What Is Term Life Insurance?

Updated on Jan 20, 2025 • 9 min read

Term Life Insurance is the simplest form of life insurance, existing in term increments of 10-40 years, sometimes referred to as traditional life insurance.

Term life insurance exists like other life insurance policies, offering a death benefit to applicable beneficiaries only if death occurs before the end of the specified term.

Typically the most lucrative and inexpensive policy, term life insurance is the premiere life insurance option in most cases, allowing for users to convert existing term coverage into permanent coverage at the end of the term so long as the applicable conditions are met (such as a conversion rider, or other like-minded specification).

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

How Term Life Insurance Works

When buying or applying for term life insurance, either through a brokerage or through a carrier themselves, your overall health is assessed either through a medical exam, or medical questionnaire. From here, your monthly premium and maximum death benefit are adjusted to match the relative risk you pose the company, as per your health exam/questionnaire. Not only is your medical history assessed, but your criminal/driving record, habits, occupation and family history are also up for discussion.

As a result of term life insurance containing some of the most rigorous underwriting procedures and restrictive term lengths, you’re rewarded with a lower monthly premium. Term life insurance pays out your specified death benefit to beneficiaries if death occurs within the specified term. If the policy expires before death of conversion occurs, the policy is voided.

Types Of Term Life Insurance?

Despite being referred to as traditional life insurance, term life insurance comes in a plethora of different forms, all drastically changing the specifications of the policy. It’s important to consider the different types of term life insurance, as the end goal may change depending on the policy chosen.

For example: a convertible term may be the only option for some individuals, whereas another individual may only require term life insurance for a specific period of time.

