Average Life Insurance Payouts & How Long To Expect To Wait For Them

Updated on May 21, 2025 • 7 min read

Life insurance is a great way to provide funds and peace of mind to your loved ones after you pass away. They do so in the form of a death benefit payout, which is arranged at the policy’s start and paid over time with monthly premiums. The average life insurance payout in the United States is about $203,000 for purchased policies, per Statista. However, this number is a bit misleading.

The $203,000 average life insurance payout is calculated using policies that are purchased, not just for policies that are paid out. Policies can end without a payout, lapsing due to end of term, policy surrender, or failure to pay monthly premiums, so average paid benefits are lower.

Final Expense Benefits is here to help you understand life insurance before you make a purchase. As experts in the life insurance market, our agents can help you find a policy that fits your needs.

Call us at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m. ET, to learn more or check our free online quoting tool for a no-obligation pricing estimate.

What Is The Average Life Insurance Payout?

While the overall average life insurance policy payout is about $203,000, payouts vary by policy type. Below are average payout statistics for the main types of life insurance, term life and whole life insurance:

Data courtesy the American Council of Life Insurers.

Average Whole Life Insurance Payout

Whole life insurance offers permanent coverage, as long as premiums are paid. Premiums are locked at the policy’s start, benefits can grow in cash value, and coverage will never decrease, so whole life policies are a trusted choice for seniors.

The average whole life insurance policy benefit is about $91,000, but payouts vary by the type of whole life insurance. Traditional whole life and universal life insurance policies have larger benefit payouts than final expense insurance, which provides benefits that typically range from around $5,000 to $50,000.

As long as premiums are paid, whole life insurance covers for life. This is the main difference between whole life and term life insurance, the other most common type of life insurance. Seniors may be attracted to the low rates of term life insurance, but it has several drawbacks:

Average Term Life Insurance Payout

Term life insurance payouts are higher than those of whole life policies, averaging around $340,000. Term life policies don’t offer permanent coverage, only providing payouts if the policyholder dies during a specified time. Terms usually range from 10 to 30 years.

Term life policies pay benefits far less frequently than whole life policies and lapse far more often. If the policyholder outlives the term, beneficiaries won’t receive a payout, and the policy would need to be renewed. Rates increase dramatically as you age; if you renew, you’ll likely be paying a significantly higher monthly rate than your previous term.

Term life health requirements set by underwriting practices are strict. Seniors with pre-existing health concerns frequently have difficulty qualifying for new term life policies.

According to some estimates, only one percent of term life insurance policies pay their benefits. For all these reasons, term life insurance can be a poor choice for seniors.

Why Do Average Life Insurance Payouts Vary Between Types of Life Insurance?

Average payouts for term life and whole life insurance vary so significantly because their uses are different.

Whole life insurance (and especially final expense insurance) is typically used by seniors to provide an inheritance or cover end-of-life expenses, such as funeral costs. The average funeral costs about $10,000, so whole life benefits are usually smaller than those of term life insurance. Most whole life benefit payouts are less than $100,000, helping to mitigate rates and health requirements.

Term life is used by young adults and other workers to cover loss of income in case of death. Term payouts are high because most insurers recommend purchasing a policy with a death benefit equal to 10 times your yearly income.

Final Expense Benefits recommends seniors avoid high-dollar policies with restrictive health requirements and unaffordable monthly rates.

How Do Life Insurance Payouts Work?

Called the death benefit, a life insurance payout is set at the policy’s start. Life insurance riders are also selected at the policy’s start and can affect benefit amounts and payout triggers.

You’ll also designate your policy’s beneficiaries, who will receive the death benefit payout. You can select as many as you want, but many policyholders designate one beneficiary, often a spouse. Beneficiaries are typically family, but you can choose anyone. Many life insurance providers allow designating charities as beneficiaries.

