What Does Life Insurance Cover? What The Right Policy Can Do For Your Family

Updated on Jan 23, 2025 • 6 min read

What does life insurance cover? Nearly anything related to your family’s future expenses. Whether you are elderly and looking for a good plan to cover your final expenses or a young adult planning out your future, the right life insurance policy can be crucial to your family’s financial preparedness. Final Expense Benefits is here to help you understand what life insurance covers and how you can fit a plan into your family’s financial future.

The amount of options in the life insurance market can be overwhelming. That’s why Final Expense Benefits is here to help. As a trusted life insurance brokerage, Final Expense Benefits can help you find a reliable policy that covers your needs from a reputable provider.

Call us at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET, and we can help you decide if life insurance is right for you. Check out our free online quoting tool for personalized pricing estimates.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

What Is The Main Purpose Of Life Insurance?

At its most basic function, life insurance provides for loved ones’ financial futures after the policyholder passes away. Commonly, life insurance is used to cover major end-of-life expenses like funerals or as a replacement for lost income.

Life Insurance Definitions

Life insurance provides a death benefit, which is the money paid to the policy’s beneficiary upon the insured person’s death. Beneficiaries are the payout recipients designated by the policyholder. The death benefit’s value is agreed upon by the provider and policyholder at the policy’s start and is usually paid as one large lump sum.

Plans with higher death benefits will typically cost more per month. The monthly payment is called the premium.

