Complete Underwriting Guide to Life Insurance

Updated on Jan 20, 2025 • 8 min read

Medical underwriting. You may have heard this phrase before, or even participated in it.

But what is it? What does it do for me? What’s the best way to answer medical underwriting

All of these questions and more will be addressed in this article.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

What is Life Insurance Underwriting?

Underwriting is a process companies utilize to appropriately rate the risk you pose to the company. Usually this occurs when the company is “loaning” you something or taking another like minded risk.

Generally, the healthier someone is, the less of a “risk” they pose to the company.

Not only health conditions are addressed with life insurance underwriting, though. Habits like tobacco use, as well as family history, age, weight, are all topics of discussion when it comes to life insurance underwriting.

Not all individuals carry the same risk, for example, if you were loaning money to someone with the risk of a heart attack vs someone with no health problems, wouldn’t you be more worried about the former? It’s a similar concept here.

Another key takeaway is that if everyone was insured at the highest potential risk, then the rates would go up across the board. The fact that some individuals are less of a risk compared to others is what allows for those in good health to qualify for a lucrative policy.

Types of Insurance Underwriting

The four types of Medical Insurance Underwriting are as follows.

1

Guaranteed Issue

Essentially, this means the lack of medical underwriting. The benefits of this underwriting style involve the lack of medical underwriting, meaning that if you know you can’t answer most of the questions confidently, this may be the right option for you. The negatives of this underwriting style is that it automatically labels you as a high risk applicant, therefore giving you the rate of someone considered high risk.

2

Simplified issue

Simplified issue, forgoing the medical exam process in favor of a medical questionnaire as well as whatever tools the insurance company uses to verify your medical/criminal record. This underwriting process is called simplified issue as a result of insurance providers “simplifying” it. The insurance provider forfeits the need for a medical exam, and as a result you are automatically deemed as a relatively high risk to the company to insure. As a result of this underlying risk, your rate will reflect that. A positive to this lack of medical exam involves the speed in which you qualify, usually capping out at no later than 48 business hours after the application has been received.

3

Accelerate Underwriting

Accelerated underwriting, otherwise known as express underwriting, is a middle ground for insurance underwriting, allowing individuals to be expressly rated and qualified for up to $1 million in coverage. This style heavily relies on the external tools employed by the insurance providers to speed up the application process. These tools are used to access your medical history, criminal history (if any), family history, what have you.

4

Full Medical Exam

Depending on the insurance provider, this insurance type is exactly how it sounds, requiring that you participate in a full medical exam. The extent of “full” changes again, depending on the provider. Some insurers may request blood/urine samples, whereas another may request a full paramedic exam and/or EKG. This is generally a good and bad thing, mainly because you are being completely evaluated, meaning you are getting the best rate for your specific qualifications. Full medical underwriting will take longer to assess than a general medical questionnaire, sometimes taking up to 8 weeks to process.

Medical Exam vs Medical Questionnaire?

Most Insurance policies require at the bare minimum you fill out a medical questionnaire so that they may assess the risk level associated with insuring you.

A Medical questionnaire may be the easier option of the two, but both are going to require that you answer/participate with your health as honestly and correctly as possible. Intentionally falsifying your answers is not a great idea in any circumstance, as the provider can easily and efficiently confirm this via your medical records.

A Medical Exam also implies that your premium will be less, or the waiting period non-existent – with the hard part being qualifying or “passing” the exam.

Key Takeaway: Insurance policies without a medical exam or health questions will result in a waiting period.

What Questions Can I Expect To See On A Questionnaire?

Medical underwriting questions are meant to assess the risk you pose to the company, or essentially how long you are presumed to live.

Not all companies are the same in what they prioritize, although there are a few questions that you can expect on every single medical underwriting application.

The questions that hold the most weight, at least in the eyes of the insurer, are going to revolve around your Age, Weight, Smoking Habits, as well as you and your families’ medical history.

Even some “irrelevant” questions, such as your gender, plays a key role in assessing your risk to the company, as it is statistically true that women live longer than men.