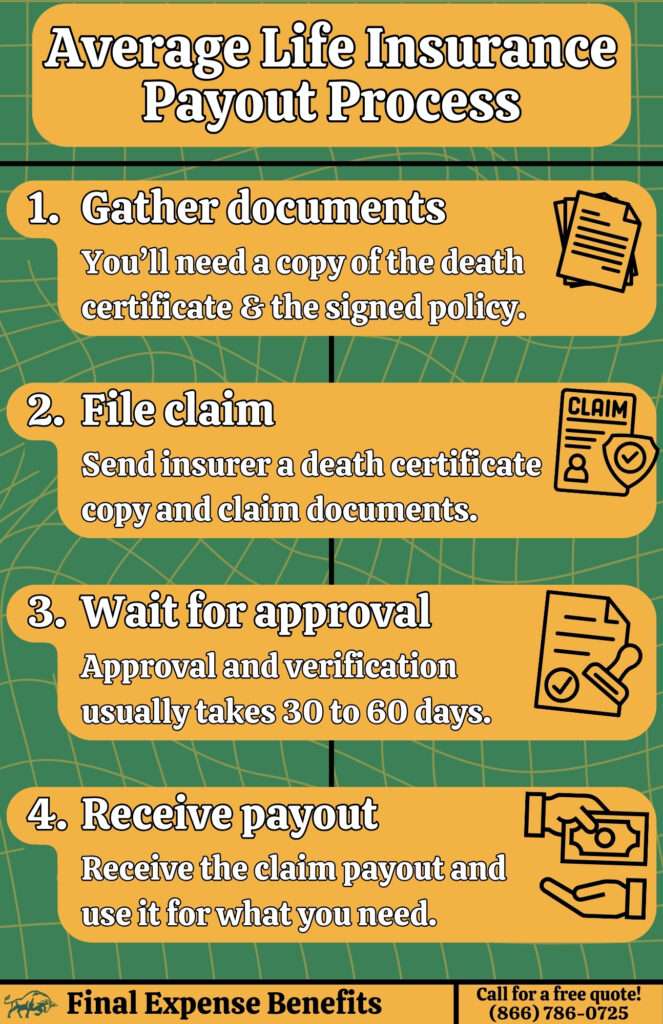

To receive the payout, beneficiaries must place a benefit claim after the policyholder dies. Additionally, they must provide a copy of the policyholder’s death certificate with their claim. After the insurer accepts the claim, beneficiaries must wait for the payout.

Once the tax-free payout is received, beneficiaries can use it for whatever they want. Typical uses include covering medical bills, funeral expenses, burial plot fees, and other end-of-life expenses.

Types of Life Insurance Payouts

Benefit payment methods are determined at the policy’s start or when the claim is placed. The main types of death benefit payouts include:

- Lump sum payment

Benefits with lump sump payments are paid in full in a single installment. This is the most common type of life insurance payout. - Installments

The death benefit is split and paid periodically on a fixed schedule until it’s fully paid.

- Income payments

The full benefit is placed into a savings account where it can accrue interest. Beneficiaries then select a periodic payment amount and schedule. If the benefit grows in total value, it may be taxed.

- Annuities

Beneficiaries can convert the payout into a deferred annuity to receive guaranteed ongoing payments.

- Retained asset

The payout is transferred to an account that accrues interest and can be accessed by the beneficiary.

How Long Does It Take Life Insurance To Pay Out?

Beneficiaries must file a claim to receive the payout. They can file claims immediately after receiving a copy of the death certificate. Beneficiaries must then confirm that the policy is active with the insurer and file the claim.

Insurers typically pay benefits about 30 to 60 days after receiving a valid claim, though some factors may make the payout take longer.

Some policies offer an optional accelerated death benefit or a terminal illness rider. If the policyholder is diagnosed with an illness with a short life expectancy (usually 12 to 24 months), they can be paid the entire death benefit instead of the beneficiaries. Accelerated death benefits are normally used to pay for medical expenses and are usually paid in about 30 days.

