What Your Family Needs to Be Prepared for if You Die Without Life Insurance

Updated on Jan 10, 2025 • 8 min read

What happens if you don’t have life insurance when you die? Dying without the right life insurance plan in place could put your family in a lot of financial trouble. Between rising funeral costs, skyrocketing mortgage rates, and debt after death, a ton of headaches could head your family’s way when you die.

Help out your loved ones and give yourself some peace of mind as well with a life insurance policy that fits your own unique needs. Check out below to see the effects of death without life insurance.

Call our expert agents at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m., to start picking out the best plan for you and your family. If you want some ideas for where to start looking, check out our free online quoting tool as well.

What Happens If You Don't Have Life Insurance When You Die?

If you die without a life insurance policy, not only will your family members be grieving, but all of the up-front bills such as funeral costs, burial costs, and some medical bills will be on them to pay.

Prices are rising for housing, general household expenses, and funerals; this can put your family in a tough spot following your death.

Try not to put your family in a position to find out what happens if you don’t have life insurance when you die. Give yourself some peace of mind with a good plan and make sure you don’t put them there. Below are a few examples of the types of expenses your family could face following your death:

1

Funeral Costs

The median cost of a funeral with a service in the United States is $7,848, National Funeral Directors Association. Yikes. And that’s just for basic services.

Traditional funerals with a viewing and burial charge median costs around $8,300. This does not include a burial vault, tombstone, and other cemetery costs, and, depending on where you live, costs could easily skyrocket past $10,000.

Cremations are cheaper, as they don’t include burials and other traditional funeral costs. But their median prices are still $6,280 for a funeral with a viewing and cremation.

Experts say to have at least $10,000 set aside for your funeral. That’s exactly why a lot of life insurance plans start at $10,000 payouts. Having a big lump-sum payment ready to go to pay for an up-front cost like a funeral is a great use of a life insurance after-death payout.

But your family will face other issues too.

2

Mortgage Prices

Owning a home is a great point of pride for millions of Americans. But according to data from the United States Census Bureau, over 50 million homes have a mortgage on them.

Per that same data set, the median monthly rate for mortgages in America is $1,904. For any family, losing a source of income is devastating. Having to stretch funds that are intended for recurring bills like mortgages to cover robust up-front costs like funerals will make that even worse.

3

Inflation on General Household Expenses

Of course, something that’s out of your hands is the economy. Rising costs due to inflation could be another factor putting your family in a tough financial place. According to the United States Labor Statistics Bureau, inflation has risen 2.4% from 2023 to 2024.

Inflation will keep on going up year after year, but so can interest rates on a good life insurance policy.

4

Debt After Death

Debts are unfortunately a part of life, and they could hassle your family even after your death. The average debt balance for Americans is $101,915, per data from debt.org. This does include debts from large borrowings like mortgages, but it’s pretty clear that having a fairly substantial debt is pretty common for Americans.

And while you may think that your debts will be cleared following your passing, a lot of lenders actually will ask for repayment from your family. That’s just another cost hounding your family at a tough time.

5

Expenses for Surviving Family Members

We’ve been talking a lot about the expected expenses that your surviving family members will be faced with following your death, but what about unexpected expenses? It just seems like times of great stress (such as losing a family member) can bring one disaster after another.

Your family could face even more up-front costs in the form of emergency expenses. Things like car breakdowns, personal injuries, or appliance issues. And what would be a minor issue at a more normal time of life has the potential to be a major disaster when a ton of other up-front costs are hitting.

The United States Federal Reserve states in their economic well-being survey that 46% of Americans don’t have enough money set aside in an emergency savings fund to cover 3 months of expenses. Furthermore, less than half of Americans responded that they can handle an emergency expense of $2,000 or more using savings.

Even then, according to a Bankrate Survey, 59 percent of Americans reported they were uncomfortable with their level of emergency savings. Dipping into savings meant to cover the long term to pay off up-front final expenses that won’t be covered if you die with no life insurance can be disastrous.

