Do You Need a Life Insurance Rider? What Every Policyholder Should Know

Updated on June 10, 2025 • 7 min read

Life Insurance Riders, also known as endorsements, are customizable features or “add-ons” one may include within their life insurance policy. Life insurance riders give you the power to tailor your policy to your family’s unique needs. Whether you want to protect a child’s future, secure long-term care, or ensure income keeps pace with inflation, riders offer extra security that standard policies may lack.

If you’re interested in learning more about insurance riders or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

What Is A Life Insurance Rider?

Life Insurance Riders exist separately from your current policy and only serve to supplement your plan. They typically provide additional coverage for specific needs, such as disability, critical illness, or coverage for children.

They are usually added when the policy is first issued, although some can be added later, depending on the insurer. These add-ons often require an extra premium, which varies based on the rider type and amount of coverage.

What Policies Support an Insurance Rider?

Generally, permanent coverage is where riders shine, but riders may also be used in different kinds of policies such as when converting term coverage into permanent whole life insurance.

As riders directly mirror the policy itself, they usually are encouraged within a permanent whole life insurance policy as it makes sense in the eyes of the insurer. Generally the main Life Insurance Riders associated with a term policy are those that allow users to convert term coverage into permanent coverage.

Types of Policies That Allow Riders

Riders are commonly available on term life, whole life, and final expense insurance policies. Availability depends on the insurer and policy type. Final expense insurance often includes basic riders like accelerated death or terminal illness riders at no extra cost and may offer others, such as child term riders or long-term care riders, upon request.

Now that you know which policies support riders, let’s explore the most common types and how each adds value to your policy.

Compare plans with optional insurance riders in minutes and find the right fit for your family’s future. Call our expert agents Monday through Friday, 9 a.m. to 5 p.m. ET at (866) 786-0725 or check out our free online quoting tool to receive an estimate.

Common Life Insurance Riders

If you’re considering enhancing your policy, here are the most common and valuable riders to know about and who they’re best for.

- Guaranteed Insurability Rider: This rider allows you to increase your life insurance coverage at specific intervals (such as marriage, birth of a child, or a new mortgage) without taking another medical exam. It’s ideal for young adults and growing families who anticipate needing more coverage in the future but want to lock in a policy now.

- Waiver of Premium Rider: If you become permanently disabled and can’t work, this rider ensures your life insurance premiums are waived while your coverage remains active. It’s especially valuable for those in physically demanding jobs or with pre-existing health risks.

- Child Rider: A child rider adds a small amount of life insurance coverage for your children under your policy. This coverage can typically be converted into a permanent policy when the child becomes an adult, without a medical exam.

- Term Rider: This rider adds temporary life insurance coverage to your base (usually permanent) policy. It’s commonly used for protection during major financial commitments like a mortgage or raising young children.

- Accelerated Death Benefit Rider: If you’re diagnosed with a terminal illness, this rider lets you access a portion of your death benefit while you’re still alive. It can help cover medical bills, hospice care, or family expenses in the final stages of life.

- Cost of Living Rider: Also known as an inflation rider, this add-on automatically increases your policy’s coverage amount to keep pace with inflation. It’s useful for long-term policies where purchasing power could decline over time.

- Long-Term Care Rider: This rider allows you to use a portion of your policy’s death benefit to pay for long-term care expenses, such as assisted living or in-home nursing care, while you’re still alive. It’s useful for seniors or those with family histories of chronic illness.

- Accidental Death & Dismemberment (AD&D) Rider: In the event of accidental death or serious injury (like loss of a limb or paralysis), this rider provides an additional payout on top of your policy’s base coverage. It offers peace of mind for those with high-risk jobs or active lifestyles

We urge you to consider your options when qualifying for coverage, as most of the time, you can not add riders after the initial coverage application.

Our expert agents can help you navigate rider types and find a great policy that fits your needs and budget. Call Final Expense Benefits today at (866) 786-0725 to learn more.

Does Having a Life Insurance Rider Benefit Me?

