Understanding Life Insurance Cash Value for Seniors and Families

Updated on June 5, 2025 • 7 min read

Some life insurance policies offer a way to accrue limited cash savings in addition to benefit payouts. This savings is called life insurance cash value, and it’s a great way to add financial flexibility to your coverage. Not all policies offer life insurance cash value, but those that do often work great for seniors.

At Final Expense Benefits, we specialize in final expense insurance. Also known as burial insurance, this type of permanent life insurance gains cash value over time, while providing affordable and accessible coverage to seniors.

To learn more about your life insurance options, call Final Expense Benefits today at (866) 786-0725. Our expert agents are available to answer your questions Monday through Friday, 9 a.m. to 5 p.m. ET, and our free online quoting tool is available 24/7 for a quick, personalized pricing estimate.

What is Cash Value Life Insurance?

Cash value life insurance is a type of permanent life insurance that includes a savings component. This cash value grows over time and is a great living benefit to life insurance – it can be used while you’re still alive. Cash value growth is one of the key differences between term and permanent life policies.

All permanent life insurance policies offer cash value growth, locked-in payment schedules, and coverage for the rest of your life, as long as premiums are paid.

How Life Insurance Cash Value Works

Your policy’s cash value grows each time you pay your premium. Here’s how it works:

- Each time you pay your monthly premium, a portion is used to build the policy’s death benefit payout.

- Another portion goes to the insurer to pay for their management fees.

- A third portion is sent to a cash value account included in the policy. This account is managed similarly to a high-yield savings account.

- Life insurance cash value growth is tax-deferred and may include interest, dividends, or investment returns (depending on the policy type)

Here is a chart depicting an example of whole life insurance cash value growth for a policy in effect for 55 years:

| Policy Year | Age | Annual Premiums | Cash Value |

|---|---|---|---|

|

5 |

40 |

$1,178 |

$3,738 |

|

20 |

55 |

$1,178 |

$33,838 |

|

35 |

70 |

$1,178 |

$99,839 |

|

55 |

90 |

$1,178 |

$289,301 |

These values are examples only, calculated using a $100,000 whole life policy and sourced from Investopedia.

How to Access Life Insurance Cash Value

Steps for accessing life insurance cash value differ by insurer. Generally, you should start contacting your insurer for available cash value life insurance options. They’ll inform you how much cash value your policy has accrued and let you know your next steps.

Most companies require policyholders to fill out a form online or by mail. Policyholders typically use their life insurance cash value for withdrawals, loans against their policy, or to add to their death benefit.

