Life Insurance for Young Adults: Benefits, Types & Sample Rates

Updated on June 11, 2026 • 6 min read

Young adults often misunderstand that life insurance is only useful to older people or those well-established in a career. However, there are some serious benefits to life insurance for young adults.

One of the major advantages is that once you’ve signed up, your premiums are locked-in for life, unless you don’t pay the monthly fee. The earlier you sign up, the less expensive it will be for you to get coverage, and that’s just one of the many benefits of applying to life insurance earlier. We’ll give you the rundown of every benefit, life insurance type, and sample rates you can expect as a young adult.

For assistance finding the best life insurance for young adults, contact Final Expense Benefits at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m. ET. As a trusted life insurance brokerage, we can help suggest the best life insurance policy for your situation. Be sure to check out our free online quoting tool to get cost estimates for a plan.

The Benefits of Life Insurance For Young Adults

Life insurance for young adults has a few clear benefits. Chief among them is that while you are young and in presumably good health, you can lock in significantly lower monthly premium rates than if you had waited until you’re in your 50s or beyond.

You’ll also have a wider range of options. If you wait to purchase life insurance until you reach an older age, you’ll have a smaller list of options and may not be able to get certain insurance types.

With all your choices, you can perfectly tailor your life insurance coverage to meet your and your family’s needs.

A huge advantage of getting a whole life insurance policy is that the cashout value of the policy increases, just like an investment account. Starting whole life insurance early compounds the account’s value over time. This will allow for a bigger cashout value and, depending on the type of account, can even add value to the benefit payout.

Is Life Insurance Worth it in Your 20s?

In general, it’s hard to recommend life insurance for folks in their 20s. However, there are a few reasons why you might consider life insurance into your 20s:

- Premiums are at their lowest: On average, a 25-year-old will pay 40% less than a 40-year-old for the same amount of coverage.

- Locks in insurability: Health issues that typically occur as you age can disqualify you or significantly raise rates. If you want the cheapest coverage for life, you should purchase a policy sooner rather than later.

- Cash value compounds: With whole life insurance, your cash value will increase the longer you have the policy. In your 20s, you’ll have longer time to accrue value.

However, life insurance policies for someone who is single, healthy, debt-free, has no dependents, and works a low-risk job is harder to justify. If you are interested in obtaining a life insurance policy, we recommend investing in an term life insurance policy instead of a whole life policy.

The Types of Life Insurance Available to Young Adults

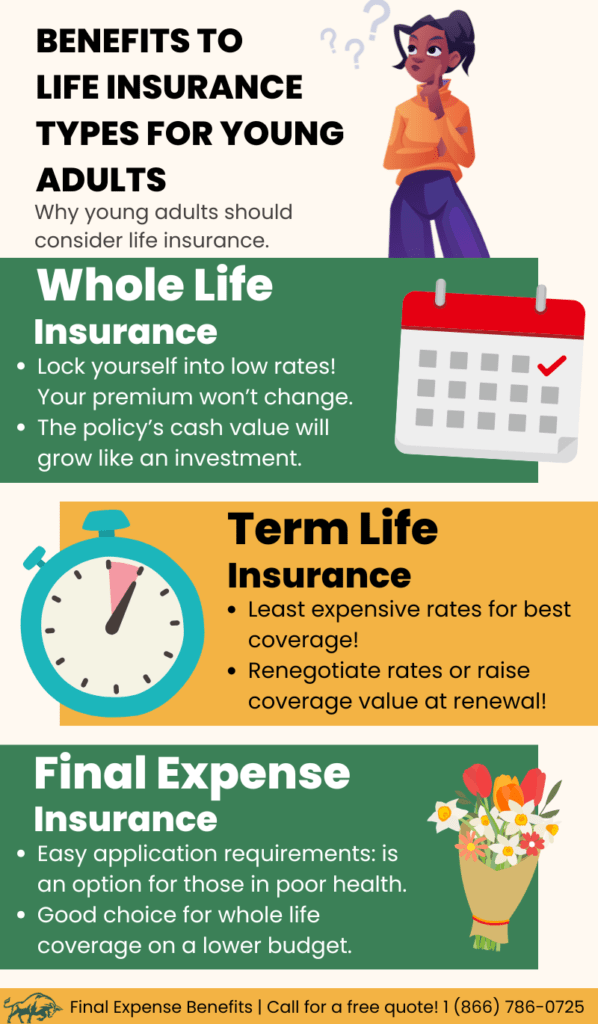

Life insurance for young adults is often available in three major forms. Most policies will function the same for a young adult as an older applicant, just with the advantages above. The three best types of life insurance for young adults are term life, whole life, and final expense insurance.

1

Term Life Insurance

Term life insurance can be a great option for young adults. It’s the most recommended policy type at a young age because it’s excellent on a budget. You’ll still get the same payouts as a whole life policy, but at a significantly lower rate.

You must renew a term life policy once the term is over. Terms usually range from 10 to 40 years, but many policies also have the option to turn them into a whole life plan once the term ends.

Remember that many term life policies require a medical exam to qualify. Term life plans will often only accept younger applicants in good health, so take advantage of the opportunities these less expensive policies give.

2

Whole Life Insurance

Whole life insurance for young adults has significant advantages over a comparable term life policy.

