Here's How Much To Expect To Spend On Life Insurance For Smokers - And How To Save On Premiums

Updated on Jan 13, 2025 • 5 min read

Life insurance is one of the surest ways to provide for your family when you pass away. A quality plan can help your family cover big end-of-life expenses and set them up for financial success when you’re gone, but what if you smoke cigarettes? Higher rates, issues with plan eligibility, and more can complicate life insurance for smokers.

If you’re a smoker and want to explore your life insurance options, but high rates and other complications concern you, Final Expense Benefits is here to help. Our expert agents understand the market and will help connect you to the right policy.

For more information on life insurance for smokers, call us at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET. Check our free online quoting tool for personalized pricing estimates.

Can You Get Life Insurance For Smokers?

Smokers are not excluded from life insurance, but policies may cost considerably more than comparable plans for non-smokers. Rates for life insurance for smokers are typically at least 25% higher than non-smoker rates for similar plans, depending on the plan type. Here’s why:

When you apply for a life insurance policy, you go through a process called underwriting. This is what determines your rates and eligibility.

When your application goes through underwriting, your health conditions, trends, and other factors are assessed. Your application is placed in a risk category based on those factors.

Insurers consider smoking a high-risk health condition, and life insurance for smokers is handled much like life insurance for those with preexisting conditions. As a smoker, you’re likely to be placed in the priciest risk category.

What Type Of Life Insurance Is Best For Smokers?

Term life insurance for smokers can end up being prohibitively expensive, largely defeating its main purpose – high-value insurance at a low rate. The same is true for some types of long-term whole life insurance, but one type can be a good choice for smokers and won’t cost too much: final expense insurance.

Final expense insurance premiums are usually relatively low, even for smokers. Final expense insurance is designed to deliver a smaller, more focused payout than other life insurance types, intended to help deal with end-of-life expenses like funerals. Because the payout is smaller, monthly premium rates can be kept lower.

