Final Expense Benefits Metlife Comprehensive Insurance Guide 2024

Easy Navigation

Metlife, is debatably one of the first and oldest names in the insurance game. They used to sell individual policies like any other agency, but recently in 2010, this was discontinued in favor of group policies. How are these group policies? Are they still worth your time? Money?

Let’s get into it.

The Origin Of Metlife Insurance

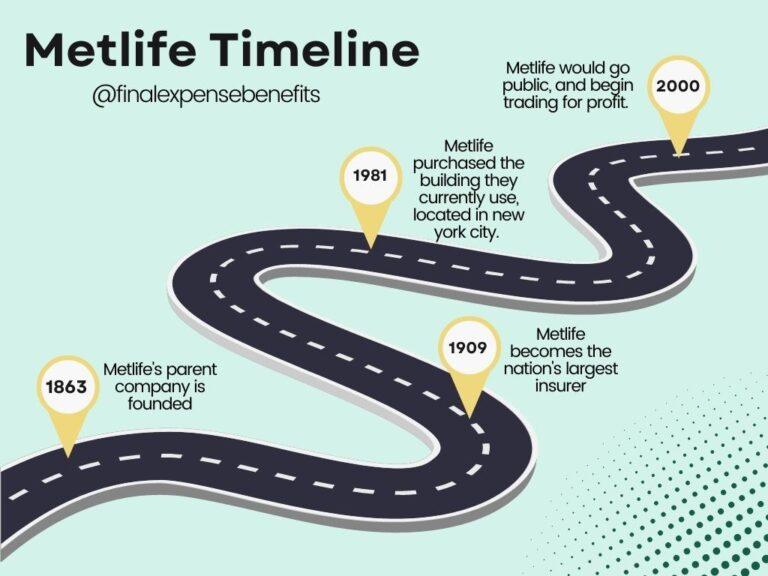

Beginning all the way back in 1863, a group of New Yorkers raised $100,000 to found the National Union Life and Limb Insurance Company – the parent company of Metlife Insurance. Their specialty back then revolved around insuring Civil War sailors/soldiers from any disabilities sustained as a result of wartime efforts. 5 years later, in 1868, they would move towards general health insurance after changing their name to Metropolitan Life Insurance Company. The company faced great hardship towards the late 1870’s, when they would reach their lowest point.

10 years later, the company would introduce traditional insurance policies to the American population utilizing a weekly or monthly payment collection system. By 1880, sales exceeded $1 million and in 1909, Metlife Insurance would become the nation’s largest life insurer in the United States. Fast forward to WW2, Metlife Insurance would provide more than 51% of all total war bond assets and was the largest insurance contributor to the American cause. In 1981, the Metlife Insurance building was acquired by Metlife Insurance for 400 million, where they still reside today. In 2000 Metlife Insurance would convert their services from a mutual insurance agency to a publicly traded for-profit business.

Notable Developments

1863: Metlife Insurance’s parent company, National Union Life and Limb Insurance Company is founded.

1868: NULL became known as Metropolitan Life Insurance Company.

1873: The Great Panic occurred, putting Metlife Insurance at their lowest point.

1879: The Company introduced traditional insurance policies.

1880: A million in collected premium was reached.

1907: The iconic clock tower was commissioned where it would go on to feature in their advertising for years to come.

1909: They would become the nation’s largest life insurer.

1924: During WW2, Metlife Insurance would produce more than 51% of the total assets involved in the war effort.

1979: operations were segmented, into group insurance, personal insurance, pensions as well as investments.

1981: Metlife Insurance purchased the Metlife Insurance building for $400 million.

2000: Metlife Insurance would convert from a mutual company to a publicly traded for-profit corporation.

Your Coverage Options With Metlife Insurance

A standard set of policies, term and universal life insurance. On top of this, Metlife Insurance features a subsection to their company just dealing with group policies. Another plus is that they offer a variety of additional riders one may customize their policy with.

Metlife Term Life Insurance

Standard Coverage, or “pure” life insurance. Generally, you’re provided with a term, such as 20 years for example, wherein you’re guaranteed payment as stated by the death benefit if the policyholder dies within the stated term. If alive at the end of term, one may renew for an additional term, or convert the existing coverage to permanent coverage. The perks of this coverage involve the introductory price point, which is generally the most budget-friendly option for the relative amount of coverage received. Depending on if it’s simplified or guaranteed, This form of insurance usually requires a medical examination.

Metlife Universal Life Insurance

Similar to a whole life insurance policy, a Universal Life Insurance Policy offers long-term protection and coverage, although without the luxury of fixed premiums. As a result, your premium can change depending on current economic conditions. With this in mind, your policy could substantially increase in price as you get older. The upside to this policy type, though, is the fact that the payment schedule associated with such a policy is very flexible and allows for payments to be made at the discretion of policyholders.

