Your Comprehensive Guide to Final Expense Life Insurance | Everything You Need to Know

Updated on Feb 10, 2025 • 8 min read

When looking for a final expense life insurance policy, you may search for the most popular companies because they have more reviews and are trusted names in the insurance industry. These companies have been around for years and countless customers rely on them. Companies such as Gerber, AARP, and New York Life will appear at the top of the search results page.

While these popular companies have name recognition and popularity, that does not mean they are the best or most cost-effective. Final Expense Benefits is here to help you find the final expense policy that gives you the coverage you need but is also the most cost-effective. Our expert agents are available Monday – Friday, 9 A.M. – 5 P.M. E.T. Our free quoting tool is available at your convenience.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

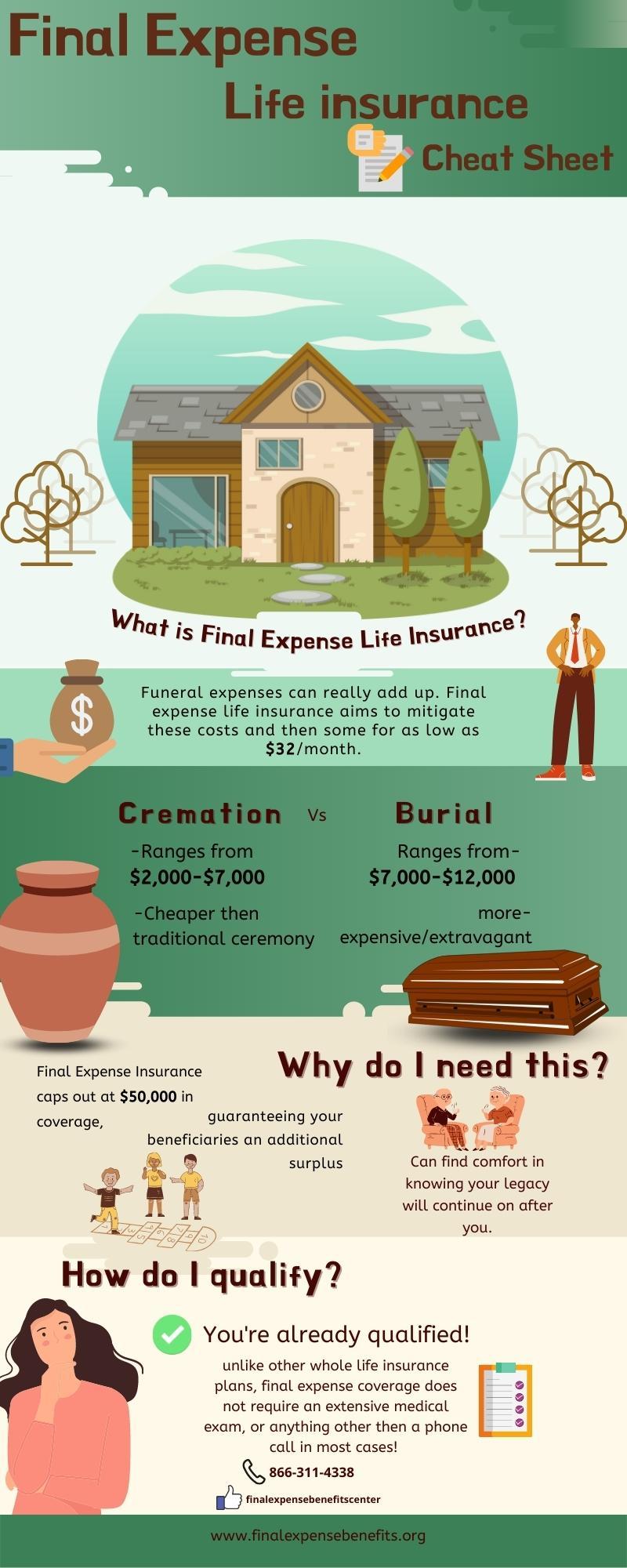

What is Final Expense Life Insurance

Final Expense life Insurance is a whole life insurance policy that can cover many things, most notably covers funeral costs or outstanding bills after your passing.

This insurance is sometimes referred to as burial or funeral insurance. You must apply for this coverage and upon approval, your family will be entitled to the payout immediately after your passing.

A final expense plan doesn’t usually require a medical exam and is easier to qualify for than other types of insurance. Additionally, this plan will give you lifetime coverage and can build cash value over time.

Why You Need Final Expense Life Insurance

There are many reasons why a final expense insurance plan can benefit you and your loved ones.

1

For Your Peace of Mind

Knowing you have a final expense insurance plan will give you and your loved ones peace of mind. Grieving a family member is difficult and the added stress of bills and planning a funeral can exacerbate the grieving process.

A final expense insurance plan will ensure that your loved ones are taken care of and will not have financial stress added to their grieving.