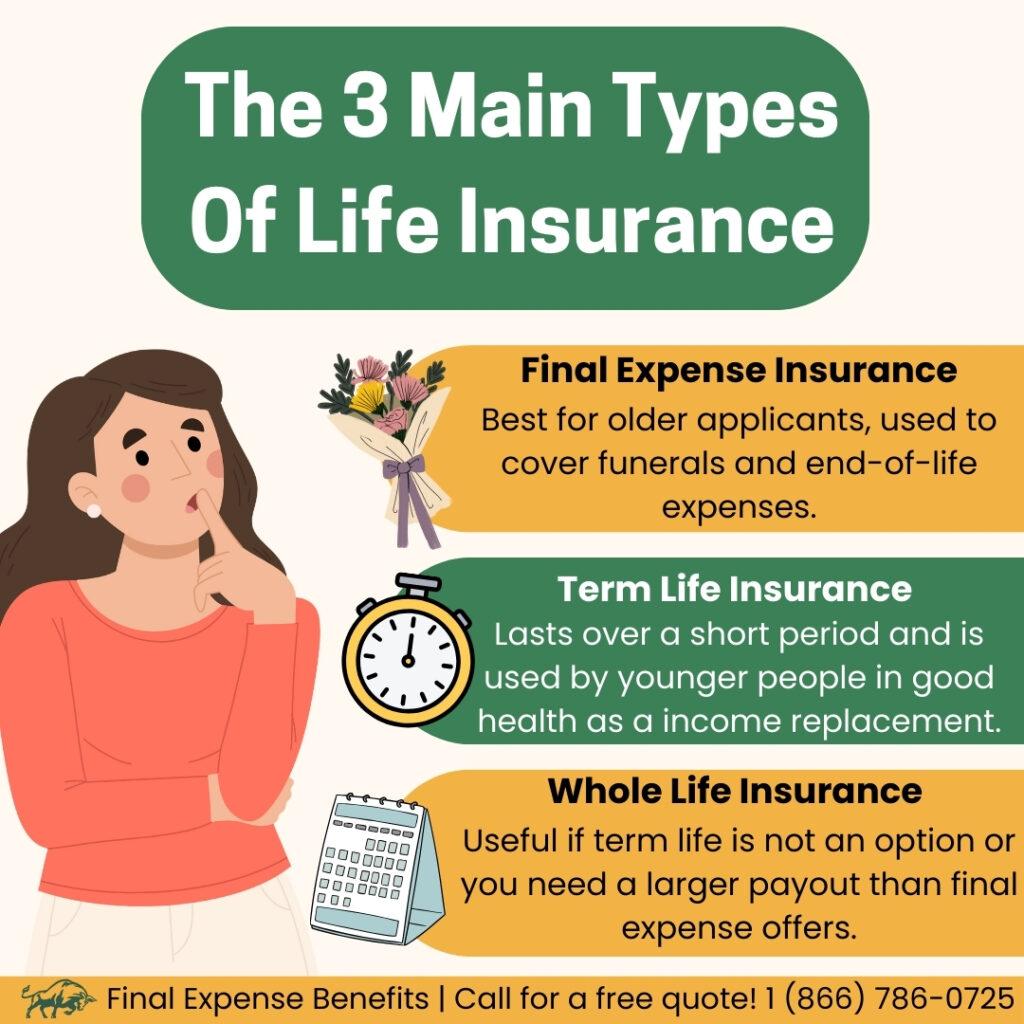

Life insurance comes in three major forms: final expense insurance (also known as burial insurance), term life insurance, and whole life insurance. Each type’s purpose and intended market are different.

What Does Life Insurance Cover?

All life insurance will pay in the case of death by natural causes. This is the typical use case for any type of life insurance. And nearly every life insurance policy will pay the benefit if the insured dies in an accident.

While examples of what life insurance payouts can cover are listed below, beneficiaries can use payouts for any purpose. Payouts are typically intended to cover costs for a funeral or other end-of-life expenses, but the recipient can use the cash from the lump sum for any desired purpose.

The right life insurance policy can be a versatile tool in providing financial security for your family. Learn more about each type of life insurance and what they can be used to cover below.

Final Expense Insurance

Also known as burial insurance, final expense insurance is a type of whole life insurance intended to cover end-of-life expenses like funerals and major medical bills.

Every life insurance plan has health requirements for applicants. These are intended to understand the type of risk a client brings to the life insurance provider to judge eligibility and set premium rates. Final expense insurance has older applicants in mind, so health requirements are much more lenient than other plan types.

Final expense insurance is often available to those with fairly major health conditions; plans that guarantee acceptance are an option if you are in poor health. All plans with guaranteed acceptance have a two-year waiting period.

This means that if you die within two years of the policy’s start, your beneficiaries won’t receive the full death benefit until that period ends. Thankfully, many plans without a waiting period will accept applicants that have serious health conditions.

As a whole life plan, final expense insurance builds cash value over time. A percentage of your monthly premium is set aside in a cash account, and that cash can be borrowed at any time. These additional funds can be used by the policyholder to pay for expenses during their lifetime or can be applied to the death benefit as extra cash for beneficiaries.

What Does Burial Insurance Cover?

Final expense insurance can cover end-of-life expenses by providing a smaller, focused death benefit payout. Possible uses for the death benefit include:

1

Funeral Services

Funerals can be pricey. According to the National Funeral Directors Association, a full traditional funeral with a viewing can cost nearly $10,000. That’s why final expense insurance is typically quoted at a $10,000 death benefit.

2

Caskets Or Urns

Funeral homes do not include the cost of a casket or urn in their funeral fees. A well-made casket can cost over $2,500 and urns over $300.

3

Burial Plots

Cemetery costs are also not included in the above funeral estimate. A vault, often required by cemeteries for casket burials, and a cemetery plot can easily cost over $3,000.

4

Medical Bills

Some medical care bills can extend to family after death. A lump-sum payment can take a dent out of major healthcare expenses. However, there’s no guarantee a final expense insurance payout will cover an entire major medical bill.

5

Anything!

While the examples listed above are common uses for a final expense insurance payout, the benefit can be used for any purpose.

How Much Does Final Expense Insurance Cost?

Because final expense insurance typically provides a smaller death benefit, rates are low, especially compared to other whole life insurance options. A major advantage to final expense insurance is that you’ll pay the agreed monthly premium rate throughout the policy’s life, like most whole life insurance.

Here are the expected monthly premiums for Final Expense Insurance for a healthy, non-smoking individual from our top providers:

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

Term Life Insurance

Term life insurance is typically bought by younger applicants to cover loss of income in case of death. These policies usually have restrictive applicant health requirements, often requiring applicants to be below age 60 and have no major pre-existing health conditions.

They’re called term life policies because they only cover a portion of the policyholder’s lifetime, usually between 10 and 30 years. Experts recommend purchasing a death benefit equal to 10 times your yearly income if you intend for your term policy to be an income replacement.

What Does Term Life Insurance Cover?

Expenses term life insurance is typically used to cover include:

1

Income Replacement

A large lump-sum payment can go a long way in ensuring financial security for your family if your income is lost due to your death.