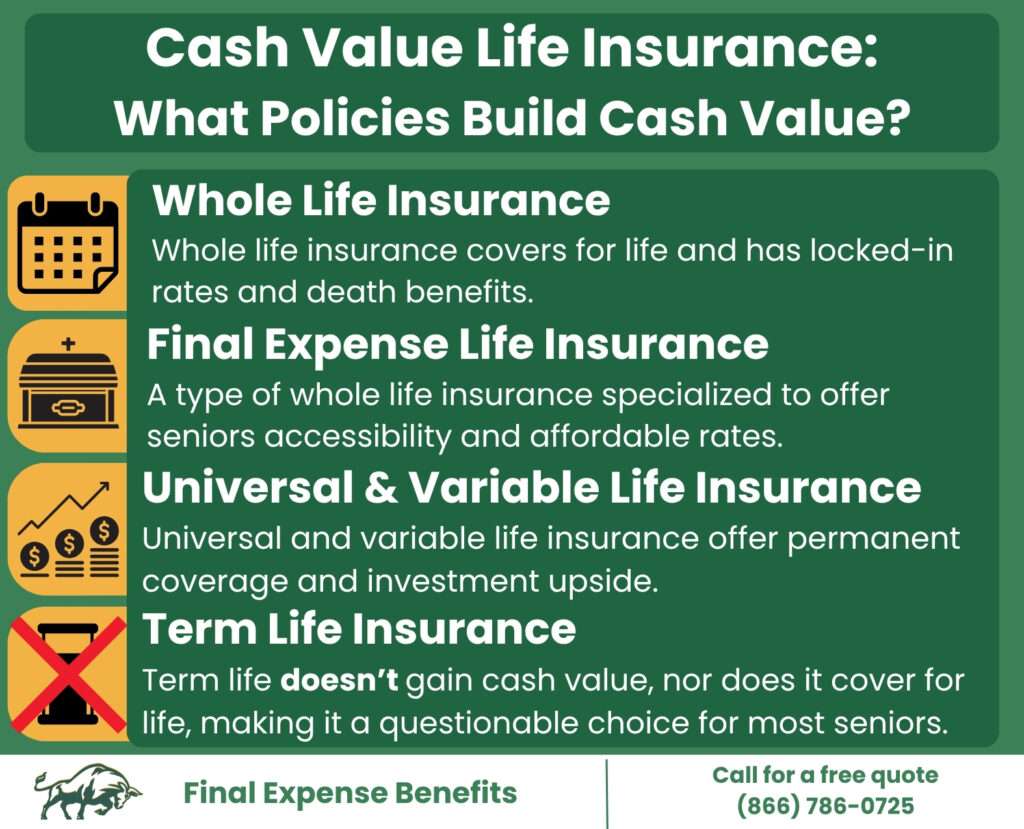

What Life Insurance Has Cash Value?

Not all life insurance builds cash value. Below is an overview of the most common types of life insurance and how they grow in cash value:

1

Whole Life Insurance Cash Value

Whole life insurance is trusted by many seniors for its cash value growth, reliability, locked-in benefits, and permanent monthly premiums. However, seniors may have limited access to traditional, high-value life insurance policies because of strict health underwriting requirements and high premiums.

2

Final Expense Life Insurance Cash Value

Final expense insurance is a whole life policy designed specifically for seniors. These policies feature smaller death benefits (typically between $5,000 and $50,000) and have more lenient health screening requirements.

Although the cash value grows more slowly than traditional whole life insurance, it provides useful financial flexibility. Final expense policies often allow seniors with pre-existing health conditions to get coverage, including those who may not qualify for other forms of insurance.

Guaranteed final expense policies are available to seniors confined to nursing homes or with major pre-existing conditions like cancer, dementia, or terminal illness. Rates are normally 25% to 40% higher than comparable standard final expense policies, and guaranteed policies always have a waiting period. If the policyholder dies during the waiting period, payouts may be reduced or paid in a modified structure. However, these policies are sometimes the only way seniors with serious health concerns can get coverage, and they still build cash value.

No matter your health conditions, final expense insurance can be a great choice for seniors looking for quality coverage. Many seniors qualify for policies with no waiting period at great rates.

3

Universal Life Insurance Cash Value

Universal life insurance is another form of permanent life insurance. It offers more flexibility than whole life, allowing policyholders to adjust their premiums and death benefits. Universal life insurance cash value grows based on interest rates or market performance.

While the potential for cash value growth is higher, so are the risks. These policies are typically better suited for individuals who understand financial markets and are comfortable with variable returns. They also tend to have higher premiums and stricter underwriting, making them less accessible to many seniors.

4

Variable Life Insurance Cash Value

Variable life insurance allows the cash value to be invested in mutual funds, stocks, and bonds. The performance of these investments directly affects the growth of your cash value, which means you could experience high returns or significant losses.

Because of this uncertainty and the financial knowledge required to manage the policy effectively, we don’t normally recommend variable life insurance to seniors. It’s built for younger policyholders with investment experience and higher risk tolerance.

5

Term Life Insurance Cash Value

Term life insurance only offers coverage in set periods, usually in 10 to 30-year periods. These policies typically have low rates and do not build any cash value.

If you outlive the policy term, the coverage ends, and you receive no payout or savings. For this reason, term life is often more suitable for young adults looking to protect their income or provide for dependents. Health requirements are usually strict and may exclude seniors from coverage.

What You Can Do With Life Insurance Cash Value

Once your policy has built cash value, you have several practical ways to use it:

- Pay your premiums

Some policies allow you to use cash value to cover future premium payments, easing your monthly financial burden. - Take out a loan

You can borrow against your cash value, often at low interest rates. If not repaid, the amount will be deducted from your death benefit.

