Joint Life Insurance: Everything You Should Know

Updated on Mar 11, 2025 • 6 min read

Joint life insurance, or dual life insurance, is a type of life insurance that insures two people on the same policy. Couples can use it to protect a surviving spouse or designate a cash inheritance, but joint life insurance is also useful for business co-owners looking to protect business assets.

Joint life insurance is a specific life insurance product that few providers offer. If you want to learn more about this type of coverage or to review your options, Final Expense Benefits has you covered. Our expert agents understand the life insurance market and are ready to help you make an informed decision on your coverage.

Call us at (866) 786-0725 to learn more about joint life insurance or for quotes, or check our free online quoting tool for personalized pricing estimates for individual life insurance.

What Is Joint Life Insurance?

Joint life insurance covers two people, but how? Dual life insurance is typically a single policy covering two people with a single monthly premium.

Dual life policies are almost always whole life, which means that as long as premiums are paid, they lasts the entire lives of the insured policyholders. Some insurance providers offer joint term life insurance and joint universal life plans, but such policies are rare.

Many people who opt for dual life insurance are married couples, but you don’t need to be married to be covered. You just need to provide some proof of shared financial responsibilities. Business partners can also use these plans, often using benefits from a joint insurance policy to cover expenses if a partner dies.

How Does Joint Life Insurance Work?

A whole life joint life insurance policy acts like most other whole life policies: premiums are set at its start, it grows in cash value over its lifetime, and coverage lasts until the policyholder’s (or policyholders’) death.

Insurance providers have different requirements, but some dual life insurance policies may require a medical exam, have a waiting period, pay a modified death benefit payout, or more. Policies will differ.

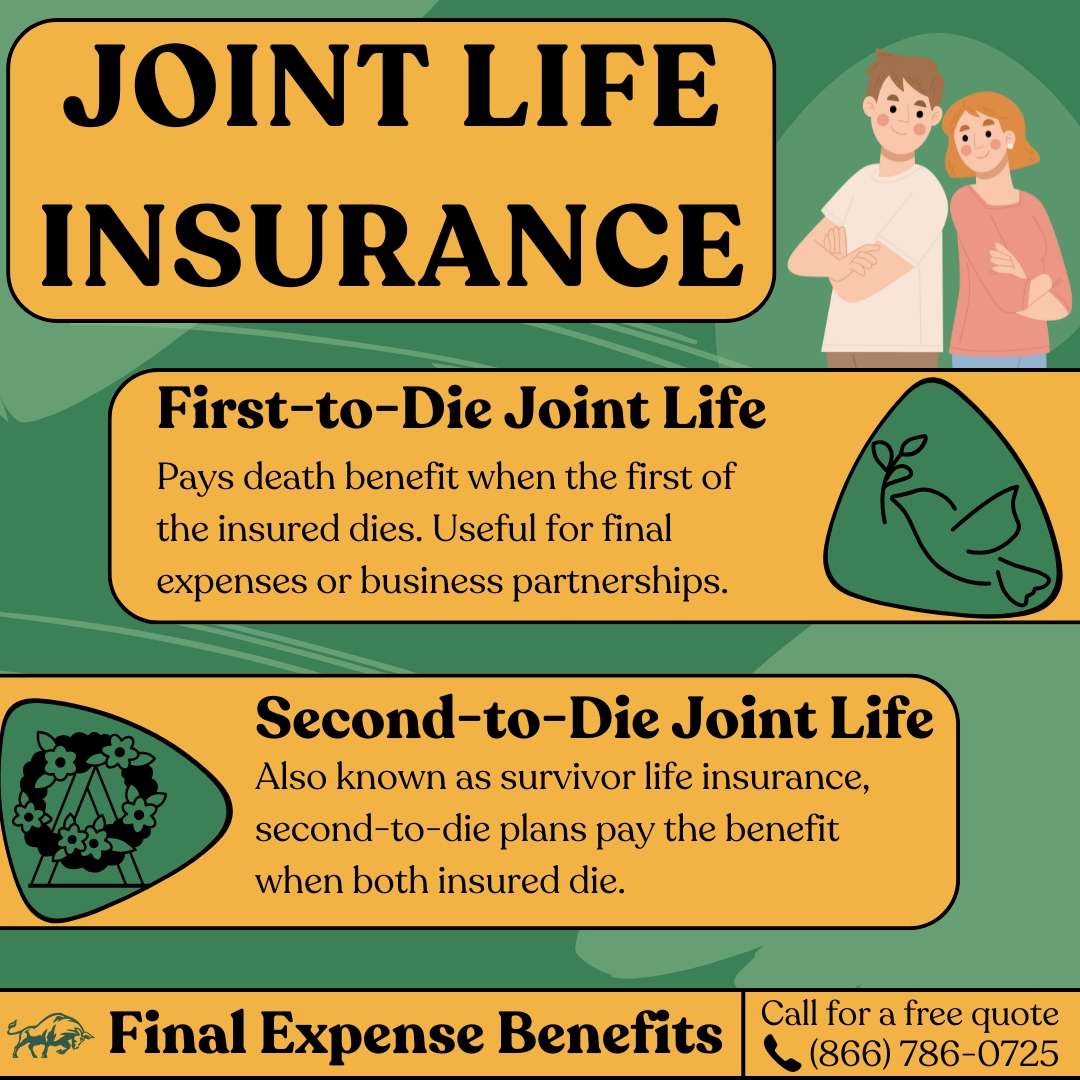

A joint policy differs from comparable life insurance plans in handling death benefit payouts. Traditional whole life policies pay upon the policyholder’s death, but a dual life insurance policy may not. Dual life insurance is typically paid in two different payout structures: first-to-die and second-to-die.