Ways For Surviving Loved Ones To Cover Final Expenses

What happens if you don’t have life insurance when you die? Well, your family will have a few methods to cover your final expenses. However, they may not be enough to cover everything or suitable methods in the first place.

Let’s review some ways that your family can cover themselves in the event you die without life insurance.

1

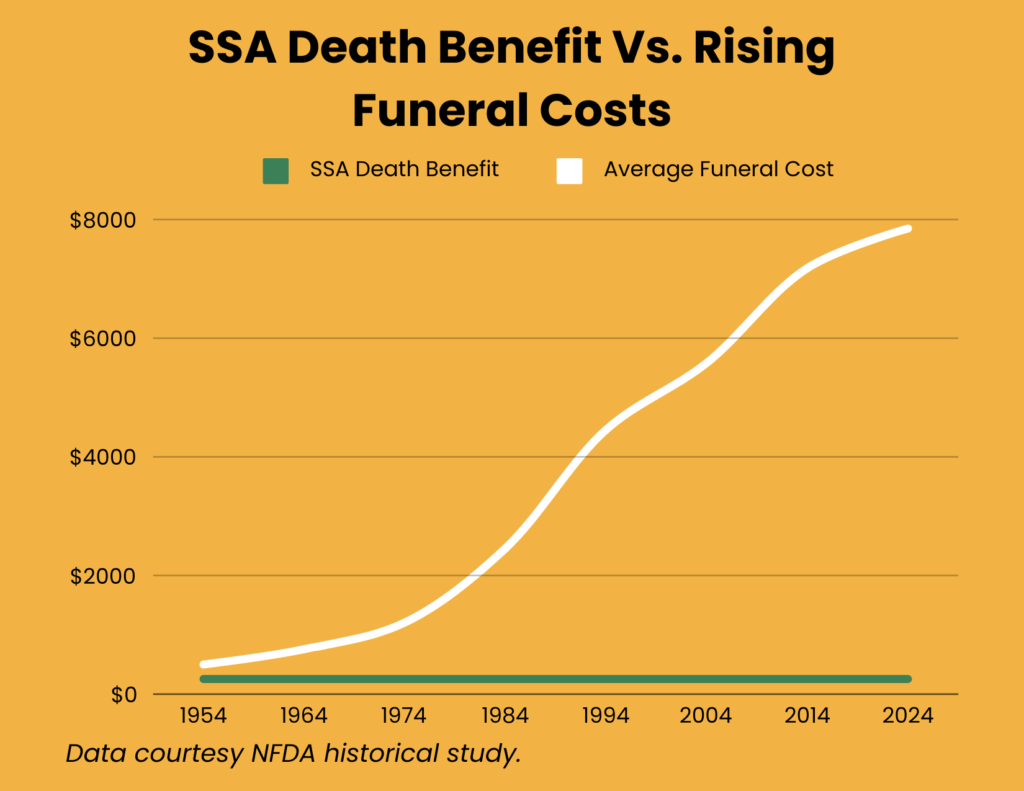

Social Security Death Benefit Payout & Monthly Payments

Social Security is a great tool for covering living expenses after retirement. The Social Security Administration even offers a death benefit payout in the event a retired Social Security recipient passes away.

Sounds great, until you realize that the Social Security Death Benefit payout was set at a paltry $255 in 1954 and hasn’t budged since.

We’ve already talked about rising funeral costs, and you can see the data right above. $255 might be able to get you a small flower arrangement or an urn, but not much else.

Social Security monthly payouts can give your family a replacement source of income. According to the SSA, the monthly average for survivor benefits is $1,509. This is a great source of replacement income, but, again, isn’t quite suitable for covering big up-front costs.

2

Retirement Savings Payouts

Retirement savings are the backbone of post-employment financial planning. However your retirement savings might not be suitable for covering your final expenses. This is due to a number of factors affecting common retirement savings accounts. These include your previous income, the type of savings you have been able to set aside, and the economy’s well-being.

If you structured your retirement savings to drop a big lump sum following retirement, it might help cover your expenses if you die without life insurance. But several plans are set up to deliver smaller amounts of money over an extended period of time, to simulate and replace your monthly income. And that just might not help very much for daunting end-of-life costs.

