Brighthouse Life Insurance Reviews: Not Ideal For Final Expenses

Updated on Feb 13, 2026 • 8 min read

Brighthouse Life Insurance broke away from MetLife Insurance in 2017 and offers customers only a select number of life insurance products. How is the company doing now, and are their products worth the cost? Despite meeting financial obligations as a business, current Brighthouse Life Insurance reviews do not paint the company in a good light. So, if you’re a senior applicant looking for final expense coverage, you may struggle to find proper insurance with the company due to extremely limited whole life options and strict underwriting.

Call Final Expense Benefits at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET, to learn more about Brighthouse Financial Life Insurance, or check out our online quoting tool to see what other providers are currently offering applicants.

Key takeaways

- Brighthouse Insurance offers products such as term life and indexed universal life insurance, and numerous riders, providing flexible options for applicants.

- Brighthouse also offers several annuity contracts, providing alternative retirement investments for final expenses.

- While third-party ratings are minimal, Brighthouse has a decent track record in terms of accreditation and their ability to meet long-term financial obligations.

- Customers share an overwhelmingly negative view of Brighthouse Life Insurance.

History of Brighthouse Financial

Brighthouse Financial was originally formed in 2017 thanks to foundational work placed by insurance providers Travelers and MetLife. However, in January 2016, MetLife announced that it would separate a significant portion of their life insurance and annuity entities. The establishments marked for separation included Brighthouse Life Insurance, the Brighthouse Life Insurance Company of NY, and the New England Life Insurance Company. They are currently headquartered in Charlotte, North Carolina.

Brighthouse Life Insurance Options

Brighthouse Life Insurance also offers a few traditional coverage options for applicants seeking a policy: indexed universal, term life, whole life, and a collection of life insurance riders offering more customization.

Brighthouse Indexed Universal Insurance

Indexed universal life (IUL) insurance is a type of policy with adjustable rates that provides a cash value component along with a death benefit. Under Brighthouse Insurance, people can apply for the SmartCare and SmartGuard Plus plans.

SmartCare is a hybrid life insurance product that combines traditional coverage with long-term care (LTC) benefits. The plan is offered to applicants between the ages of 40 and 75 because medical exams are not required for most (cognitive screening for those aged 66 and older; medical records checked for significant conditions). For seniors, indexed universal life insurance can provide permanent life coverage with flexible payment options for premiums.

Brighthouse Term Life Insurance

Term life insurance only covers policyholders while the plan is active, usually in five-year increments. Typically, at the end of a term, the insured can renew the plan at any time.

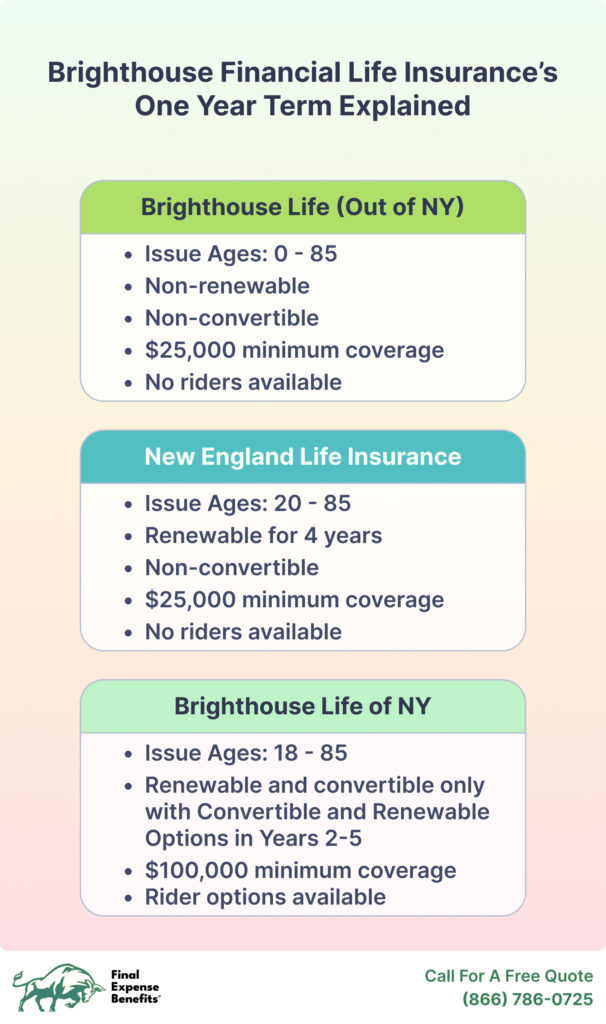

With Brighthouse Life Insurance, term life is offered through the Brighthouse One Year Term. As the name implies, the company offers one-year terms with issuing ages capping out at 85. However, depending on where your policy was originally issued, the features of your plan will change:

