How the Medical Information Bureau Impacts Life Insurance for Seniors

Updated on June 4, 2025 • 7 min read

Seniors often face challenges when applying for life insurance, especially with pre-existing medical conditions. If you’re searching for life insurance, it’s important to understand health requirements set by insurance underwriting and how they are affected by health reporting from the Medical Information Bureau.

When you’re applying for life insurance, especially later in life, it’s important to understand how your medical history is used behind the scenes. Even if you don’t have any major health issues, your medical history and personal health can affect policy eligibility and rates.

At Final Expense Benefits, our mission is to help seniors understand how life insurance eligibility works and to find a policy that meets their needs. We partner with over 20 top-rated providers and offer compassionate guidance every step of the way.

Call us at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m. ET. Check our free online quoting tool for a personalized life insurance pricing estimate.

What is the Medical Information Bureau (MIB)?

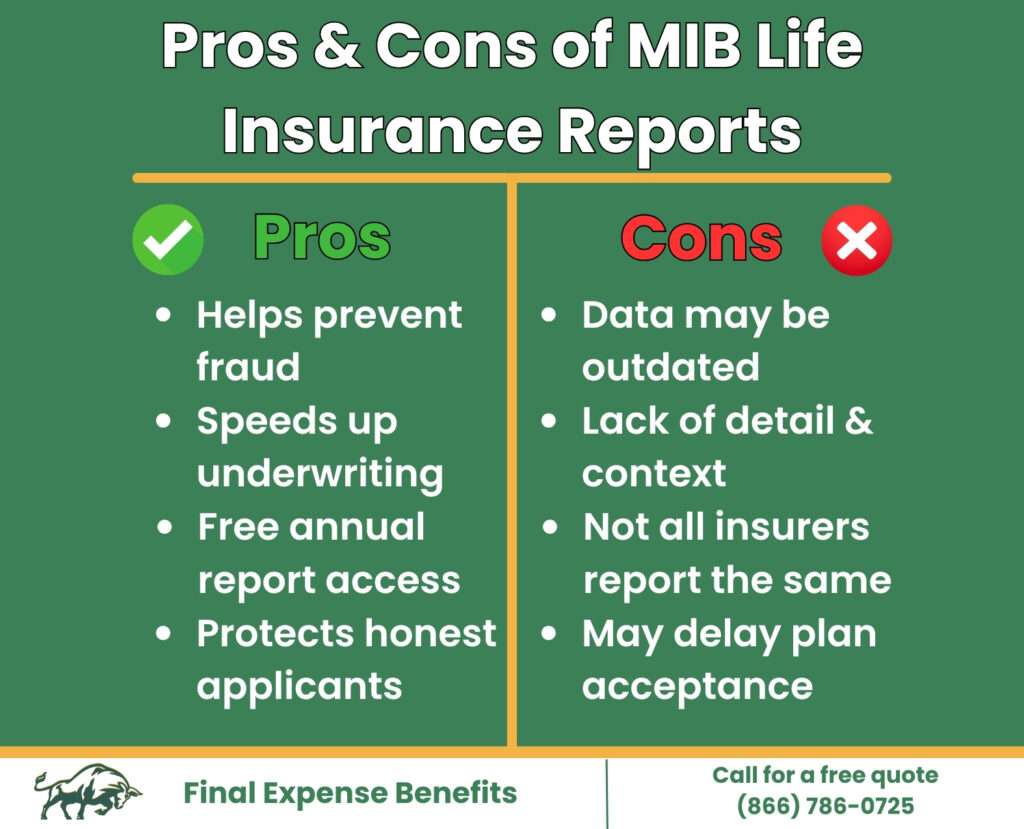

The Medical Information Bureau (MIB) is a nonprofit organization founded in 1902 that supports life and health insurance companies by enabling them to share coded information about applicants. This process helps detect fraud and verify application details. According to the FTC, over 99% of life insurance policies are issued by insurers who are MIB members.