2

Home Mortgages

Per the U.S. Census Bureau, the median monthly mortgage cost in the United States is $1904. A large lump sum can cover that for some time.

3

Regular Home Expenses

Term life plans are normally intended to replace an income stream and cover all home expenses for an extended period, giving your family financial stability in an uncertain time.

What Does Whole Life Insurance Cover?

Other forms of whole life insurance can have a higher payout than final expense insurance, but will also require a higher monthly premium payment. Because term life can be so restrictive in applicant acceptance, whole life plans may be attractive to those with underlying health concerns.

Whole life insurance can also be a limited investment because policies grow in cash value. Generally, if you’re interested in whole life insurance, you should look at policies with smaller payouts like final expense insurance. Premium rates for whole life policies with larger payouts can be prohibitively expensive; this is why we at Final Expense Benefits often recommend final expense insurance to those looking for a whole life plan.

What Does Life Insurance Not Cover?

Life Insurance can cover your family in the event of many financial hardships but do remember there are some cases where life insurance may not be able to help. These cases include:

1

Expired Policies

A term life policy will eventually expire and you won’t get a payout. This is why we recommend diversifying your life insurance holdings and having a low-cost final expense insurance policy.

2

Life Insurance Fraud

Lying on a life insurance application or medical questionnaire to get better rates is a bad idea. It can lead to the policy being voided or premium rates skyrocketing.

What Does Life Insurance Sometimes Cover?

Some specific circumstances or life insurance policy riders can determine eligibility in a few gray areas of life insurance coverage. Insurance riders are optional add-ons to insurance policies that provide extra situational coverage, usually at an additional cost.

Some policies or riders can provide coverage in the following events and more:

1

Death By Risky Activity

If you have a dangerous hobby, such as auto racing, rock climbing, or flying a plane, it’s best to disclose such hobbies with your insurance provider. Such behavior will likely raise your rates, but disclosing hobbies like these could prevent your policy’s death benefit from being voided if you die doing them.

2

Lapsed Policies

If you miss paying your monthly premium, your policy will lapse in coverage and beneficiaries may not be paid your full death benefit. Some providers and riders have lapsed coverage forgiveness. If your policy fully lapses, your paid premiums will likely be refunded.

3

Criminal Activity

Logically, if you die while performing criminal actions, your beneficiaries likely won’t be paid your death benefit. Some providers will return paid premiums to the beneficiary, and others have riders that will allow for a full payout, regardless of the nature of the policyholder’s death.

4

Death By Suicide

Some insurance providers will not pay a benefit payout if the policyholder dies by suicide. Some policies have riders that allow for full payout in case of suicide, and others will pay after the end of the policy’s two-year waiting period.

5

Expenses While The

Policyholder Is Alive

Some policies and riders allow the policyholder to access portions of the death benefit payout to pay for medical expenses and other care-related costs. Riders like this can apply if the policyholder becomes disabled.

Conclusion

Life insurance is an excellent way to provide financial security for your family when you pass away. In particular, final expense insurance is a low-cost way to cover major end-of-life expenses and ensure your family isn’t saddled with huge upfront bills at an emotionally draining time.

Final Expense Benefits is here to help you understand the life insurance market and see how a policy can fit into your financial toolkit. Call us at (866) 786-0725, Monday through Friday, 9 a.m. to 5 p.m. ET, to learn more about life insurance, and be sure to use our free online quoting tool for pricing estimates.

Frequently Asked Questions

What Does Life Insurance Cover?

Life insurance is typically used to cover end-of-life expenses like funerals and major medical bills or as a replacement for the income of a worker who died.

What Is Final Expense Insurance?

Also known as burial insurance, final expense insurance is a simplified-issue life insurance policy, meaning it has relaxed application requirements. Application requirements are relaxed so older applicants can qualify and use their final expense insurance to cover their funeral and other end-of-life expenses.

What Is Term Life Insurance For?

Term life insurance is typically used by workers wishing to provide an income replacement in case they die. Terms vary from 10 to 30 years and experts usually recommend policyholders have a death benefit 10 times their yearly income.

What Is A Death Benefit?

A death benefit is the money paid out by the life insurance policy to the beneficiaries when the insured person dies. Usually, a death benefit is paid as a single lump sum, but some plans will pay it as an annuity, which are smaller amounts paid over several years.