- Withdraw funds

You can remove part of the cash value directly. This differs from a loan and will reduce your death benefit accordingly. - Surrender your policy

If you no longer want the coverage, surrendering the policy allows you to receive its full cash value (minus fees). - Sell your policy

Some third-party buyers may offer a lump sum to purchase your policy, which can be a good option if you no longer need the death benefit. - Buy an annuity

Using a tax-free 1035 exchange, you can convert your cash value into an annuity that provides guaranteed income for life. - Increase your death benefit

Many insurers allow you to use the accumulated cash value to buy more coverage, boosting your policy’s payout.

While cash value life insurance offers unique ways to grow and access money over time, it’s not the right fit for everyone. Below are the key pros and cons to help you decide if cash value life insurance meets your needs.

Cash Value Life Insurance Pros & Cons

Cash value life insurance can be a powerful tool for long-term financial planning, especially for those looking to leave behind more than just a death benefit. However, while these policies offer lifelong coverage and a savings component, they also come with higher costs and more complexity. Before choosing cash value insurance, it’s important to understand the benefits and drawbacks to make the best decision for your family and your future.

Pros

- Lifetime coverage

Cash value life insurance policies don’t expire as long as premiums are paid. - Tax advantages

Cash value grows tax-deferred, and death benefits are paid out tax-free. - Access to funds

You can use the cash value for emergencies, premiums, or other needs. - Potential to increase benefits

Accumulated cash value can be reinvested into your policy.

Cons

- Doesn’t pay out automatically

Unless you arrange otherwise, cash value is typically kept by the insurer when you pass. - Slow growth

It can take many years before your cash value becomes significant. - Higher costs

Premiums for whole life policies are usually higher than term life policies, though they are often more accessible for seniors.

Who Should Consider Cash Value Life Insurance?

Cash value life insurance is often a good fit for seniors looking for permanent, predictable coverage and to build savings within their policy. Final expense policies always include cash value growth, and they can be a great choice for seniors with pre-existing conditions or searching for affordable, quality coverage.

One of the main reasons why we recommend final expense insurance so much is the low price. Below are sample quotes for a benchmark $10,000 burial insurance policy from some of our top-rated providers. These quotes are calculated using a non-smoking applicant with no pre-existing health conditions:

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more or check our free funeral calculator to see how much coverage you need for your end-of-life expenses.

Final Thoughts

Cash value life insurance is more than just a policy — it’s a long-term financial tool. Typically great for seniors, cash value life insurance policies offer protection, savings, and flexibility, particularly for seniors planning ahead.

At Final Expense Benefits, we’re here to help you find the right policy for your needs. Whether you’re just starting to explore your options or ready to compare quotes, we partner with top-rated providers to make the process easier.

To learn more, call us at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m. ET, or check our free online quoting tool for a personalized pricing estimate.

FAQ

Are life insurance cash value withdrawals taxable?

In most cases, cash value withdrawals are not taxable as long as the amount withdrawn is less than or equal to the amount you’ve paid into the policy (your “cost basis”). However, if you withdraw more than your total premiums paid, the excess may be taxed as income. Loans against the cash value are typically not taxed, but if the policy lapses or is surrendered, the loan balance could become taxable.

Can Medicaid take life insurance cash value?

Yes, in some cases. Medicaid may count the cash value of a life insurance policy as an asset, especially for policies with a face value over $1,500.

How does life insurance cash value work?

Cash value is a savings-like feature included in many permanent life insurance policies. Here’s how it works:

- A portion of each premium you pay goes into a cash value account

- This account grows tax-deferred, often at a fixed or variable interest rate

- You can access this money while alive through loans, withdrawals, or by surrendering the policy

- Any unpaid loans or withdrawals reduce the death benefit paid to your beneficiaries

What life insurance has cash value?

Only permanent life insurance accrues cash value. This includes traditional whole life insurance, final expense insurance, guaranteed life insurance, universal life insurance, and variable life insurance.

What life insurance has no cash value?

Term life insurance doesn’t accrue cash value.

What is final expense insurance?

Final expense insurance is whole life insurance designed to help seniors cover end-of-life expenses like funerals and burial plot costs.