Some key features to remember about the MIB include:

- Independent entity: It’s not a government agency or credit bureau

- Used during underwriting: Confirms applicant health to ensure policy and rate assignment is done accurately

- Supports risk assessment: Protects insurers and consumers from fraud

Rather than storing full medical histories, the MIB collects coded summaries of major health conditions, prescription history, and previous insurance applications. Medical Information Bureau reports don’t include lab results, doctor notes, or financial data.

The MIB reporting system allows insurance companies to detect inconsistencies. For instance, if a 70-year-old applicant reports excellent health but disclosed a serious illness at 66 to another insurer, the MIB helps flag the discrepancy. Inaccurate health disclosures don’t automatically disqualify applicants, but they may prompt additional verification.

Additionally, the Medical Information Bureau plays a role in maintaining affordability across the industry. Reducing fraud and minimizing risk helps insurers avoid unnecessary payouts that would otherwise lead to higher premiums for all applicants. In this way, it protects both insurance companies and honest consumers.

The Medical Information Bureau and Life Insurance Applications

Though the MIB doesn’t approve or deny coverage directly, its data can influence how underwriters evaluate senior applicants’ risk profiles. Flagged records may:

- Trigger questions or requests for medical records

- Delay applications

- Affect the premiums

MIB data doesn’t always negatively affect applicants. For some, having consistent MIB data can reassure underwriters that your application is trustworthy. It’s only when discrepancies arise that deeper research begins.

Many applicants are still approved, especially if they’re honest and work with an experienced brokerage like Final Expense Benefits. We believe transparency is a key aspect of the life insurance process for insurers and consumers. Creating a trusting relationship between insurance providers and policyholders helps seniors proactively address concerns before applying.

Our expert agents can help you navigate underwriting and find a great policy that fits your needs and budget. Call Final Expense Benefits today at (866) 786-0725 to learn more.

Medical Information Bureau Pros and Cons for Life Insurance Applicants

The key is understanding how to use the MIB to your advantage. If your MIB record is clean and accurate, it can speed up your approval process.

Learn more about our life insurance options by talking to an expert at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

Accessing and Correcting Your MIB Report

You can request a free copy of your MIB Consumer File once every 12 months to make sure it’s accurate. This is a vital step, especially if you’re applying for a new policy. Reviewing your file gives you insight into how insurers might view your risk profile.

Requesting Your Report:

- Visit www.mib.com

- Select “Request Your MIB Consumer File”

- Provide personal details (name, SSN, date of birth)

- Submit online or via mail

Reports typically arrive within 15 days of your request. Remember that y may not have an MIB record if you haven’t applied for life or health insurance in the last 7 years.

If You Spot an Error:

- Initiate a dispute through MIB

- Provide documentation (e.g., doctor letters or insurance correspondence)

- MIB will investigate and respond, typically within 30 days

Correcting inaccuracies can prevent coverage delays or denials. It’s important to act quickly so any needed corrections are made before submitting a new application.

Final Expense Insurance for Seniors and the Medical Information Bureau: What to Expect

Many seniors, especially those seeking final expense or guaranteed issue policies, may not need to worry much about the MIB. Many final expense insurance policies are simplified-issue, meaning they have relaxed health requirements and applications may not be dependent on MIB report data. Benefits of simplified-issue final expense policies include:

- No medical exam required

- No MIB report needed in many cases

- Quick approval based on simple health questions

This is why we often recommend final expense insurance to seniors with complex health histories. These plans are built for people who may have been declined elsewhere due to medical concerns, and many offer immediate coverage with no waiting period.

Also known as burial insurance, final expense insurance is whole life, meaning it covers for life, premiums are set at policy start, coverage will never decrease, and benefit payouts can grow in cash value over time. Final expense policies often have coverage limits smaller than other types of life insurance (typically $5,000 to $50,000), but they’re ideal for covering funeral costs and other end-of-life expenses. It’s an easy way for seniors to get quality, simple life insurance at low rates that covers their needs.