First-To-Die Joint Life Insurance

The insurer pays the death benefit after the first of the joint insured policyholders dies on first-to-die joint life insurance policies. The beneficiary is designated ahead of time and is typically the surviving partner.

Not every provider offers first-to-die joint life insurance. They may opt for you to enroll in a standard individual life insurance policy instead. In fact, individual policies are quite similar to first-to-die joint insurance because coverage ends as soon as the death benefit is paid upon the first policyholder’s death.

An older or less healthy partner could drive up dual life insurance premiums for an otherwise healthy applicant, so you should be careful with first-to-die dual life insurance. It’s more helpful for business partners to use first-to-die policies to cover business expenses upon the death of one of the partners.

Second-To-Die Joint Life Insurance

Second-to-die joint insurance, also known as survivorship life insurance, pays the death benefit when both insured policyholders die. These policies are best for established couples, typically parents, looking to support a dependent or designate money for charity after death.

Application requirements for second-to-die life insurance are more relaxed than first-to-die plans. The insurers’ risk is managed because applications consider both applicants’ health conditions and payouts only occur after the second policyholder’s death. Therefore, a second-to-die joint life insurance policy can help a less healthy partner get life insurance coverage they may otherwise have difficulty qualifying for.

There may be a gap between each insured policyholder’s deaths, making second-to-die joint insurance less helpful as an income replacer and more useful as a type of tax-free inheritance. Remember, the surviving insured is responsible for premium payments after the first insured policyholder’s death.

Joint Life Insurance vs. Individual Life Insurance

Joint life insurance and individual life insurance are quite similar but differ slightly in use cases. Individual policies, especially whole life plans, are well-suited to covering funeral costs and other end-of-life expenses. Due to the differing payout structure, dual life insurance may not be suitable for final expenses.

Joint life insurance can also get quite messy if the insureds are married and get a divorce.

Many dual life insurance plans offer insurance riders (optional extra coverage) that split death benefit payments in case of divorce. Payouts for plans without these riders could end up going to an undesired party.

For most cases, Final Expense Benefits advises using individual life insurance. A simpler plan with a more straightforward payout structure is often preferable, especially for final expenses.

If you’re interested in life insurance, call us at (866) 786-0725 to learn more.

Pros and Cons of Joint Life Insurance

Pros

Well-suited for estate planning

If you have significant assets or want to provide a tax-deferred supplementary inheritance in cash, a second-to-die joint policy could help. You could use it as a controlled way to ensure a specific heir can get an inheritance share in cash without the complication of a will or estate management.

Available for unmarried couples or business partners

Joint life insurance isn’t just for married couples. People in domestic partnerships and business partners can benefit from a dual life insurance policy.

Can be less expensive than purchasing two policies

If you want coverage for yourself and a partner, a single joint policy with one premium could be cheaper than two individual policies with separate premiums.

Cons

May cost more than two policies

Unfortunately, dual life insurance may become more expensive than two individual policies. If one partner has health issues and the other does not, premiums could drastically increase. Insurers look at joint applicants’ health as a whole. Standard final expense coverage for people in poor health can be surprisingly affordable, and you can often get plans without a waiting period even with preexisting conditions.

- Divorce complications

Some insurers don’t allow a dual life insurance policy’s benefit to be split without a rider. If you have a shared joint plan and get a divorce, you may have a tough time making sure payouts go where you want them to. With a standard final expense policy, you can typically change beneficiaries whenever you need.

Lower cash value growth

Because premiums with a single joint plan are less expensive than two separate individual policies, cash growth is significantly slower. Additionally, depending on the payout type, beneficiaries may be waiting for some time before the payout.

Harder to find

Far fewer insurance providers offer joint insurance as an option than traditional final expense policies.

Final Thoughts

Joint life insurance can be a good choice in some specific cases, but it’s better for most people to get an individual final expense policy instead. If you’re looking to manually control an inheritance payout or cover business expenses with a partner, a joint life insurance policy could be useful.

Contact our agents if you are interested in learning more about dual life insurance and to review all of your life insurance options. Final Expense Benefits works with over 20 of the top-rated life insurance providers on the market.

Call Final Expense Benefits at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m. ET, and check our free online quoting tool for a personalized estimate.

Frequently Asked Questions

What is whole life insurance?

Whole life insurance is a type of policy that lasts for the rest of the policyholder’s life, as long as they pay the premiums. Whole life insurance also has a cash value that grows over the lifetime of the policy.

What is final expense insurance?

Final expense insurance is a type of whole life insurance often used to cover end-of-life expenses like funerals. It’s designed with older applicants who may have health issues or fixed incomes in mind.

Survivorship life insurance vs. joint life insurance: What’s the difference?

Survivorship life insurance is a type of joint policy. Also called second-to-die joint plans, survivorship life insurance policies pay upon the death of both of the joint insurance policyholders.

Is a joint life insurance policy better than individual life insurance?

It depends on your needs. If you’re trying to manage assets or cover the loss of a business partner, joint insurance could be helpful. However, traditional plans are generally more helpful for the average person’s needs.

Do you have to be married to get joint life insurance?

Absolutely not. Business partners and people in domestic partnerships can also get a joint life policy. The only additional requirement is proof that you depend on each other or have shared assets.

Does joint life insurance pay two death benefits?

Joint life insurance only pays one benefit, regardless of if it’s a first-to-die or second-to-die policy.