Some questions you can expect to see:

- Age

- Gender

- Height

- Income

- Occupation

- Hobbies/Habits

- Current/Past Health History

- Your families’ health history

- Smoking/Alcohol habits

- Criminal History

- Prescription use

Sample Questionnaire

![2022 burial insurance with no waiting period [sample questionnaire]](https://finalexpensebenefits.org/wp-content/uploads/2022/10/Always-expect-to-see-this-question.-1-1-917x1024.jpg)

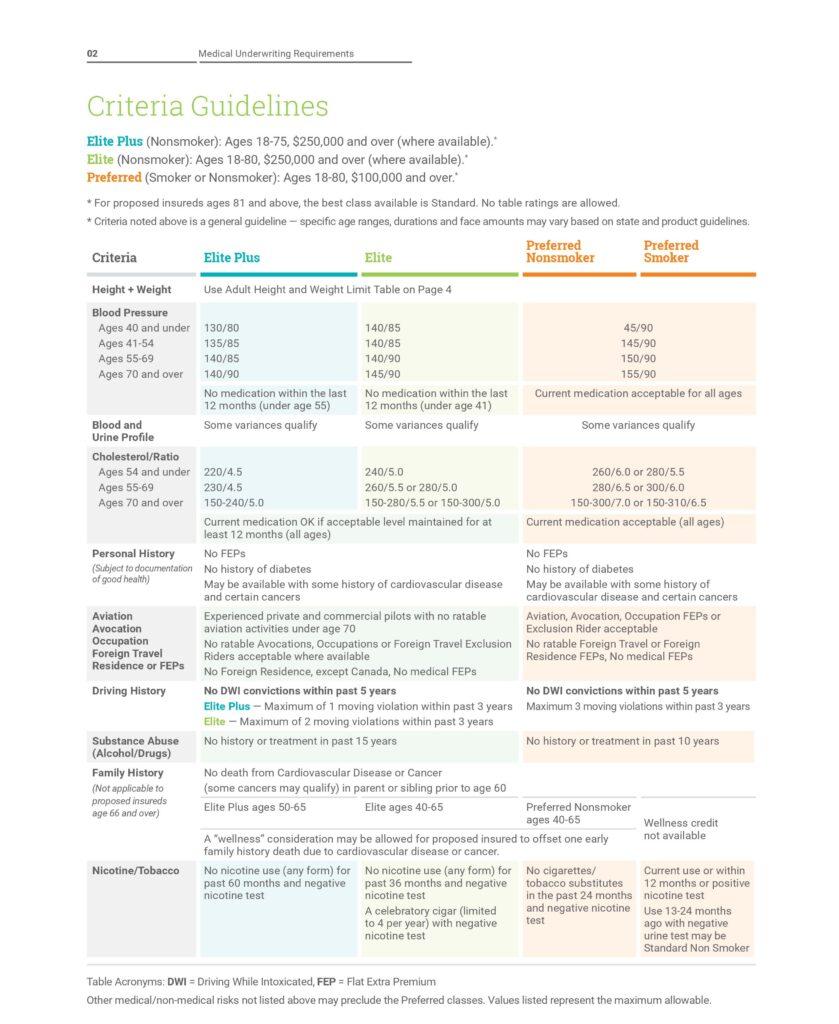

How Do Insurance Companies Rate My Risk?

Similar to a BMI chart, or other indication system,

Burial Insurance providers will assess the risk you pose to them via their own rankings.

This chart is divided into five subsections, indicating an increasing risk the further you descend.

- Preferred plus: This is the category reserved for those in pristine physical condition – you will not qualify for this category if you’re overweight, have pre-existing conditions, or have used tobacco within the last 12 months.

- Preferred: The second highest category, the preferred class is reserved for those that are just barely unable to qualify for preferred plus, such as if you’re barely overweight, have a light tobacco habit, or other like minded factors that will still demonstrate that you’re in good health.

- Standard plus: The middle of the road, where the vast majority of those that apply will see themselves. This section involves moderate-good health, including those with a negative family history or pre-existing condition but are in otherwise great health.

- Standard: The second lowest rating,where someone who is just below the middle ground for a person’s physical status. This is usually the category where the obese, chronic tobacco user, etc., would see themselves.

- Table ratings: The category reserved for those considered “high risk”. This is a rating where your weight, habits, pre-existing conditions, what have you, are not enough to place you here alone. Rather, it’s the culmination of all of the above.

Some conditions will automatically place you in a specific category, as providers will usually place minimum/maximum weight and height restrictions on each rating.