1

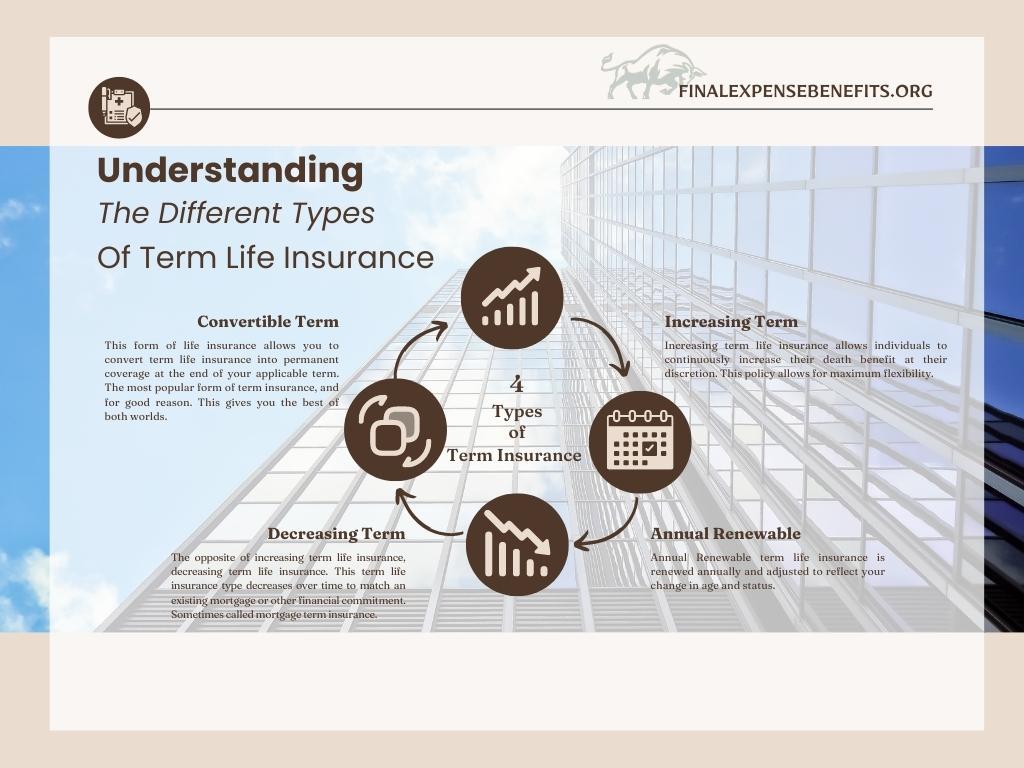

Convertible Term

The most popular form of term life insurance, this option allows users to eventually convert term coverage into permanent life insurance at the end of the applicable term. The most popular form of term life insurance, this policy type offers a middle ground between affordability and safety, leading to permanent coverage so long as premiums continue to be paid. You are also given the option to convert the entire policy or a partial amount of the policy into permanent coverage. Term life insurance also allows users flexibility in converting coverage, offering conversion options before the expiration of the policy as well as the ability to forgo a medical exam when the conversion process begins.

2

Increasing Term

Increasing term policies, also called level death benefits, act almost exactly how they sound – you’re allowed as the policyholder to increase your death benefit throughout the length of your term, with a higher premium as a result. All of this is down without a medical exam, allowing for supreme flexibility. Oftentimes, increasing term policies introduce themselves at a lower premium and slowly ramp up over time. This form of term life insurance also prevents individuals from re-taking a medical exam for an additional death benefit later on down the road.

3

Decreasing Term

Decreasing term policies, inversely similar to increasing term policies, act exactly as they sound. With your death benefit and monthly premium slowly decreasing over time, the goal of this policy is to cover a specific need or to prepare for an upcoming circumstance. This form of term policy is sometimes referred to as mortgage term life insurance as its purpose is to match any outstanding mortgage debt and slowly decreases over time as a result.

4

Annual Renewable

Annual Renewable term life insurance is renewed annually as the name suggests, usually at a higher monthly premium to reflect your increasing age. The benefits of this policy type involve your guaranteed renewable access every year, but the increasing cost can dissuade some people from choosing this policy.

Who Is Term Life Insurance For?

Generally, term life insurance without the presence of a conversion rider or other customization is marketed towards people with children and/or a mortgage. This also may apply to first time home buyers, part-time employees, and entrepreneurs looking for introductory and affordable coverage. Ideally, the goal of term life insurance is to see your kids out of the house and into college and provides a safety barrier in the meantime. This policy type almost always requires a medical exam or a medical questionnaire at the bare minimum and is suited for those that are in relatively great health.

What Happens If A Term Policy Expires?

As term life insurance exists in terms, the policy may expire at the end of the specified term if other action isn’t taken. When this occurs, the policy expires and the death benefit is lost – monthly premiums are halted as well. If the policy holder had a return of premium policy/rider associated with their policy they are entitled to either full or partial compensation for lost premium. The policy holder also does not need to retake a medical exam when converting term coverage into a permanent whole life insurance policy.

Exceptions include:

– A term conversion rider is present on the policy, allowing for full or partial conversion to a permanent whole life insurance policy.

– Your term life insurance is annually renewable or renews after the specified term.

Keep in mind that if your term life insurance policy expires without the presence of a conversion rider or other applicable circumstance, the death benefit of the policy is essentially lost.

How To Determine How Much Coverage You Need

One of the most common pieces of advice given to those trying to determine the amount of coverage they might need is to multiply your salary by 10. The main issue with this advice is that it doesn’t factor in any potential financial goals or assets within your toolbelt. There’s children to consider, college expenses, debt, etc that come into play when planning ahead for your financial future. It’s also important to go higher rather than lower, as expenses generally tend to rise as the individual moves up in life.

Using the DIME formula, we may more accurately determine the amount of coverage you’ll need moving forward.

Debt and Final Expense: This includes the sum of all of your outstanding debt, as well as any potential final expenses that your funeral may require.

Income: Your yearly salary as well as the amount of years your family will/could potentially need support.

Mortgage: Calculate your current mortgage and the payments required to payoff said mortgage.

Education: The cost of education, including any private schooling or college expenses for you or your child.

Term Life Insurance Pros and Cons

Pros

- Inexpensive.

The most inexpensive type of policy, providing ridiculous death benefits for very inexpensive monthly premiums.

- Customizable.

