Top 10 Reasons to be Denied Life Insurance (And What to Do About it)

Updated on Apr 8, 2025 • 6 min read

Most who have been denied life insurance coverage are surprised when the agent or company reveals their decision. Even if your life insurance application has been rejected, you still have options. What are the reasons you may be denied life insurance? What can you do if you have been denied? Final Expense Benefits discusses the top reasons why you may be denied coverage and what you can do about it.

Continue reading to learn more about why you may be denied life insurance and what to do should this happen to you. Our team of expert agents is available at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET. Our free quoting tool is available for you to receive a free estimate at any time.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

Top 10 Reasons to Get Denied For Life Insurance

If you do not keep up with your payments, it can be difficult to reinstate your policy. Policy reinstatements include higher monthly premiums than your original policy.

1

Serious Medical Condition

Serious conditions such as cancer, Lou Gehrig’s Disease, and Multiple Sclerosis are likely to get you denied life insurance. Underwriters consider people with these conditions to be high-risk applicants. Some moderate conditions that can be reversed or reduced, such as obesity, may not result in an automatic denial.

Failure to disclose this information could result in your application being rejected. Underwriters may contact your healthcare providers to confirm the information on your application.

2

Being Untruthful or Withholding Information on an Application

When applying for insurance, it is crucial to be truthful. It is one of the reasons why life insurance policies require applicants to complete a medical exam. An important aspect of the underwriting process includes taking the information you’ve shared about your medical history and lifestyle to determine your premium based on the chance of you potentially passing while covered.

You might think it’s not significant to claim you quit smoking years earlier than you did. However, if you were to pass away and the insurance company discovers this discrepancy in your application, they could refuse to pay your claim. While life insurance for smokers may be more expensive, it is worth being truthful in the long run, as you will not risk your claim being denied due to false information.

3

Age

Life insurance companies have a specified limit on the ages they will cover. You may be denied life insurance due to advanced age, making it crucial to apply as early as possible. If you apply for a whole life insurance policy at a younger age, you can lock in a lower rate and guarantee coverage.

Insurance companies are less likely to insure an older applicant as they are more likely to have health problems. If you have applied for life insurance and have been denied due to age, a term life insurance policy may be the best alternative.

4

Involvement In Illegal or Criminal Activity or Death Due to Criminal Activity

The insurance company can refuse payment if you pass away while involved in illegal activity. Your insurer won’t issue the coverage or benefit at all if you are proven to be someone who abuses drugs.

Having a criminal record could result in you being denied life insurance. However, the outcome will depend on the company you have applied for coverage with. Those who have committed more serious crimes or are repeat offenders are at a higher risk of being denied than a one-time offender.

Individuals charged with a felony should note that it is important to wait until after the proceedings and your sentence is complete before applying for life insurance. If you apply for insurance while serving prison time, your application will be denied. Final Expense Benefits works with various companies that provide insurance policies for inmates.

5

Hazardous Occupation

Some careers are more dangerous than others and could result in your life insurance application getting denied. Insurance companies will look at the mortality rate within the line of work and may deny your application. Examples of hazardous jobs include the following:

- Police Officers

- Pilots

- Truck Drivers

- Roofers

- Iron and Steel Workers

If you work in one of the careers listed above, you may have difficulty obtaining life insurance. However, you can speak with your employer about your options, as most of these careers may offer some type of coverage.

6

Financial Reasons

When applying for life insurance coverage, the provider will look at your income and net worth to determine the amount of coverage you can apply for. For example, an individual earning $30,000 a year will have difficulty getting approved for a $5 million life insurance policy. The risk to the insurer is too high.

7

Previous Denials

Life insurance companies share information with a repository called the Medical Information Bureau (MIB). This will contain information about you, including your health history, medications prescribed, and how many life insurance companies you’ve applied for coverage with.

It can hurt your application if your report shows that you have applied at various life insurance companies and were denied coverage.

8

Alcoholism

Having a chronic issue with alcoholism can be a strong case for denial. Having a few glasses of wine with dinner will not result in your application being denied, however, it is important to note that during the medical exam, your blood will be tested, and the doctor will be able to determine whether or not you have higher-than-average levels of alcohol consumption.

Alcoholism is detrimental to your health, and many chronic health issues can be linked to alcoholism, so underwriters will typically deny life insurance to those with alcoholism.

9

Positive Drug Test

Life insurance companies will test your blood and urine during your initial exam. Testing positive for illegal drugs can cause an immediate denial of life insurance. You will most likely be denied coverage if you test positive for any of the following drugs:

- Amphetamines

- Barbiturates

- Benzodiazepines

- Cocaine

- Marijuana

- Methadone

- Methamphetamine

- Nicotine

- Opiates

- PCP

Some of these drugs listed can be prescribed or obtained legally, however, it can still hurt your chances of being approved for coverage if you are found to have tested positive.