Guaranteed policies always disregard health questions, but rates are often 25% to 40% higher than comparable simplified-issue polices. Guaranteed policies always have a waiting period, which means the full benefit may not be available in the first few years of coverage or pay a modified benefit payout, but they still offer peace of mind for those who may not qualify for traditional life insurance.

If you’d like to check how much coverage you need for your end-of-life expenses, check our free funeral cost calculator, or check our online quoting tool for rate estimates.

Tips for Senior Life Insurance Applicants Concerned About MIB Reports

If you’re worried about how your Medical Information Bureau report might affect your life insurance application, these steps can help:

- Be accurate and honest: Application inaccuracy can lead to rejections or rate hikes.

- Review your MIB file: Know what insurers might see and fix errors in advance.

- Work with a licensed broker: They understand how MIB data factors into different policies and can match you with an insurer that fits your health profile.

- Choose simplified-issue options: Many simplified-issue final expense policies MIB checks entirely, and many focus on basic eligibility rather than deep medical history.

It’s also smart to keep your records in order. Maintain a simple summary of major medical events, diagnoses, and treatments, as well as dates and doctors involved. This helps you stay consistent when filling out applications and provides written proof of potential report errors.

Contact Final Expense Benefits for assistance finding a great burial insurance policy that works with your health needs.

How Much Does Final Expense Life Insurance For Seniors Cost?

One of the biggest reasons why we recommend seniors get final expense insurance is the low cost. Rates for seniors in good health range from about $30 to $150 per month and vary by gender and age.

Below are sample rates for a benchmark $10,000 final expense policy from some of our top-rated carriers. These rates are calculated using a non-smoking applicant with no pre-existing conditions.

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more and check our free online quoting tool for personalized pricing estimates.

Final Thoughts

The Medical Information Bureau might sound intimidating, but it’s simply a tool to help insurers validate the information you provide. By being proactive—checking your MIB report, correcting errors, and selecting the right type of policy—you can improve your chances of approval and find affordable life insurance even with medical concerns.

You don’t have to navigate this alone. A trusted brokerage like Final Expense Benefits can help you understand how your personal health and MIB report data might influence your options. And if you’re a senior who’s been turned down before, know that there are policies that don’t even consider the MIB.

Explore your options today and compare final expense policies designed for seniors who want peace of mind and financial protection for their loved ones. If you’re interested in life insurance but are concerned about your medical history, contact Final Expense Benefits. Our expert agents can help you find a great policy that fits your needs.

Call us at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m. ET, or check our free online quoting tool for more information.

FAQ

What is the Medical Information Bureau?

The Medical Information Bureau (MIB) is a nonprofit group that stores coded medical and application summaries to help insurers verify disclosed applicant medical information.

Does the MIB have my full medical history?

The MIB doesn’t store anyone’s full medical history. It contains coded indicators, not full reports or doctor records. It doesn’t include lab tests, genetic data, or full treatment plans.

How do I get my MIB report?

To get a copy of your Medical Information Bureau report, visit www.mib.com and request one free report per year. You’ll need to verify your identity and can expect the report by mail in about two weeks.

Can MIB data impact my insurance rates?

MIB report data can influence underwriting decisions, but many other factors are considered, like age, policy type, and lifestyle habits. Honesty and transparency are your best tools.

Do all policies use Medical Information Bureau reports?

Final expense and guaranteed issue policies often skip the MIB entirely, making them ideal for seniors with health concerns.

How often should I check my MIB file?

It’s ideal to check your MIB report annually, especially if you plan to apply for new life insurance coverage or have had recent medical changes.

Can I apply again if I was denied due to MIB data?

You can reapply after denial due to MIB reports or medical history. After resolving any errors or choosing a policy that doesn’t rely on the MIB, many seniors find success with their next application.