rated A- in 2024, implying good, but not perfect financial health.

Better Business Bureau

Moody’s

As of 2024, Moody’s Investors Service changed the outlook of Kemper from negative to stable. A stable outlook from Moody’s indicates that a rating is not likely to change.

Moody’s rating scale aims to determine the likelihood that an organization will be able to meet financial obligations. This score can help investors decide on their portfolio.

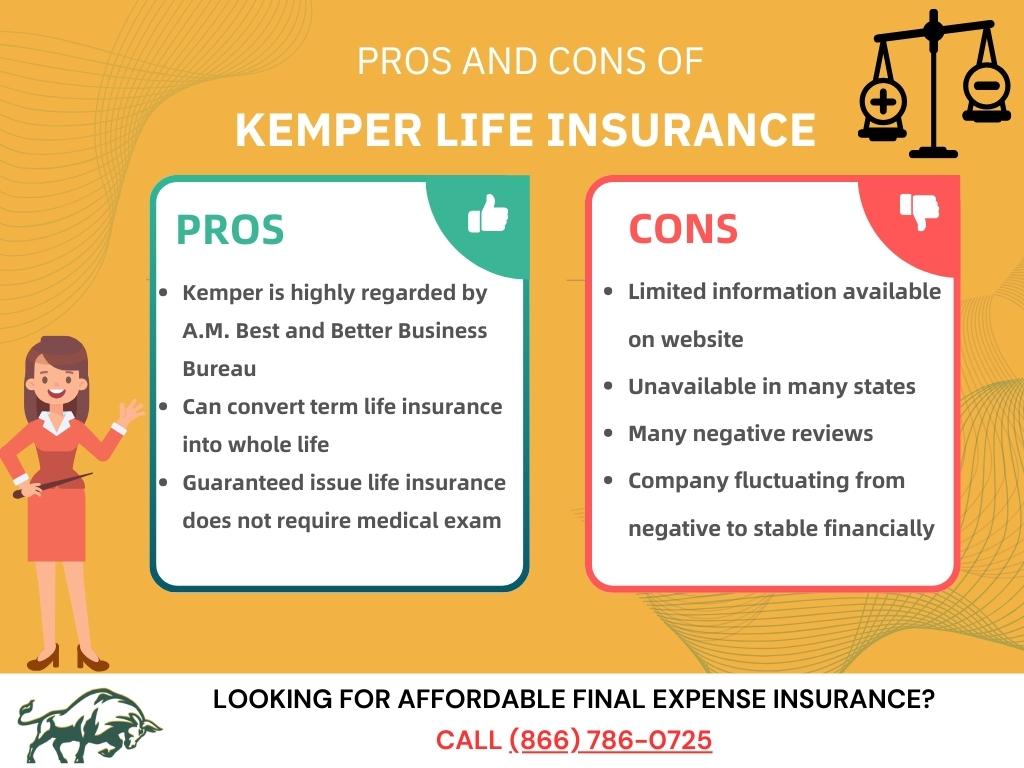

Kemper Life Insurance Pros & Cons

Pros

- Highly regarded by A.M. Best

This rating is a strong indication of Kemper’s financial integrity

- A+ rating from BBB

This rating from BBB indicates a strong commitment to ethical business practices

- Guaranteed issue life insurance does not require a medical exam or questions.

- Option to convert term life insurance into whole life insurance.

Cons

- Next to no online functionality.

The only thing you are able to do via their website is acquire the surface level requirements needed to apply for their policies, as well as a brief excerpt of what they do.

- High number of customer complaints.

Kemper currently sits with a 1.8/5 rating on TrustPilot. Many reviews mention difficulty in receiving payment from claims.

- Unavailable in many states.

Kemper life insurance is currently available in only 27 states.

- Company fluctuating from negative to stable.

According to Fitch Ratings, Kemper has been fluctuating between negative and stable.

Kemper Life Insurance Reviews

Ray J.

Mesa, AZ

1/5

Stacey V.

Pittsburgh, PA

1/5

William G.

Morton Grove, IL

1/5

Our Review and Final Thoughts

Customer reviews for Kemper Life Insurance are poor. The company has a 1.8/5 star rating on TrustPilot. Many customer reviews note that Kemper refused to pay their claim, leaving them to try and cover costs.

On the other hand, Kemper offers a guaranteed issue life insurance policy that does not require a medical exam. This is a great option if you have been denied life insurance coverage or have a preexisting condition.

We’d argue that you have plenty of other options that have better customer reviews and pricing.

We say this because there is no area where Kemper Life Insurance stands out particularly, the only reason to consider this provider is if you have personal ties to the company or if you already have a policy with them due to your parents/loved ones.

Final Expense Benefits only works with the best carriers to provide you and your loved ones with the coverage you need.

We partner with over 20 carriers, including:

Call our expert agents Monday through Friday, 9 A.M. – 5 P.M. ET at (866) 786-0725 or check out our free online quoting tool to receive an estimate.

Frequently Asked Questions

Is Kemper Life Insurance Legit?

Yes, the company is legitimate. Kemper has a high number of policy-holders and total assets are in the billions.

Is Kemper Insurance Good?

While Kemper may have a policy that fits your needs, the company has poor customer reviews and high premiums.

What Determines Coverage Eligibility?

Determining factors for coverage include age, medical history, and physical health. When an underwriter reviews your application, they are trying to determine your risk level. If you have many severe health problems, then you will most likely have to pay a higher premium.