- Brighthouse Life Insurance: non-renewable; non-convertible; $25,000 minimum coverage; no riders available

- New England Life Insurance: renewable for four years; non-convertible; $25,000 minimum coverage; no riders available

- Brighthouse Life Insurance of New York: only available in New York; can be renewed up to five times; can be converted into a whole life plan with an insurance rider; $100,000 minimum coverage; smoking status will influence premium rates

If you’re a senior applicant looking for a stable, more traditional plan to cover final expenses, call Final Expense Benefits at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET.

Brighthouse Life Insurance Riders

In short, insurance riders grant policyholders customization options for their coverage plan, usually at additional cost. Brighthouse Life Insurance offers several life insurance riders and, depending on which plan you apply for, may include some riders for free. Some of those free and add-on insurance riders include the following:

- Long-Term Care Acceleration of Death Benefits: included in Brighthouse Financial’s SmartCare coverage; allows you to access up to 98% of your policy’s face amount to pay for long-term care expenses at the cost of reducing your death benefit amount.

- Return of Death Benefit: included with Brighthouse’s SmartCare plan; guarantees that a policyholder’s death benefit will never be less than 100% of the premiums paid.

- Guaranteed Distribution: required to pay additional charge; guarantees distribution payments in the form of policy loans from your plan’s cash value component for a specific period.

Interested in learning more about insurance riders? Final Expense Benefits has you covered—read more about it here and get familiar with how you might be able to customize your plan today.

Does Brighthouse Have Whole Life Insurance?

There is no accessible method to apply for and purchase a whole life policy directly unless you have a New York term life coverage with the company. With that NY-exclusive term life policy, you’ll be able to convert it into a whole life policy—a permanent form of life insurance—with a conversion rider.

Brighthouse Financial Annuities

Much like life insurance policies, annuities can serve as an alternative method of providing a stable income for retirees. Aside from providing financial support for seniors, they can turn earned assets into consistent payouts later in life.

At Brighthouse, several annuity options are available for purchase: fixed index annuities, registered index-linked annuities, and variable annuities. Here’s what the company has to offer:

- SecureKey: fixed indexed annuity; available for anyone under age 80; minimum premium of $25,000

- Shield Level II/Shield Level Pay Plus II: registered index-linked annuities; $25,000 minimum contribution; no surrender schedule for base offerings

- FlexChoice Access: variable annuity; promises 5% annual compounding growth; can also apply Brighthouse’s FlexChoice Access—a living benefit rider that can offer guaranteed income for surviving beneficiaries if you pass away

If you’re interested in a more reliable form of final expense coverage, then consider contacting Final Expense Benefits at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET, to learn more today.

Alternative Final Expense Insurance Providers

Final expense insurance is a specialized whole life plan meant to cover end-of-life expenses while offering level rates and cash value growth potential.

If you’re a senior applicant looking for an insurance plan for funerals, cremations, or even outstanding debts, consider a final expense policy. Here are some of the current market’s top-rated providers across the US:

Sample $10K Burial Coverage Plan Rates

| Company |

Male 50y/o |

Male 60y/o |

Male 70y/o |

Female 50y/o |

Female 60y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$51 |

$73 |

$27 |

$41 |

$58 |

|

|

$31 |

$43 |

$71 |

$26 |

$35 |

$53 |

|

|

$37 |

$50 |

$75 |

$26 |

$37 |

$55 |

|

|

$31 |

$44 |

$75 |

$24 |

$33 |

$53 |

|

|

$34 |

$45 |

$79 |

$29 |

$35 |

$59 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

The Pros and Cons of Brighthouse Life Insurance

Pros

- Coverage decisions in 24-hours

Typically, agents working for Brighthouse Life Insurance will get back to you within 24 hours to tell you if you are qualified for their life insurance.