2

Ensure Your Wishes Are Carried Out

Although it may be hard to consider now, everyone has specific wishes regarding their funeral. There are many options to think about — such as flower arrangements, themes, and more.

By making these decisions ahead of time, you can ensure that your wishes are carried out and take additional stress off your loved ones. Without a guideline, your family might feel the burden of figuring out what you may have wanted.

3

Take Care of Your Loved Ones

Funerals have become very expensive in recent years. On average, the cost of a funeral in America ranges from $8,920 to $9,429. While shocking, this figure is only an estimate of the funeral proceedings, not the burial service or grave price. When considering every aspect of a funeral, the total cost can range anywhere from around $10,000 – $20,000. This cost can blindside family members as many are unaware of how expensive a funeral can be.

Putting aside money for your final expenses will ensure you protect your family from unexpected bills and they are financially secure. Any leftover money from your final expense costs can be used by your family to cover other costs such as bills, education costs, or any other unexpected costs your family may face.

Cremation

Cremation services can cost between $2,000 to $7,000, depending on the funeral home and the type of funeral you choose. Direct cremation is less expensive than cremation with a casket. Cremation costs are approximately $3,585 and around $6,170 for cremation services in addition to a full viewing, service, transportation, embalming, and more.

Traditional funerals are more expensive than cremation since caskets are the biggest expense when it.

The traditional cremation ceremony is the most popular option. It combines a funeral service with cremation. This allows the family to hold a conventional funeral service with a viewing of the body, the funeral service, and the following ceremony. After the viewing, the body is cremated and returned to the family in an urn or designated container. The total for this service is $6,170.

If you prefer your body to be donated to science, researchers will use the body for scientific purposes and the ashes will be returned to the family. If you choose this option you will not have to pay for the cremation.

What's the Best $10,000 Final Expense Life Insurance Plan?

Final expense life insurance comes in many coverage options, typically starting at $2,000 and capping out at $50,000. It is best to lock in a plan as soon as possible as the cost increases as you get older. Below is a chart of sample rates for seniors seeking a $10,000 burial insurance plan.

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

Pros & Cons of Well-Known Final Expense Life Insurance Companies

AARP

AARP has teamed up with New York Life to offer life insurance to seniors. AARP has been around for years and is considered a very reputable company. AARP offers:

- Term life insurance up to $100,000 in coverage

- Term life insurance with no medical exam up to $50,000 in coverage

- Guaranteed issue whole life with no medical exam up to $25,000

AARP is a well-known company, but their final expense insurance has mixed reviews. The company has high financial ratings which shows their strong ability to pay claims, but they had over 100 complaints filed last year with the Better Business Bureau (BBB).

Pros:

- Straightforward and simple application process

- No medical exam required

- Accepts pre-existing conditions

- Smokers pay the same rates as non-smokers (exclusions apply)

Cons:

- You are only able to get a policy if you are an AARP member

- Death benefit amount is low

- If you are a health senior there are more affordable options available

- Premiums are expensive

- Coverage is available only to seniors from 50-74

Gerber

One might not consider getting a final expense life insurance policy with Gerber, as the company is closely associated with insurance for babies but do offer guaranteed issue whole life insurance for seniors.

Anyone between 50 and 80 can get between $5,000 and $25,000 in guaranteed life insurance coverage from Gerber. There are no health questions or a medical exam to complete, however there is a waiting period called a graded benefit.

While Gerber is a popular company known for their baby life insurance plan, their life insurance plan for adults leaves much to be desired. Last year there were over 30 complaints filed with my customers noting a lack of customer service and an inability to change their payment method online.

Gerber could be a good option if you are a senior who needs very little coverage or are in poor health and would prefer an insurance plan with no health questions or medical exams.

Pros:

- Option with no medical exam and no health questions

- Seniors aged 50-80 cannot be refused coverage

Cons:

- Many customer complaints

- Waiting period for guaranteed life insurance

New York Life

New York Life was founded in 1845 and has become a well-established name in the insurance industry. Most insurance products from New York Life are fully underwritten, meaning you must answer a health questionnaire and complete a medical exam. However, the simplified issue term life insurance policy from New York Life does not require a medical exam, only a short health questionnaire.

With this policy, you can get up to $150,000 in coverage, but it is important to note that rates on this policy increase every five years.

The guaranteed issue whole life policy for seniors only gives you up to $15,000 in coverage. There are no medical exams, rate increases, or health questions to answer. New York Life has received over 100 complaints on the BBB within the last year. Many customers raise concerns about not being able to cancel their policy or being overcharged.

While customers have expressed frustration with New York Life, this plan is a nice option for those who don’t need much coverage or those who would prefer a term policy with no health exam.