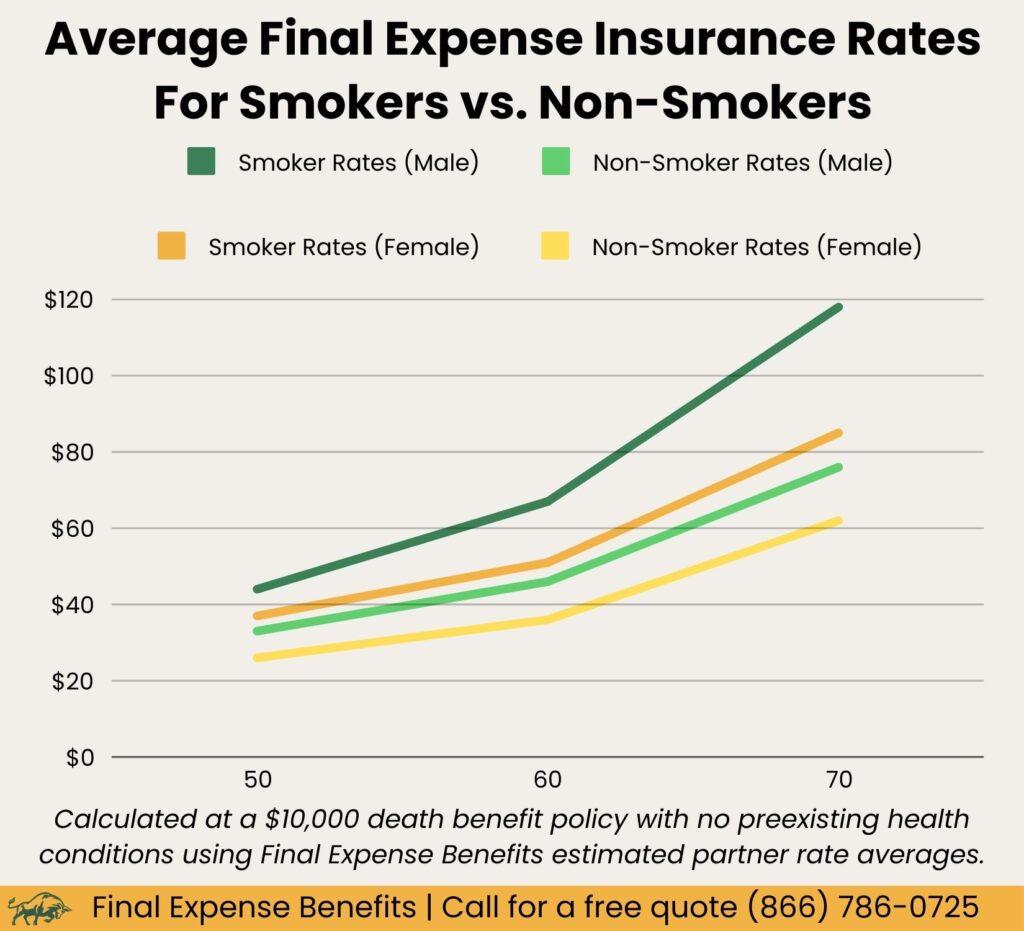

How Much More Is Life Insurance For Smokers?

Life insurance for smokers costs more than non-smokers by a noticeable margin. However, final expense insurance is still affordable, even for smokers.

Here are sample life insurance rates for smokers vs. non-smokers from our top providers:

Rates for life insurance for non-smokers:

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

Rates for life insurance for smokers:

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$48 |

$41 |

$66 |

$51 |

$111 |

$79 |

|

|

$44 |

$38 |

$71 |

$52 |

$130 |

$90 |

|

|

$38 |

$32 |

$60 |

$45 |

$107 |

$74 |

|

|

$49 |

$39 |

$72 |

$59 |

$122 |

$102 |

|

|

$42 |

$34 |

$65 |

$49 |

$118 |

$82 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more.

How Other Tobacco Products Affect Life Insurance Costs

Someone who actively smokes cigarettes will be flagged as a smoker by life insurance companies and will likely have to pay higher rates, but what about other tobacco products?

Other tobacco or smoking products can affect life insurance prices depending on the provider. Even if you aren’t smoking cigarettes, you may have to pay rates similar to those of life insurance for smokers if you:

- Chew tobacco

- Vape or use e-cigarettes

- Smoke cigars or pipes

- Use nicotine patches or other nicotine replacements

- Smoke or vape marijuana

How To Reduce Rates On Life Insurance For Smokers

Many top senior life insurance companies provide discounts or benefits to incentivize quitting smoking. If you have already quit smoking, you may not have to pay the higher prices of life insurance for smokers or at least qualify for a discounted smoker rate.

Depending on the insurance carrier, if you are using nicotine products to quit smoking, you may not be required to pay increased rates. However, this comes down to the underwriting process and highlights the need to work with a trusted broker.

Contact Final Expense Benefits to find discounted rates on life insurance for smokers that you may qualify for.

Recommended Providers of Life Insurance For Smokers

Final Expense Benefits works with over 20 of the best burial insurance companies. We’ve gone through our providers and found a list of five of the best providers of life insurance for smokers:

5

Great Western

Great Western offers competitive rates for smokers and highly rated customer service.

4

Prosperity

Prosperity is a solid middle ground for smokers. They have smoker rates competitive with many of our options and offer exceptional customer service and a quick application process.

3

Aetna Accendo

Aetna Accendo life insurance offers competitive rates across the board, intended to make their insurance offerings a good choice for first-time life insurance buyers.

2

Americo

Americo offers very similar rates for smokers vs. non-smokers. They also accept applicants with a wider range of preexisting health conditions than other final expense insurance providers.

1

Mutual of Omaha

Mutual of Omaha is one of our top-rated providers, and it’s no surprise that they provide competitive rates for smokers. Their rates are the lowest among our top providers.

Conclusion

Final expense life insurance for smokers can be tougher to get than it is for non-smokers, but it’s just as necessary. The life insurance market can be confusing to navigate in general and can be even worse if you smoke.

That’s how Final Expense Benefits can help. We know where to look, what incentives to find, and how to get you the best rates for the coverage you need. Call us at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET, or check our free online quoting tool for rate estimates.

FAQ

If I quit smoking, can I get a reduced rate?

Each insurance provider handles rate specifics differently, but speak with your broker or insurance representative when you are applying for a policy. Rates may be lowered if you quit smoking for an extended period, all at the insurer’s discretion.

How long do I need to no longer smoke to qualify for non-smoker rates?

Most companies consider you a non-smoker if you haven’t smoked for at least 12 months.