The most enticing benefit is that you’ll be locked into a potentially low rate – for the rest of the policy’s lifespan. While that rate will almost always be higher than that of a comparable term life policy, there’s no guarantee that once your term plan ends you can keep the same rates.

You’ll be significantly older than when you first negotiated rates, which means you’ll be quoted for higher monthly rates. As term policies are stricter in their application processes, you may no longer be eligible for your previous policy.

A whole life insurance policy will also gain value over time, similar to a 401k or other investment accounts. Putting in cash from your premium payments will allow the policy to accrue value over time. This will increase its cashout value. Depending on the policy, your monthly payments could also increase the benefit payout’s value.

3

Final Expense Insurance

Final expense insurance, or burial insurance, can be a viable choice for young adults. While many plans are intended for older applicants and have minimum age requirements, finding a final expense life insurance policy that can work for young adults is possible.

Final expense insurance is a whole life policy, so you get all the benefits of whole life at a less expensive monthly premium rate. The payout will also be smaller, as its scope focuses on paying for funerary bills and similar end-of-life expenses.

Final expense insurance often requires a waiting period, typically two years, so getting it ahead of time can nullify that wait. Some policies with no waiting period are available, but these are accompanied by higher premium rates and typically are intended for older applicants.

Final expense insurance rarely requires a medical exam to qualify. It can be an attractive option for those looking for the benefits of whole life but constrained by a lower budget.

Things to Consider When Looking For Life Insurance for Young Adults

Several factors can help you determine if life insurance is a good option. First, consider your health. Many policies, especially less expensive term life plans, require answering a medical questionnaire or even undergoing a medical examination. Whole life and final expense insurance policies may not ask you to prove you’re of upstanding health, but will often carry higher monthly premiums.

If you smoke or are in poor health, you may not qualify for the lowest possible rates, but you can still get less expensive rates than an older applicant with a comparable policy. Your income and debts can be a major factor in choosing life insurance, especially for young adults. Life insurance can be a major additional monthly bill and at a time when you may just be starting your career, stretching your income may be challenging. While life insurance for young adults has some lower-cost options, there’s a reason why life insurance is generally geared toward those with an established income stream. Also, consider your current or future family. It’s a great idea to plan for them with a supportive life insurance policy and help them cover major bills with a lump-sum payout. Just ensure you’re not putting yourself and your family into a tough financial situation with an unnecessary additional bill.

What If You Have Student Loans?

Another item to consider is the amount of student loans you carry. If you have a significant remaining balance, it might be worth investing in life insurance as a young adult. If you were to pass away before you’ve fully paid off your student loans, the burden to pay them off will go to your co-signer. That means placing the financial burden on a loved one.

It would be wise to discuss your options and seek a term life policy that could cover the cost of your funeral and pay off your student loans.

How Much Does Life Insurance For Young Adults Cost?

Life insurance can be inexpensive for young adults, especially term life policies. As a young and healthy applicant, you’d be eligible for very low monthly premiums, even for considerable coverage. Below are sample rates for non-smoking individuals with no preexisting medical conditions for final expense insurance and term life insurance.

Whole Life Insurance For Young Adults Prices

| Company |

Male 25y/o |

Female 25y/o |

Male 30y/o |

Female 30y/o |

Male 40y/o |

Female 40y/o |

|---|---|---|---|---|---|---|

|

$16 |

$15 |

$18 |

$16 |

$25 |

$21 |

|

|

Liberty Bankers Life |

$17 |

$15 |

$19 |

$16 |

$24 |

$21 |

|

$17 |

$15 |

$19 |

$16 |

$25 |

$21 |

|

|

$21 |

$19 |

$21 |

$19 |

$24 |

$22 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

Term Life Insurance For Young Adults Prices

| Company |

Male 25y/o |

Female 25y/o |

Male 30y/o |

Female 30y/o |

Male 40y/o |

Female 40y/o |

|---|---|---|---|---|---|---|

|

$19 |

$19 |

$22 |

$23 |

$32 |

$28 |

|

|

$19 |

$19 |

$21 |

$21 |

$31 |

$31 |

|

|

$20 |

$15 |

$21 |

$17 |

$31 |

$26 |

|

|

$19 |

$18 |

$22 |

$21 |

$38 |

$36 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

Conclusion

Life insurance is a great option for young adults. Locking in a low premium rate when you’re in good health is great, and you can watch your policy’s cash value climb.

Determining the policy or provider that is right for you can be tough. There are a lot of options, and if you do it by yourself, you might not find the best policy or premium rate. Get in touch with our expert agents at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m. ET. and be sure to use our free online quoting tool so that you’re prepared to confidently navigate the life insurance market as a young adult.

Final Expense Benefits is here to help you understand the life insurance market and see how a policy can fit into your financial toolkit. Call us at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET, to learn more about life insurance, and be sure to use our free online quoting tool for pricing estimates.

FAQ

What type of life insurance is the best for young adults?

Why should a young adult get a whole life insurance policy?

Is life insurance worth it if you're single with no dependents?

Yes, even without dependents, life insurance can cover debts, build cash value, and you can lock in the lowest rates.

What happens to my life insurance if I change jobs?

Individual policies will follow you regardless of job changes. If you received a life insurance policy through your employer, you’ll need to find out what happens by contacting your HR representatives.

Is it too early to get life insurance at 18?

No, most policies have 18 as the minimum age. Buying earlier locks in the absolute lowest rates, some policies allow minors to be added to a parent’s plan.