Pros:

- Strong financial standing

- Guaranteed issue whole life option is offered

- Senior term with no health exam

Cons:

- Many customer complaints

- Coverage limits are low

- If you are a fairly healthy senior, you will be overpaying with this option

Pros & Cons of Our Trusted Final Expense Life Insurance Providers

AIG Life Insurance

AIG Life Insurance was established in 1919 and has quickly become a popular choice for life insurance. Their life insurance for seniors policy is a guaranteed issue whole life insurance policy for seniors from age 50 to 80.

AIG offers guaranteed acceptance final expense insurance, meaning you do not need to complete a medical exam or health questionnaire in order to obtain coverage. Additionally, if you pass away within the first two years, your beneficiary gets 110% of the premiums paid, rather than the full death benefit. AIG has excellent financial ratings and competitive rates, making this a great choice for seniors.

The complaint index for AIG is currently at 0.53, which is lower than The National Complaint Index of 1.00. Some complaints do state that the processing time was longer than expected and other customers had difficulty reaching an agent.

Overall, this option is a great choice for seniors who are in poor health and want to choose the guarantee issue.

Pros:

- Complaint score is lower than average

- Competitive Guarantee Issue Prices

Cons:

- Customers have reported long waiting periods

- Only for seniors from age 50 to 80

Mutual of Omaha

Mutual of Omaha was founded in 1909 and is one of the largest life insurance companies in the United States. Their insurance is highly rated by customers and the age limits are fairly generous.

Mutual of Omaha offers burial insurance without a medical exam for applicants up to age 85.

Additionally, the company offers a guaranteed issue final expense life insurance with coverage amounts ranging from $2,000 to $25,000. There are no medical exams or health questions with this type of insurance and you are guaranteed to be approved.

Mutual of Omaha burial insurance rates are based on age and the price will never increase. This policy has a graded death benefit with premiums returned plus 10% if you pass away in the first two years.

Overall, Mutual of Omaha is a great option if you are looking for a death benefit of $25,000 or less. It is also a great option if you are in poor health as there is no required medical exam or health questionnaire.

Pros:

- Competitive Rates

- Issue up to age 85

- Most claims are reported to have been paid within 24 hours

Cons:

- Graded death benefit

Aetna

Aetna has been selling life insurance policies since 1861 and was acquired by CVS Health in 2018.

Aetna is considered one of the best burial insurance companies as their underwriting is more lenient when it comes to accepting individuals with a variety of health issues. Additionally, they offer final expense life insurance to seniors over 80.

Aetna’s final expense insurance is a simplified issue whole life policy that does not require a medical exam. To qualify, you will only be required to answer some basic health questions, your coverage will last forever, premiums never increase and your policy will earn cash value. There are no restrictions on how the money can be used and your beneficiaries will receive a tax-free payout.

Aetna is a great option for seniors over 80 who are looking for final expense life insurance or seniors with pre-existing conditions.

Pros:

- Will accept seniors for immediate coverage even if they have high-risk conditions such as COPD or diabetes

- In order to qualify you will only have to answer certain health questions, there is no medical exam requirement

- Competitive pricing

Cons:

- No guaranteed acceptance

- Depending on your circumstances, you might find that other companies are less expensive

Conclusion

There are many options when it comes to finding a final expense life insurance provider and it can be confusing to figure out where to start. When looking online for final expense providers, you may immediately see some familiar names such as New York Life or AARP. While these companies are well-established, they will most likely cost much more than a lesser-known insurance company.

The reason why you may end up paying more for a more popular insurance provider is that these companies have a high marketing budget. To make money back from the marketing costs, these companies will charge you more. There are plenty of less expensive options available from lesser-known insurance companies. Not only are these companies less pricy, but their coverage is just as good, if not better. Final Expense Benefits works closely with these companies, knows exactly what they are looking for, and can help you find a policy that gives you the coverage you need at the best price.

Interested in finding a plan that provides you and your loved ones the necessary coverage? Our talented agents can help you find a plan Monday through Friday, 9 A.M. – 5 P.M. E.T at (866) 786-0725. Our free quoting tool is available at your convenience to get estimates on pricing.

Frequently Asked Questions

I Already Have Whole Life Insurance, Why Do I Need Final Expense Life Insurance?

Let’s put it this way. Funerals are expensive, and you get that. Considering final expense coverage options aren’t expensive, you would trade a minor monthly expense to ensure your beneficiaries are secure.

Are Two Life Insurance Policies Necessary?

Necessary is debatable. We’d recommend asking yourself, “could we handle funeral costs comfortably?” if the answer is no, final expense options are a great idea considering the low monthly cost.

Will My Final Expense Life Insurance Monthly Payment Be Too High?

Not at all. Final expense coverage generally ranges between $30 and $70 a month, on average. Factors that can affect this price include height, weight, age, preexisting conditions, etc.

How To Pick A Funeral Home For Cremation?

The two most apparent concerns are the cost and services offered. It’s important to conclude what you’re looking for before anything else.