What Factors Affect How Long Life Insurance Payouts Take?

Life insurance providers may take longer than the normal 30 to 60 days to pay benefits. Factors that could affect payout time include:

- Payout method

Some payout methods defer payments, lengthening the payout process. - Beneficiaries

Insurance providers may take longer to process policies with several beneficiaries. - Documentation

Failure to provide proper documentation like a certified death certificate or correct claim forms can slow the claims process significantly. - Policy details

Some policies have waiting periods that delay or reduce payouts if the policyholder dies during them. Life insurance riders like accelerated death benefit riders can also affect when benefits are paid. - Cause of death

Insurers suspicious about the policyholder’s cause of death can delay payouts to investigate. - State laws

Some states shorten and lengthen how long insurers can take to process and pay valid claims. - Fraud

If insurers suspect fraud, they can delay payouts to investigate.

Final Expense Insurance Is A Simple Answer for Seniors

Also known as burial insurance, final expense insurance is a great choice for seniors looking for simplified, inexpensive life insurance. These whole life plans are designed with seniors in mind, offering relaxed health requirements, cheap rates, and benefits focused on covering seniors’ needs. Thanks to simple underwriting practices, seniors with pre-existing health conditions can qualify for final expense plans with affordable rates.

These policies typically pay quickly in a lump sum, great for covering large up-front costs like funerals, medical bills, and other end-of-life expenses.

Final expense insurance is a great choice for seniors, and we work with over 20 of the market’s top-rated providers. If you’re interested in learning more, contact Final Expense Benefits.

How Much Does Final Expense Insurance Cost?

Below are sample rates from our top final expense insurance providers. These sample rates are based on a benchmark $10,000 policy using a non-smoking applicant with no pre-existing health issues.

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

These rates are estimates only, calculated for $10,000 level-benefit burial insurance with a non-smoking applicant.

If you’re interested in these or any of our other final expense insurance options, call Final Expense Benefits at (866) 786-0725.

Final Thoughts

The overall average life insurance payout is around $203,000, but varies by life insurance type. Whole life insurance is the preferred choice for seniors with an average payout of $91,000. Average term life insurance payouts are larger, but these policies pay infrequently and don’t fit seniors’ needs.

Unlike term life insurance, final expense insurance is specialized for seniors, offering simplified payouts, relaxed health requirements, and inexpensive monthly rates.

Though average final expense insurance payouts are lower, ranging from about $5,000 to $50,000, these policies are great choices for seniors looking to cover their end-of-life expenses or provide an inheritance to loved ones.

Contact Final Expense Benefits to learn more. As experts in the life insurance market, our agents can help you find the best policy for your needs. Call us at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m. ET to learn more, or check our free online quoting tool for a pricing estimate.

FAQ

What disqualifies life insurance payouts?

Fraud and other criminal activities related to the policyholder’s death are the most common ways life insurance payouts are disqualified, but thankfully, over 90% of valid policy claims are paid. Some insurers reduce or disqualify payouts if the policyholder dies within a set waiting period.

When will I receive life insurance payouts?

Life insurance benefits are agreed at the policy’s start. Benefits are usually paid to beneficiaries around 30 to 60 days after they file a valid claim.

Are life insurance payouts taxable?

Life insurance payouts are not taxable because they are purchased with after-tax funds.

Who gets the life insurance payout?

Life insurance payouts are paid to beneficiaries who are designated at the policy’s start. You can have more than one beneficiary, and they don’t have to be relatives.

What is the lowest life insurance payout?

Final expense insurance payouts are smaller than other types of life insurance. This helps seniors operating on fixed incomes get coverage at low costs. Some providers offer policies with benefits as low as $2,000, but most start around $5,000.

What is final expense insurance?

Final expense insurance is whole life insurance designed to help seniors cover end-of-life expenses like funerals and burial plot costs. It’s often a good idea to purchase a policy ahead of time if you are at genetic risk for major terminal illnesses.