Everything You Need to Know Before Buying Burial Insurance for Your Parents

Updated on Jan 20, 2025 • 6 min read

Losing a parent is one of the hardest things to go through. Purchasing a burial insurance policy will provide comfort during the difficult transition period. Burial insurance is a type of life insurance for your parents and is important to consider as you begin to make final arrangements. It can not only help pay for funeral expenses but also help cover everyday costs to give you and your family peace of mind.

Discussing burial insurance or even thinking about the loss of a loved one can spark anxiety and unease in anyone. No one wants to think about life after the passing of a parent and bringing up the topic can be awkward. While it is extremely difficult, it is also very important to discuss while your parents are still around to ensure that their wishes are enacted and that your family is taken care of. Final Expense Benefits is here to cover all of your questions regarding burial insurance so that you can make the best choice in coverage for your loved one.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

Can You Get Burial Insurance for Your Parents?

Why You Should Get Your Parents’ Burial Insurance

What Happens If Your Parents Pass Away Without Life Insurance

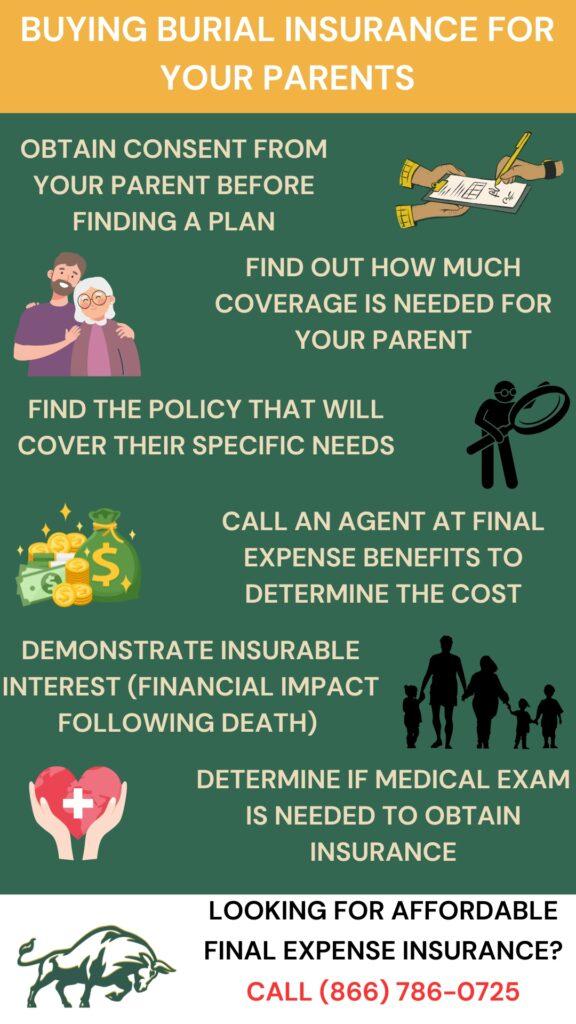

How to Obtain a Burial Insurance Policy for a Parent

Determine your parent’s specific needs: Figure out how much coverage you will need based on a combination of funeral costs, your parent’s financial commitments, and if you are a dependent, any supplemental income you may need.

Demonstrate insurable interest: In order to purchase a burial insurance policy for your parents, you must have insurable interest. Insurable interest is a financial interest in a person that would result in loss or difficulties once they are gone. The following are the most common financial obligations that would satisfy the insurable interest requirement:

- Funeral Bills

- Expenses associated with providing for a surviving parent

- Any debt that you have taken responsibility for following the loss of a parent

- Additional expenses that would fall to you after the passing of a parent

Life Insurance Options for Elderly Parents

Some variables will impact the type of coverage you can obtain for an elderly parent. The cost of burial insurance will vary depending on the health, age, gender, state of residence, and tobacco usage of an individual.

Some insurers may require a medical exam to qualify, but not all. It can be difficult to find a plan that will not only fully cover your parents, but also covers any health issues your parents may have.

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

No Exam Burial Insurance

Someone with a pre-existing condition may opt for a no-exam burial insurance policy. The downside of this type of insurance is that it is typically more expensive than standard life insurance, but your beneficiary can claim the death benefit whenever they choose, so long as you have paid the premiums.

Guaranteed Acceptance Burial Insurance

If you do not want to answer a health questionnaire, you can opt for a guaranteed acceptance burial insurance program With this type of plan, you will be accepted with no medical exam or questionnaire regardless of status.

The disadvantage of this type of plan is that you will not receive immediate coverage. It can take about two years for beneficiaries to receive the amount on your policy. Additionally, with this type of policy, your premium will be high for the coverage you receive.

Conclusion

Starting a conversation with your parents about burial insurance can be awkward and hard to even think about, but it will provide a financial safety net for your family and will also make the transition process easier.

Finding the plan that best suits your family can be difficult, but Final Expense Benefits is here to help make this decision easier. If you are looking for affordable and trusted burial insurance, call one of our talented agents today at (866) 786-0725 to get a quote and discuss options.

FAQ

Is Burial Insurance Worth It?

It is important to make sure parents, especially elderly parents, have burial insurance to help surviving family members cover funeral costs, leftover debt, and everyday costs.

Can I Buy Burial Insurance For My Parents?

Yes, you can get burial insurance for your parents, but you need their consent. They must also meet any requirements regarding health and age.

What Is The Difference Between Burial Insurance And Life Insurance?

Burial insurance is a life insurance policy that pays a flat sum to a chosen beneficiary. Unlike standard life insurance, burial insurance does not require a medical exam to determine the cost of the policy.