If you are denied life insurance because of your prescription medication, you can ask your doctor to write a letter explaining why you need the prescription. However, even if you obtain the note, insurance companies may still see you as a high-risk applicant and deny you coverage. If you are a smoker, you may not immediately be denied life insurance coverage, but your premium rates may be higher.

10

Dangerous Hobby

If you are someone who enjoys participating in various activities that could be considered dangerous, you may be at risk of being denied life insurance. Insurance underwriters seek to insure those who present the smallest risk possible. Engaging in risky activities, including the following, may put you at risk of being denied coverage:

- Motocross

- Skydiving

- Hang gliding

- Rock climbing

- Aviation

The more you participate in these activities, the more likely you are to be denied life insurance. However, if you have been trained or have a license, the insurance companies will see that you are serious about your safety. This may prevent you from being denied altogether and can minimize the amount you pay.

Other Reasons Why You Were Denied Life Insurance Coverage

Policy Expiration

Life insurance coverage falls under two main categories: term and whole life. A whole life insurance policy covers you for life as long as the premiums are paid. Term life insurance lasts a pre-determined amount of time. Once it expires, you must purchase a new term life plan, which will become more expensive as you age.

If you had a 20-year term policy and passed away during the coverage period, the insurer would disburse your death benefit. Once your term policy expires, the coverage expires. You can purchase a new term policy once the old policy expires, but it will be more expensive.

Policy Lapse

A policy lapse is another factor that can lead to a life insurance payout denial. This occurs when premium payments are not made. As a result, the insurance company might cancel your policy, leaving you unprotected. However, some insurers might provide a brief grace period for policyholders to settle their outstanding payments. Your coverage remains intact during the grace period, which can run from 30 to 90 days.

How To Appeal A Denied Life Insurance Claim

Get Information About Why You Were Denied and Review It

If you have been denied life insurance, you can appeal the decision, however, there are a few things you can do to increase your chances of successfully appealing for life insurance. Final Expense Benefits agents can help you navigate your next steps after being denied life insurance coverage. Our talented agents are available at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET.