- Online educational resources available

Brighthouse Life Insurance provides open access to educational resources for learning more about annuities, insurance, estate planning, and more.

Cons

- Limited whole life coverage options

The only way to get a Brighthouse whole life policy is exclusive to New York, where you can convert your term life policy using an insurance rider.

- Strict underwriting process

Qualifying for a life insurance policy with Brighthouse will be difficult since there are no whole life or final expense options. - No online quote tool, no online application

If you’re looking for information on monthly premiums or applying for coverage, you’ll have to contact a financial professional. - Overwhelmingly negative customer reviews

Across multiple sites, including third-party rating services, Brighthouse Life Insurance customers have regularly cited poor customer service and repeated mishandling of customer payments.

Brighthouse Life Insurance Reviews: Third-Party Rating Services

AM Best

1

Through their annual findings, AM Best has helped consumers by evaluating companies’ overall financial strength and their ability to run their business in good faith.

As of November 2025, the Brighthouse Financial Life Insurance Company has not received a financial strength grade. However, they did receive a Long-Term Issuer Credit rating of “bbb+”, showing a good score of confidence in a business’s ability to meet their ongoing financial obligations.

BBB

2

Helping customers by identifying trustworthy businesses, the Better Business Bureau (BBB) tracks customer complaints and helps resolve disputes.

Brighthouse Financial Life Insurance is a BBB-accredited company as of November 2025. Additionally, Brighthouse currently holds an A+ rating; however, customer reviews of the company filed with the BBB yield an average customer rating of 1.00/5.00 stars.

NAIC

3

The National Association of Insurance Commissioners (NAIC) is responsible for reporting annual findings of companies’ customer complaints.

As of 2024, the Brighthouse Financial Life Insurance Company has a 0.35 consumer complaint index score, indicating that they received less than half the annual average of customer complaints compared to other life insurance companies.

Brighthouse Life Insurance: Customer Reviews

Nancy S

1/5

“This company claimed it would pay out the money it owes me for my annuity on October 15, 2025. I’ve made multiple calls to their “customer service” department, but they don’t have any idea what happened to MY money. It’s a lot of money, so it looks like I have to sue.”

Christen H

1/5

“This companies customer service is AWFUL!! You can hardly understand the […] and when you ask to be transferred to a supervisor they drop the call. It’s happened 3 times. And this is like the only company that does not ask you to take a survey after each call. I will be letting my policy lapse and go with another life insurance company like […] Their customer service has been fantastic.”

Craig M

1/5

“I have a life insurance policy with Brighthouse.. (had for 8 years) and when asked how I can access the account online, they said “you can’t”. WHAT?? What kind of archaic system do they have??? Does not give me any comfort on how my family will access the funds upon my passing!! Wow. And when calling their customer service #, they had to pass me through “several departments” before I was able to talk to a live representative (who I could barely understand). Seriously considering dropping them…”

Final Thoughts

If you or a loved one plans to apply with Brighthouse for final expense coverage, then you may want to consider a different provider, as whole life options here are extremely limited. And according to policyholders in Brighthouse Life Insurance reviews, the company’s ability to provide quality service and help with customers’ needs a lot of improvement. Brighthouse’s main focus is selling life insurance and annuity contracts, which do not provide long-term coverage.

In the market for a whole life policy? Don’t forget to call Final Expense Benefits at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET, or get personalized quotes with our free online quoting tool.

FAQ

Where is Brighthouse Life Insurance located?

Brighthouse Life Insurance is currently headquartered in Charlotte, North Carolina.

Who owns the Brighthouse Life Insurance Company?

Chuck Chaplin currently serves as Chairman, while Eric T. Steigerwalt operates as the company’s Chief Executive Officer.

Are MetLife and Brighthouse Life Insurance the same?

MetLife and Brighthouse Financial Life Insurance are not the same. MetLife established Brighthouse Financial Life Insurance, but officially separated from the company in 2017 and has operated as an independent company since.

Is burial insurance worth getting?

Burial insurance is a form of permanent life policy with level rates that can cover end-of-life coverage. So, if you don’t want to pay out of pocket following a death, you may want to consider investing in a good burial insurance plan.