3

Up-Front Costs vs. Long-Term Payouts

The fact of the matter is that you and your family can be paid out a significant amount of money from sources like Social Security and retirement savings. They’re a great tool for covering your late-life and final expenses, but that’s just what they are: a tool that can fit in and fill a niche in your financial toolbelt.

Social Security payouts and retirement savings are normally intended to be used as long-term income replacement. But because funeral costs are usually up-front, along with a host of other expenses like the ones listed above, these smaller-sum monthly payments may just not be suitable.

And life insurance can fill the gap that these payout methods leave.

What Can You Do To Avoid Dying Without Life Insurance?

It’s not easy to quantify what happens if you don’t have life insurance when you die. But what you should do is simple. Help your family avoid the types of financial issues that come up when loved ones die by choosing a life insurance plan that fits your specific needs.

Customize your coverage and choose the rates, payouts, premiums, and provider that fit your unique requirements. Here’s some information about the types of life insurance we can help you find and how they might fit into your end-of-life plans:

1

Term Life Insurance

Term Life Insurance offers coverage in terms, usually in increments of 10 years, though 5-year increments can also be common.

Term life insurance often will provide the highest payout coverage out of the main types of life insurance and the cheapest monthly premiums relative to the payout. However, term life insurance may also require a medical examination.

Term life is the most difficult policy type to qualify for. As a result, it may not be the best choice for older applicants. We encourage those in good health to review term life insurance possibilities.

2

Whole Life Insurance

Whole Life Insurance is a permanent form of life insurance. It can come in multiple forms, but the most common type involves a fixed monthly premium and lifetime coverage. Whole life insurance payouts also carry a cash value that accrues interest and grows over the life of the policy and policyholder.

Whole life insurance also often does not require a medical examination or a questionnaire. This could make it a good choice for older applicants.

3

Final Expense Insurance

Final expense insurance is a type of life insurance specifically intended to cover end-of-life expenses, like funeral costs. Final expense insurance involves an application and approval process; unlike certain other life insurance plans, your family will be entitled to the payout immediately, no matter when you die.

While final expense insurance is usually used to cover funeral and burial costs, beneficiaries can use the funds however they would like. It is normally classified as a simplified-issue plan, which means that you are almost always approved regardless of any underlying medical conditions.

Final expense insurance premiums are usually low, and last for your whole life, which means that the rate doesn’t change over the policyholder’s lifetime. Depending on your total asset values, you could even have a final expense insurance policy if you benefit from Medicaid.

4

How Much Does Life Insurance Cost?

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more.

Conclusion

It’s clear that dying without life insurance isn’t going to do your family any financial favors. In fact, it can put them in a really bad situation, depending on your total savings. Utilize life insurance as a tool to fill the gaps between your other assets to help put your family in the best financial position following your death.

We can help you out with finding the right plan. Give us a call at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m., or check our free online quoting tool and start your journey to giving yourself and your loved ones peace of mind.

FAQ

What happens if you die without life insurance?

Your family is stuck with the bill for your funeral costs, certain medical bills, and debts. They’ll also be liable for recurring payments such as mortgages and household expenses.

What are some funeral costs my family may need to cover if I die without life insurance?

Many funeral homes charge a variety of fees for funerals, including service fees, embalming prices, body preparation for viewing, use of a hearse, caskets, and more. These costs can easily add up, putting your family on the hook for more than $10,000 if you die without life insurance.

What can you do if you don’t have life insurance?

First, take stock of all your assets and determine where life insurance fits in. Life insurance can be a great tool to fill in the gaps of what types of retirement or emergency funds you already have. Then contact a trusted source like Final Expense Benefits to learn more about life insurance and how the right plan can help you and your family.

How can you prepare surviving loved ones for final expenses?

You can prepare your surviving loved ones using several of the financial tools we’ve discussed above. Social Security death and survivor benefits, retirement investments, and a good life insurance plan will give your family what they need to face final expenses or emergencies with confidence.