Best $10,000 Burial Insurance Companies

If you’re looking for a policy with $10,000 in coverage that remains instated throughout the remainder of your life at the premium you locked in at, then we’d like to recommend a few names that may be of interest to you and your wallet.

| Company | 50 y/o Male | 50 y/o Female | 60 y/o Male | 60 y/o Female | 70 y/o Male | 70 y/o Female |

|---|---|---|---|---|---|---|

|

$49 |

$39 |

$74 |

$59 |

$107 |

$85 |

|

|

$58 |

$49 |

$76 |

$60 |

$127 |

$96 |

|

|

$44 |

$34 |

$64 |

$47 |

$110 |

$78 |

|

|

$51 |

$43 |

$64 |

$53 |

$119 |

$88 |

|

|

$82 |

$56 |

$101 |

$79 |

$158 |

$119 |

These figures were obtained from the NFDA and are estimates only. For a detailed quote, please contact an agent.

Metlife Insurance Funeral Insurance

Final expense insurance is the type of insurance that’s in place to cover the funeral costs after your passing. While final expense coverage is generally used to cover funeral/burial costs, one may use the funds in any way desired. Final expense coverage usually exists as a simplified issue plan, meaning that you are approved regardless of any previous medical conditions, 99% of the time. The premiums are also generally low (depending on the condition of the applicant) and whole life, meaning that your rate does not change within the span of your lifetime.

Additionally, these plans can coexist with Medicaid, depending on your total assets. If said assets are too high to qualify, one may withdraw and use these funds to purchase additional coverage or what have you, maximizing your beneficiaries’ payout. Metlife Insurance claims to offer final expense insurance, but upon looking into the coverage options available on their website, there was nothing applicable. Nowhere did we see guaranteed issue or final expense insurance.

Is Metlife Insurance A Legitimate Life Insurance Company?

Absolutely.

With almost 200 years of providing insurance to Americans, on top of their immense market share of 11.3%, and almost 1 trillion in assets, it’s no wonder they’re the most numerous insurance providers in America as of 2024. But, does the biggest mean the most legit? Not necessarily. Although we didn’t find anything glaringly bad, minus their NAIC score, it’s never a good idea to assume the biggest = the best.

Metlife Insurance Pros & Cons

Pros

- Largest insurer in the country.

Holding over 11% of the entire insurance market (in America), as well as almost 2 millenium of service, it’s no wonder Metlife Insurance is the largest insurer in the country, as it’s probably the oldest.

- Competitive group policies.

Although they may have forwent selling individual policies, their group policies are lucrative and do provide a competitive option if it fits your specifications.

Cons

- No individual policies.

In december 2010, Metlife Insurance discontinued selling individual policies to those via agents. Instead, they only offer group policies now usually involving a family or employer.

- Large number given by the NAIC.

Nearly a 4.0 rating, Metlife Insurance’s current customer relations as surveyed by the NAIC are almost 4x that of the industry average.

- No online quote tool. At least for their life insurance products.

Most insurers/brokeridges at the very least offer you a quote tool so that you may gather information before participating in the agent process. Metlife Insurance does not have an online quote tool for their life insurance products, most likely as a result of their discontinuation of individual life insurance policies.

Ratings For Credit And Customer Service Satisfaction

A.M. Best Rating Service

They utilize a rating, similar to the letter ratings placed on restaurants, meant to help you discern their overall quality. This letter ranking varies from A+ to F, similar to a scholastic grading system, and this organization is overseen by the chief insurance regulators regarding any US-affiliated territory. The rating itself is determined by a variety of different factors, such as performance, management, financial flexibility, shareholder safety, etc. The rating given to Metlife Insurance as of 2021 is an A+, reflecting near-perfect scores in financial strength.

NAIC

The NAIC, or The National Association of Insurance Commissioners, is a regulation standard support organization based in America meant to add credibility to insurance companies. Essentially, the goal of this organization is to protect consumers and to mandate that insurers deliver on their promises made. The rating used within the NAIC, involves a numerical value usually ranging from 1 – 10. One implies average customer complaints, where anything above this is above average, and so on. The rating that was given to Metlife Insurance for individual life insurance is 3.75, making it 3x the industry average. In regards to all of their products, the average is only 0.64. This gives us an indication of how working with them for life insurance will be.

J.D Power

JD Power ratings are essentially nationwide surveys that allow consumers an unbiased opinion regarding what other consumers say about said company. Generally, these surveys take a group of companies, usually around 21, and rate the companies in relation to each other. This is done either through focus groups, paid calls, or what have you. JD Power spends large sums of money annually simply on data specifically for this reason.

Metlife Insurance ranked 14th out of the 21 insurance companies surveyed in JD power’s 2021 insurance survey, which is in the bottom 33%.

Metlife Insurance Reviews

Our Review and Final Thoughts

Frequently Asked Questions

Where is the Metlife building?

In downtown New York City.

When Was the Metlife Stadium Built?

April 10th, 2010.

Are Metlife and Brighthouse the same?

Throughout a series of mergers the answer is essentially yes. They belong to the same subgroup of insurers.