Term life insurance provides a plethora of different rider and policy options, with conversion options available when the policy expires as well as level death benefits.

- Some of the highest death benefits out there.

With death benefits easily reaching $1,000,000 or more, this is the policy type that is going to provide you with the highest average overall death benefit. This is especially important to note as when converting coverage into a permanent policy, the extremely high death benefit remains without the need to retake a medical exam.

Cons

- This policy can expire.

Without the presence of a conversion rider or other applicable circumstance, the policies’ default state is to expire once the term length ends. When the policy expires, a notice is sent to the provider and monthly premiums are halted as a result. Although the policy by default will expire, you’re given a multitude of options that either allow you to reinstate the policy or convert it into permanent whole life insurance.

- Usually requires a medical exam.

As a result of such lucrative rates, and gargantuan death benefits, the presence of a medical exam is almost always expected. At the bare minimum a medical questionnaire will be given to you unless it’s explicitly stated that no medical underwriting is required.

Why Is Term Life Insurance Worth It?

It boils down to 3 aspects.

1. You are given the most competitive monthly premium and death benefit in the insurance world.

2. You are given the option to convert coverage into permanent whole life insurance at the end of the term selected.

3. Term Life Insurance directly supports taking the time to grow your finances, and may align itself with your mortgage and/or other expenses.

If you find any of these applicable to you, then term life insurance is worth it. Term life insurance simply is the best bang for your buck, especially if you’re a relatively healthy individual and/or require a huge death benefit.

Term Vs Whole Life Insurance

Term and whole life insurance are inherently very different types of insurance policy, with term life insurance generally lending itself to becoming permanent whole life insurance.

Term Life Insurance:

– Term life insurance contains no cash value and does not generate interest.

– The most inexpensive policy type.

– Exists in terms.

– May be converted at the end of the time in most cases.

– Policy expires at the end of the specified term unless converted to permanent coverage.

Whole Life Insurance:

– More expensive than term life insurance.

– Guaranteed death benefit so long as monthly premiums are paid.

– Premiums are locked in upon approval.

– Does contain a cash value and may generate interest.

– Sometimes no medical exam or medical questionnaire.

Term Life Insurance With No Medical Exam?

In some cases you can get term life insurance without taking a medical exam, although this is considerably more rare then traditional term life insurance, as medical

exams are how the insurance provider rates your relative risk and adjusts your rate as a result.

Without the ability to rate the risk posed to the company when insuring you, you’re automatically placed into a high risk category with an accompanying premium to match.

It’s important to keep in mind that this is not always the case, as some providers aim to specifically fulfill this niche.

How Much Is Term Life Insurance?

Monthly premiums heavily depend on the specifications of the individual applying for coverage.

For example, a 45-year-old man who stands at 5 ft 10, 160 lbs, that doesn’t smoke can expect to pay just under $20/month for a $10,000 policy.

Keep in mind, different insurance companies place emphasis on different things, and may be able to offer you a more lucrative rate depending on the provider chosen. Some factors that may change from provider to provider are their emphasis on smoking, your families history, as well as your overall health and habits.

Best 10,000 Term Life Insurance Companies

We’ve attached a table below that may allow you to get a general idea of what to expect for your monthly premium when purchasing term life insurance. Keep in mind that as its term life insurance, your rate is likely to be less then this if you foresee yourself able to complete a medical exam/questionnaire.

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

Final Thoughts

We at Final Expense Benefits partner with over 20 carriers, with:

Being some of the ones that stand out among the crowd. Reduce the stress involved with life insurance and let us do all of the heavy lifting for you. You can reach us at 1 (866) 311-4338, and we’re open from 9-5, Monday through Friday.

FAQ

Are Term Life Insurance Proceeds Taxable?

Life insurance proceeds you receive are not required to be included on gross income and you are not required to report them.

Are Term Life Insurance Premiums Fixed?

Term life insurance premiums are often fixed for the duration of the term length.

Are Term Life Insurance Premiums Refundable?

If a Return of Premium (ROP) rider is applied to your policy then you are entitled to partial or a full refund of premiums paid.