The Future of Life Insurance: New Trends That Could Change Everything

Updated on June 3, 2025 • 7 min read

The future of life insurance isn’t just about new tech or changing policies. It’s about how coverage is evolving to meet your needs in a digital-first, post-COVID-19 world. From artificial intelligence technology to instant approvals, the industry is transforming fast. Here’s what you need to know to stay ahead of the curve.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

Life Insurance Is Changing

Before we look ahead, it’s important to understand how the life insurance landscape is shifting.

The life insurance industry is facing a wave of transformation, driven by digital disruption, shifting generational values, and COVID-19. As we emerge from the pandemic, consumers are rethinking financial security. Planning for the future has turned into preparing for today.

How The Life Insurance Industry Is Evolving After COVID-19

According to the Life Insurance Marketing and Research Association, or LIMRA, post-COVID life insurance trends show consumers like you want easy access to simplified, quality policies. This shift is fueling the future of the life insurance industry, where digital access, speed, and personalization are no longer optional: they’re expected.

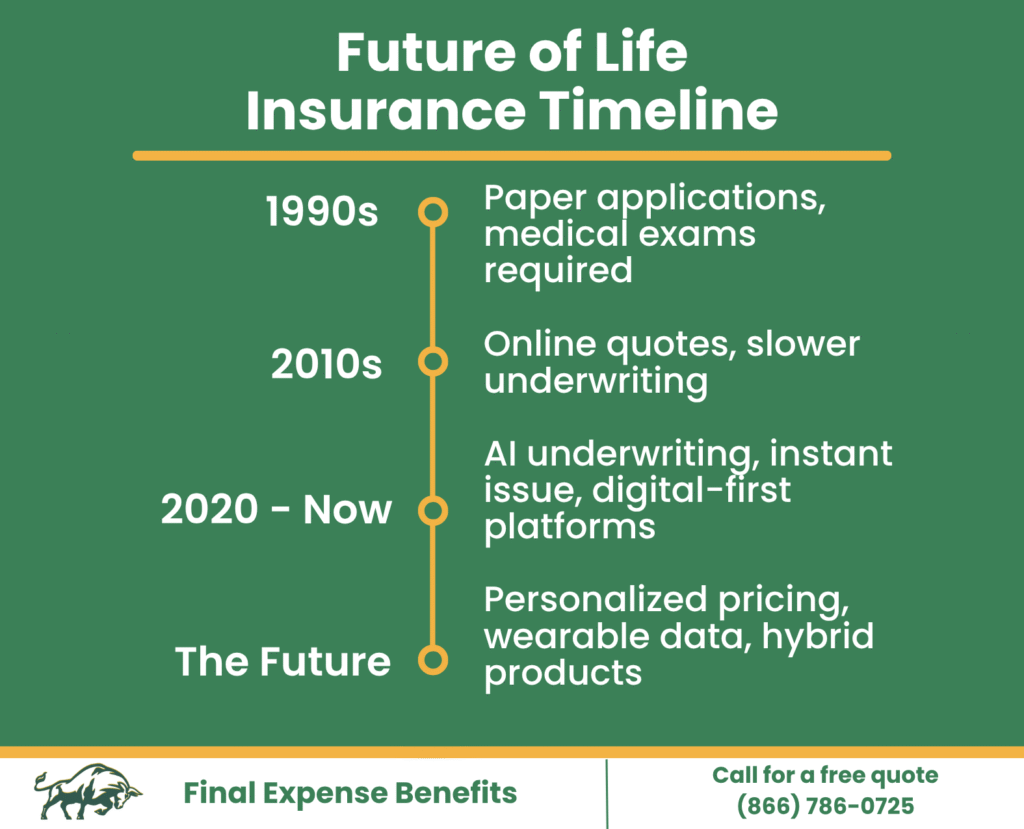

Remember when applying for life insurance meant piles of paperwork, weeks of waiting, and medical exams? Now you can apply, get a quote, and get approved, all from your phone with Final Expense Benefits.

Final Expense Benefits has the most accurate information and rates. Check our free funeral cost calculator to find estimated prices. Call Final Expense Benefits at (866) 786-0725 to connect with an agent and get quoted in less than 20 minutes.

Technology is Reshaping the Life Insurance Application Process

Insurers are turning to technology to keep up with changing consumer habits. From artificial intelligence to mobile apps, the way you apply for coverage is getting a modern makeover.

AI-Powered Underwriting and Digital-First Platforms

One of the most significant shifts in life insurance today is how companies evaluate risk and interact with customers. Technology is leading the way in modernizing the life insurance industry.

Thanks to advancements in AI-powered underwriting, applying for coverage is faster and more accurate than ever. Insurers now use automated systems that pull from the Medical Information Bureau’s records, credit data, and behavioral insights, often through secure health data platforms like Human API, to streamline approvals. Insurers can instantly access information that once took weeks to acquire, all while offering customers more personalized pricing.

Instant-Issue Policies Are on the Rise

Today’s market is rapidly growing in instant, simplified-issue life insurance policies. Simplified-issue plans offer same-day coverage with minimal paperwork, tapping into the booming young adult life insurance market.

Call us at (866) 786-0725 or use our free quoting tool to compare policies and find the best option for you and your needs.