What To Do When You Have Been Denied Life Insurance Coverage

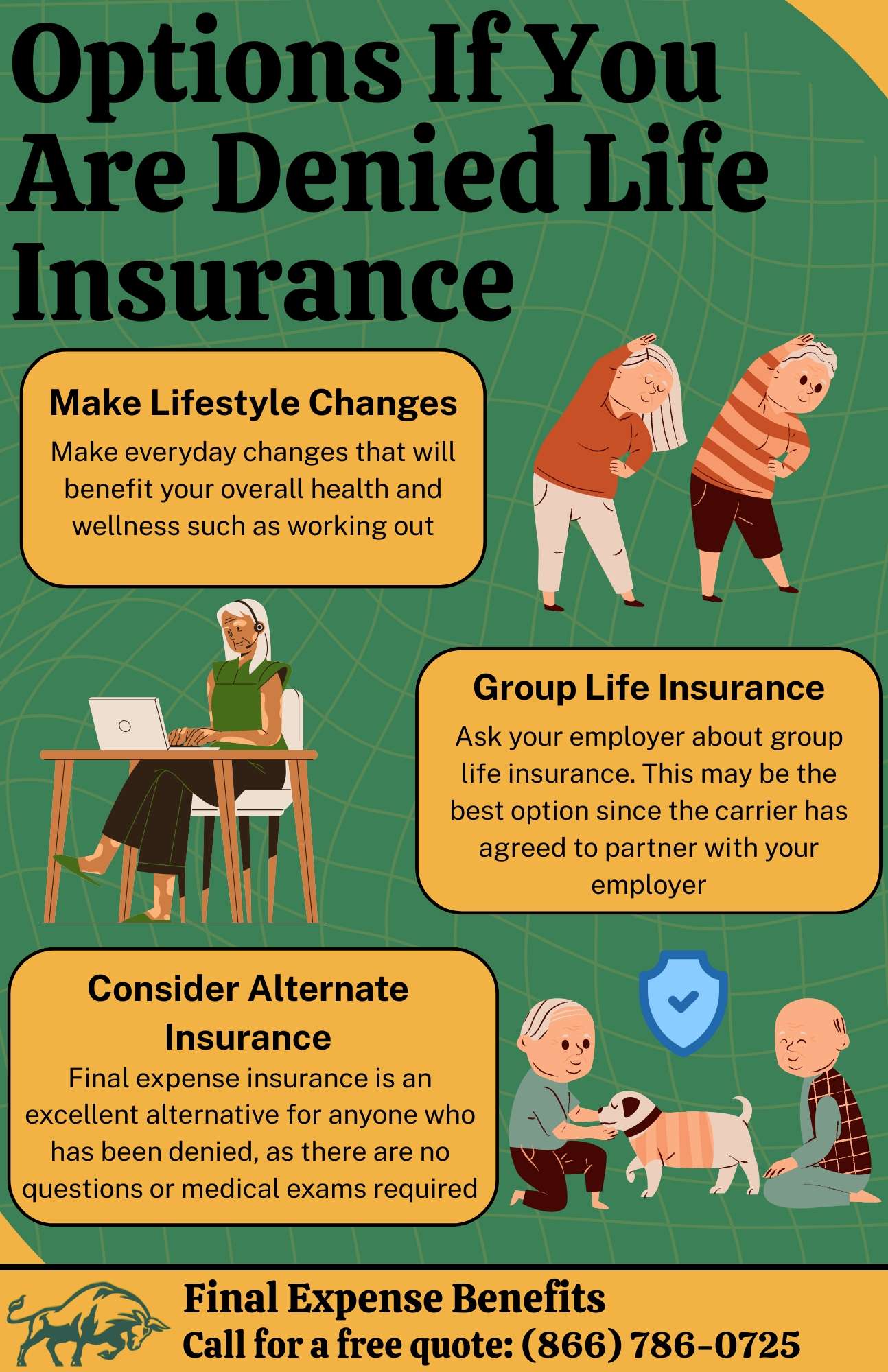

1

Make Lifestyle Changes

If your life insurance application is denied, the first thing you can do is make everyday changes that will benefit your overall health and wellness. Underwriters want to insure people they deem as low risk. To make yourself more appealing to underwriters, you can start by making healthy decisions. Eating well and exercising are great ways to improve your health and lower your weight, as weight is a factor for underwriters.

It is imperative to include any steps you are taking to improve your health, such as being part of a weight-loss program or obtaining a gym membership. Life insurance for overweight individuals can be more expensive, but Final Expense Benefits can help you find a plan that provides comprehensive coverage at a fair rate. Our talented agents are available at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET.

Another way to make yourself a lower-risk applicant is to take steps toward decreasing your alcohol consumption and smoking. This may not be accessible to everyone, as pre-existing conditions can make this challenging. However, making small changes over time can be helpful when looking for life insurance.

2

Ask Your Employer About Group Life Insurance

Group life insurance is available for most full-time workers through their employer. Typically, it does not require you to complete a medical exam, so it is preferred for those with medical issues.

While group life insurance may not fully meet your insurance needs, it can be a great way to get coverage. This may be your best option since the carrier your employer works with understands the difficulties of the job and has agreed to partner with your employer.

3

Consider an Alternative Form of Insurance

Final expense insurance, or burial insurance, is an excellent alternative for anyone who has been denied life insurance, especially if you have been denied due to advanced age or health issues.

To obtain a final expense policy, you will be required to answer a few general questions, but you will not be required to complete a medical exam. Most final expense companies specialize in working for seniors, so you can ensure that you and your remaining expenses are covered should you pass away.

Options If You Are Denied Life Insurance

Best Burial Insurance for When You Are Denied Life Insurance

$10,000 coverage policies have affordable premiums for the life of the policy. Final Expense Benefits only works with top-rated carriers for all your final expense needs. If you are denied life insurance, you can still find coverage with any of our top-rated insurance companies.

Below is a chart of some of our top-rated partners. Our expert agents are available to help you find a plan that provides protection for you and your loved ones. Our agents are available at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET.

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

Conclusion

Final Expense Benefits partners with over 20 carriers, with many providing options that do not require a medical exam. Our expert agents are available to help and can assist in finding alternative insurance should you be denied. Some of our carriers include:

Our team of expert agents is available at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET to help you find the perfect plan for you and your loved ones. Our free quoting tool is available for you to receive a free estimate at any time.

FAQ

Can Life Insurance Be Denied?

Life insurance can be denied for a variety of reasons. Whether you have a serious medical condition, financial issues, or have previously been denied, you may find your life insurance application denied.

Can Life Insurance Be Denied For Drug Use?

Illicit drug use can result in an immediate denial of life insurance. Providers will examine your urine sample to see if you test positive for any drugs. It is important to note that drugs that can be prescribed legally can still be a threat to your application.

Can A Life Insurance Claim Be Denied For Alcohol Use?

Yes, a life insurance claim can be denied for alcohol use. Having a chronic issue with alcoholism could be a strong case for denial. During the medical exam, they draw blood and run tests to indicate whether or not you have higher-than-average levels of alcohol consumption. Chronic health issues almost always coincide with alcoholism.