Your age, habits, and pre-existing conditions may also automatically grant you a specific rating.

Important note: Not all providers are the same, some will place emphasis on different aspects and ask you different questions. You may be able to qualify for one provider and not another using the same information.

Sample Chart

Why Is My Weight So Important In The Eyes Of The Insurance Provider?

Your weight directly correlates to your expected life span, with obese/morbidly obese individuals expected to live a lot less then those who are not.

As a result, insurance providers rely on a weight chart, allotting the maximum weights allowed for a specific height/gender.

This aspect of health alone may change the category in which you qualify.

For example, if you are perfectly healthy minus your weight, you may be placed in category 2 vs category 1 based on that alone.

It’s also important to note that being underweight also holds the same “weight” in the eyes of the insurance provider when assessing your qualifications, as being severely underweight will see your rates increase as well.

Male Preferred Plus

| Height | Low | High |

|---|---|---|

|

5’0 |

96 lbs |

151 lbs |

|

5’1 |

99 lbs |

156 lbs |

|

5’2 |

103 lbs |

161 lbs |

|

5’3 |

107 lbs |

166 lbs |

|

5’4 |

110 lbs |

176 lbs |

|

5’5 |

114 lbs |

177 lbs |

|

5’6 |

117 lbs |

183 lbs |

|

5’7 |

121 lbs |

188 lbs |

|

5’8 |

123 lbs |

194 lbs |

|

5’9 |

128 lbs |

200 lbs |

|

5’10 |

130 lbs |

205 lbs |

|

5’11 |

134 lbs |

211 lbs |

|

6’0 |

137 lbs |

217 lbs |

|

6’1 |

142 lbs |

223 lbs |

|

6’2 |

145 lbs |

230 lbs |

|

6’3 |

149 lbs |

236 lbs |

|

6’4 |

152 lbs |

242 lbs |

Female Preferred Plus

| Height | Low | High |

|---|---|---|

|

5’0 |

92 lbs |

148 lbs |

|

5’1 |

94 lbs |

153 lbs |

|

5’2 |

97 lbs |

158 lbs |

|

5’3 |

99 lbs |

163 lbs |

|

5’4 |

101 lbs |

163 lbs |

|

5’5 |

103 lbs |

174 lbs |

|

5’6 |

106 lbs |

180 lbs |

|

5’7 |

107 lbs |

185 lbs |

|

5’8 |

111 lbs |

191 lbs |

|

5’9 |

114 lbs |

196 lbs |

|

5’10 |

114 lbs |

202 lbs |

|

5’11 |

120 lbs |

208 lbs |

|

6’0 |

122 lbs |

214 lbs |

|

6’1 |

122 lbs |

220 lbs |

|

6’2 |

128 lbs |

226 lbs |

|

6’3 |

132 lbs |

232 lbs |

|

6’4 |

136 lbs |

238 lbs |

How Long Does The Underwriting Process Take?

Depending heavily on the underwriting type you were given,

The process can take anywhere from the same day to 2 months/90 days later.

This discrepancy is due in part to the process in place.

A medical exam may require multiple visits, or separate testing locations, to fully verify the information they’re requesting. This can be anything from a complete physical exam to a full analysis of your blood/stool/saliva.

A medical questionnaire is going to be much more lenient, as there is no in person visitation required. In some cases, you can even be approved the same day depending on the provider.

Our Top Picks For The Most Lenient Underwriting

It’s important to discuss options with your experienced licensed agent, as they’ll be able to form a strategy for you moving forward. If you’re unsure where to find the right licensed agent for you, we encourage you to consider Final Expense Benefits.

We at Final Expense Benefits partner with over 20 carriers, with:

Being some of the ones that stand out among the crowd. Reduce the stress involved with life insurance with no waiting period and let us do all of the heavy lifting for you. You can reach us at 1 (866) 311-4338, and we’re open from 9-5, Monday through Friday.

Conclusion

It’s no surprise that medical underwriting can be a stressful endeavor, as your result directly reflects what you’re going to be paying monthly.

Although stressful, the underwriting process doesn’t have to be hard. As long as you’re prepared and comfortable answering the questions you’ll have no issues.

FAQ

What are Medical Underwriting Requirements?

Why Do We Need Insurance Underwriting?

So that the insurance providers may accurately assess your risk level to the company, as well as the rate you deserve to pay.