Consumer Expectations Are Redefining Coverage

Today’s market is rapidly growing in instant, simplified-issue life insurance policies. Simplified-issue plans offer same-day coverage with minimal paperwork, tapping into the booming young adult life insurance market.

Is Self-Service the Future of Life Insurance?

Today’s consumers, especially millennials, want control and convenience without giving up quality.

Millennial insurance buyers expect a streamlined, digital-first experience. As more companies deliver on that promise, the digital experience in life insurance becomes critical for customer satisfaction and long-term retention.

Final expense insurance stands out for its straightforward design, making it an ideal choice for seniors seeking peace of mind without paperwork overload. With no medical exam required and fixed premiums for life, this policy removes the confusion and delays often associated with traditional life insurance.

Life Insurance is Getting Easier and More Flexible

Life insurance is changing to make things simpler and more helpful for families. Some new plans, called hybrid policies, give you more than one kind of protection in one package. They might help pay for care if you get sick, save money for the future, or even give you a steady income when you’re older.

Some people also want their funeral plans to be environmentally friendly. That’s why some insurance policies now cover things like tree pod burials, green burials, or water cremation. These choices are gentle on the planet and still give your family peace of mind.

Behavior-Based Pricing and Personalization

More and more, policies are tailored to you, not just your age or health, but your habits.

Tech-enabled tools like wearables and mobile tracking are driving data-driven life insurance models. With wearables in life insurance, providers can offer personalized pricing through predictive analytics based on your activity and lifestyle habits. It’s a win-win for health-conscious consumers who want lower rates and real-time feedback.

Get a clear breakdown of funeral expenses based on your choices with our free funeral cost calculator. Call Final Expense Benefits at (866) 786-0725 to get started.

What the Future of Life Insurance Means for You

So, what does all this mean for life insurance applicants? Let’s explore how these trends directly impact your experience.

It’s Easier Than Ever to Get Covered

Getting life insurance used to be a drawn-out process. Not anymore. The future of life insurance is all about speed, choice, and simplicity. Most final expense policies are issued without a medical exam, making them ideal for seniors or individuals with health concerns. That means, even seniors with pre-existing health conditions can qualify without answering medical questions or taking a medical exam. Once approved, coverage never decreases, and premiums remain the same for life.

The Cost of Waiting Might Increase

Life insurance trends and inflation mean many providers may raise premium rates as they adjust to data-driven risk models. And it’s not just premiums: funeral costs are rising too, adding even more pressure to plan. The longer you wait, the higher your rates could be, especially if your health changes or interest rates continue fluctuating. The best time to get a policy is now, and Final Expense Benefits can help.

Even with all the digital advances, some things haven’t changed, like the value of expert advice. Talking to a licensed insurance agent can help you understand complex terms, choose the right policy, and avoid costly mistakes. Need help? Our licensed professionals are just a click away.

Call us at (866) 786-0725 or use our free quoting tool to compare policies and find the best option for you and your needs.

How Much Does Final Expense Insurance Cost?

Below are sample rates from our top final expense insurance providers. These sample rates are based on a benchmark $10,000 policy using a non-smoking applicant with no pre-existing health issues.

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

These rates are estimates only, calculated for $10,000 level-benefit burial insurance with a non-smoking applicant.

Final Thoughts

The future of life insurance isn’t just changing for the industry, it’s changing for you. Whether you’re just starting your career or planning for retirement, the smartest move you can make is to stay informed and take action before rates rise or your health changes.

For many older adults, the ease of applying and knowing your loved ones won’t face complicated claims or out-of-pocket expenses is one of the greatest gifts you can leave behind.

Curious about what the future of life insurance could mean for your policy? Call now from Monday through Friday, 9 a.m. to 5 p.m. ET at (866) 786-0725.

If you’re interested in these or any of our other final expense insurance options, call Final Expense Benefits at (866) 786-0725.

FAQ

What is the future of life insurance?

The future of life insurance is centered around speed, personalization, and convenience. Expect more policies that use AI-powered underwriting, issue instantly, and allow customers to apply and manage coverage entirely online.

Will I still need a medical exam to get life insurance?

Many insurers now offer no-medical-exam life insurance, especially for younger or healthier applicants. These policies rely on digital health data and predictive tools to make fast, accurate decisions, sometimes in just a few minutes.

Are funeral costs going up in the future?

Like most living expenses, funeral costs continue to rise due to inflation, labor, and service-related fees. That’s why many families are turning to final expense insurance as an affordable way to lock in funds for burial or cremation.

What are hybrid life insurance products?

Hybrid life insurance combines traditional coverage with added features, like long-term care benefits or annuity riders. These policies are designed to provide living value, not just a payout after death, making them appealing for retirement planning and financial flexibility.

What is Final Expense Life Insurance

Final expense insurance is a small, simple policy that covers funeral costs and other end-of-life expenses. It’s usually easy to qualify for, with no medical exam, and offers lifelong coverage with a fixed premium.

Is it still worth talking to an insurance agent?

Absolutely. Even with all the digital tools, a licensed insurance agent can help you compare policies, understand the small print, and choose the best coverage for your goals. You get personalized guidance and peace of mind.

What is term life insurance?

Term life insurance covers you for a set period, like 10, 20, or 30 years. It’s usually the most affordable option for younger individuals for things like mortgage protection or family security during key life stages.