Having an insurance rider connected to your policy may not be necessary. They are needed in some cases, such as with a term conversion rider that allows you to convert your term policy into permanent coverage. An insurance rider may also be the glue one may need to fill in the gaps of their policy, as they are highly customizable and, in most cases, very cheap relative to the additional coverage they give you.

Before adding one, it’s important to understand both the potential benefits and reasons it might not be the right fit for your situation.

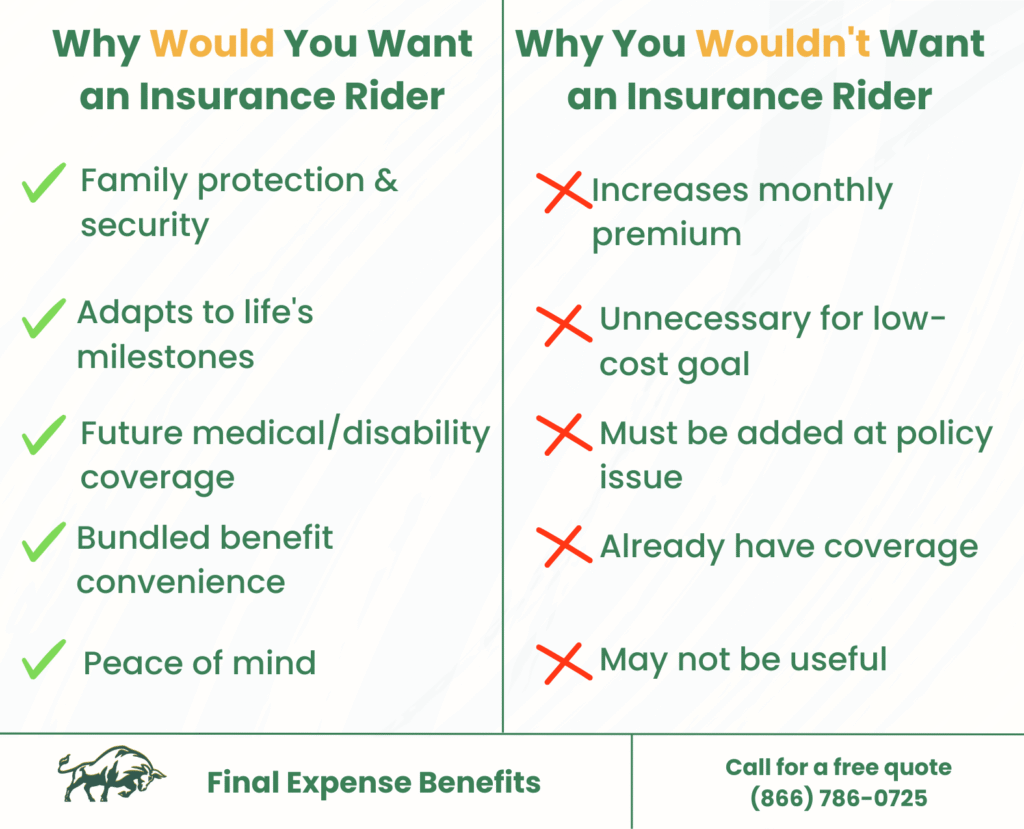

Pros and Cons of Adding an Insurance Rider

Understanding the reasons for and against insurance riders can help you make the best decision for your family’s situation.

Here’s a visual breakdown to help you weigh both sides:

Average Rider Insurance Cost

If you don’t see yourself using it, or if the extra cost will be too much.

Most of the time, an insurance rider incurs an additional cost to your monthly premium.

Although this usually isn’t enough to make a significant difference, they can still be noticeable.

If you genuinely don’t see yourself using it, then there’s no reason to add it to your policy.

Keep in mind though, life insurance riders accompany permanent life insurance policies for the most part, and these last for the remainder of your lifetime so long as premiums are paid.

Since they last for your entire life, It’s important to think ahead when utilizing an insurance rider.

| Rider Type | Monthly Cost | Who It's For |

|---|---|---|

|

Guaranteed Insurability

|

$10–$20

|

Young adults, growing families

|

|

Waiver of Premium

|

$8–$15

|

Those at risk of disability

|

|

Child Rider

|

$5–$10

|

Parents or guardians

|

|

Term Rider |

$10–$20

|

Income protection supplement

|

|

Cost of Living Rider

|

$5–$15

|

Inflation protection

|

|

Long-Term Care Rider

|

$25–$50

|

Seniors planning for health needs

|

|

Accelerated Death Benefit

|

Often free

|

Terminal illness coverage

|

|

AD&D Rider

|

$10–$25

|

Accident-related coverage

|

Additional Factors That Affect Cost

Life insurance rider costs vary based on your age, health, whether you have any pre-existing conditions, coverage amount, and policy type. Older applicants and those requiring medical underwriting typically pay more. Higher benefit amounts increase premiums, and term riders are usually more affordable than riders attached to whole life policies.

How to Lower Your Insurance Rider Costs

To reduce your monthly premiums, consider bundling riders when you buy the policy, as this often leads to lower overall costs. Select only riders that meet your personal or family needs, instead of over-customizing. Using a guaranteed insurability rider may allow you to expand coverage later without purchasing a second, more expensive policy.

What is Final Expense Insurance?

Having an insurance rider connected to your policy may not be necessary. They are needed in some cases, such as with a term conversion rider that allows you to convert your term policy into permanent coverage. An insurance rider may also be the glue one may need to fill in the gaps of their policy, as they are highly customizable and, in most cases, very cheap relative to the additional coverage they give you.

Final expense insurance is a type of whole life insurance specifically designed to cover end-of-life costs, such as funeral services, cremation, burial plots, medical bills, and outstanding debts. Unlike traditional life insurance, it’s easier to qualify for, typically offers coverage between $10,000 and $25,000. It features locked-in premiums, cash value growth, and lifelong coverage as long as premiums are paid.

Benefits of Combining Insurance Riders with Final Expense

Final expense insurance often doesn’t require a medical exam. Applicants answer a few health questions, and some policies are guaranteed issue, meaning no health questions at all. This makes it a strong option for those with chronic conditions like diabetes who may not qualify for traditional life insurance.

Adding riders can extend the value of these policies by offering living benefits and extra protection for your loved ones. Get started today with Final Expense Benefits.

By using our Funeral Expense Calculator, you’ll get a better sense of how much coverage your loved ones need to cover your end-of-life expenses, making it easier to determine which riders are worth including in your policy. Call Final Expense Benefits today at (866) 786-0725 to learn more.

Conclusion

Riders are an extension of your current policy, acting as a support system for said policy that will remain for the remainder of your lifetime. Whether you’re looking to protect a child, plan for inflation, or ensure income during disability, insurance riders make your policy work smarter for your future.

Compare plans with optional insurance riders in minutes and find the right fit for your family’s future. Call our expert agents Monday through Friday, 9 a.m. to 5 p.m. ET at (866) 786-0725 or check out our free online quoting tool to receive an estimate.

FAQ

What is a rider insurance?

Life insurance riders are optional add-ons to policies that enhance and personalize your coverage. They offer flexibility, letting you adapt your policy to unique needs such as like covering dependents, health conditions, or inflation.

Can cash value help lower the cost of insurance rider?

Yes, cash value can help lower the cost of rider insurance. If your life insurance policy builds cash value, such as a whole life or final expense policy, you could use that accumulated value to help pay your premiums over time. While not all riders directly benefit from cash value, it can offer flexibility in managing your insurance expenses, especially as your financial needs change.

How much is rider insurance?

The cost of rider insurance varies between $5 and $50 per month. Pricing depends on the rider type, your age, health status, and the base policy it’s attached to.

Which rider waives premiums if I am disabled?

The Waiver of Premium Rider ensures your policy stays active by covering your payments if you become permanently disabled.

What is a guaranteed insurability rider?

This rider allows you to increase your policy’s coverage at specific times in your life, like marriage or the birth of a child, without undergoing a medical exam.

Can I add a rider after buying a policy?

Some riders, like the guaranteed insurability option, can be added after the initial purchase. However, most riders must be chosen when the policy is first issued.

What's the best rider for families?

Child riders are excellent for parents wanting affordable coverage for dependents. Guaranteed insurability riders are also ideal for families planning for future growth and changing needs.