Senior Life Insurance with Pre-Existing Conditions

Updated on May 16, 2025 • 9 min read

Seniors looking for life insurance with pre-existing conditions often have difficulty finding many traditional plans that accept them. They typically aren’t eligible for affordable rates for term life, universal life, and traditional whole life insurance. So what should seniors looking for life insurance with pre-existing conditions do?

That’s where Final Expense Benefits can help. As experts in the burial insurance market, our agents can help you find a policy that fits your health needs and budget.

Call us at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m. ET to learn more, or check our free online quoting tool for a personalized pricing estimate.

Can You Get Life Insurance with Pre-existing Conditions?

A pre-existing condition is a diagnosed medical condition present before applying for a life insurance policy. If you are a senior with a chronic health concern, you’re not alone. According to the U.S. National Health Service, nearly 25% of American seniors over 65 self-report fair or poor health status.

Seniors with pre-existing conditions can get life insurance, though eligibility mostly depends on the condition’s severity.

Seniors with well-managed or less severe conditions qualify for much better plans and rates than those with serious conditions.

Burial insurance is typically seniors’ best option for life insurance with pre-existing conditions. Also known as final expense insurance, burial insurance is a special type of whole life insurance offering simplified health requirements and coverage tailored to seniors’ needs.

Burial insurance is accessible even to seniors with serious pre-existing health conditions. There’s a good chance that most seniors with pre-existing conditions can find a burial insurance policy that works for them, with some policies offering guaranteed coverage, despite health concerns.

We can help you find burial insurance with pre-existing conditions like:

- Alzheimer’s & dementia

- Asthma and other controlled breathing conditions like mild COPD

- Cancer

- Disabilities not related to illness

- Epilepsy & managed seizures

- Heart conditions

- High blood pressure

- HIV / AIDS

- Living in assisted living / long-term care facilities

- Major stroke events

- Managed Type 1 or Type 2 diabetes

- Mental health issues like anxiety or depression

- Minor health complications from being overweight

- Obesity

- TIA stroke event (“mini stroke”)

- Tobacco use

- Terminal illnesses

Best Life Insurance with Pre-existing Conditions

Seniors with pre-existing conditions struggle to qualify for many types of life insurance, and if they do, some may not properly fit their needs. Here is an overview of the main categories of life insurance and how each may work for seniors with pre-existing conditions.

Term Life Insurance with Pre-existing Conditions

1

Term life insurance covers specified periods, used by young adults and other workers as income replacement in case of death. Benefit payouts for term life are large, and monthly premium rates can be low, but only if their strict health requirements are met.

Seniors typically have difficulty qualifying for term plans at low rates, plus they risk outliving their coverage.

A pre-existing condition complicates the term life application process. Seniors with pre-existing conditions don’t qualify for many term policies, even if conditions are well-managed. Rates can be unaffordably high if they do qualify. Term life insurance is a poor choice for seniors with pre-existing conditions for these reasons.

Traditional Whole Life Insurance with Pre-existing Conditions

2

Whole life insurance policies work great for seniors.They offer growing cash value, rates that are locked at the policy’s start, and coverage for life as long as premiums are paid, making them a reliable choice for many seniors.

However, traditional high-value whole life plans usually have large death benefits, and as a result, strict health requirements and high rates. Seniors looking to leave a significant amount of cash behind could use traditional whole life insurance, but rates could be unaffordably expensive with major pre-existing conditions.

Universal Life Insurance with Pre-existing Conditions

3

Universal life insurance is similar to whole life insurance, but with the upside of gaining value through investment performance. Instead of holding your paid premiums, insurers invest them, allowing death benefits to gain value.

However, this reliance on the stock market makes these policies unreliable for seniors. Seniors typically want their money to have more guarantees, and tying benefit payouts to investment performance could lead to them losing value. Universal life insurance can be an interesting choice for younger applicants, but we usually don’t recommend it to seniors looking to cover their end-of-life expenses.

Burial Insurance with Pre-existing Conditions

4

Also known as final expense insurance, burial is whole life insurance used by seniors to cover end-of-life expenses like funerals and pricey medical bills. Burial insurance is a great choice for life insurance for pre-existing conditions because it has low premium rates and relaxed underwriting requirements.

Burial insurance rates and health requirements favor seniors because most policies’ tax-free death benefits are limited to around $5,000 to $50,000.

This isn’t a big deal to seniors, who generally use life insurance to cover their funeral expenses, which average around $10,000.

When your application is received, your health status is used during the underwriting process to determine your plan category. Seniors in good health typically qualify for level benefits, which offer the best rates and benefits and have no waiting period. If health is less favorable, seniors may only qualify for plans with waiting periods like modified life insurance or guaranteed life insurance.

Burial insurance is a great choice for seniors with many well-managed pre-existing conditions, but what about more serious health concerns?

Guaranteed Life Insurance with Pre-existing Conditions

5

Guaranteed life insurance, burial insurance that disregards health status in underwriting, may be the only burial insurance that seniors with serious medical concerns may qualify for. Because underwriting is so relaxed, guaranteed plans have the highest rates out of any burial insurance policy. These plans also have a waiting period, usually two to three years.

If the policyholder dies during the waiting period, payouts may be reduced or replaced with a return of premiums. Less reliable providers like Colonial Penn and Lincoln Heritage primarily offer guaranteed plans, but they come at high costs, poor flexibility, and rigid waiting period requirements.

We typically only recommend seniors select guaranteed life insurance if it’s their only option. You may be surprised to see the health conditions you could have and still qualify for a policy with no wait. That’s why it’s important to have help from a brokerage like Final Expense Benefits. Our agents are experts in the life insurance market and will help you find a policy that fits your health and budget.

Contact Final Expense Benefits today for a no-obligation burial insurance consultation or check our online quoting tool for a free pricing estimate.

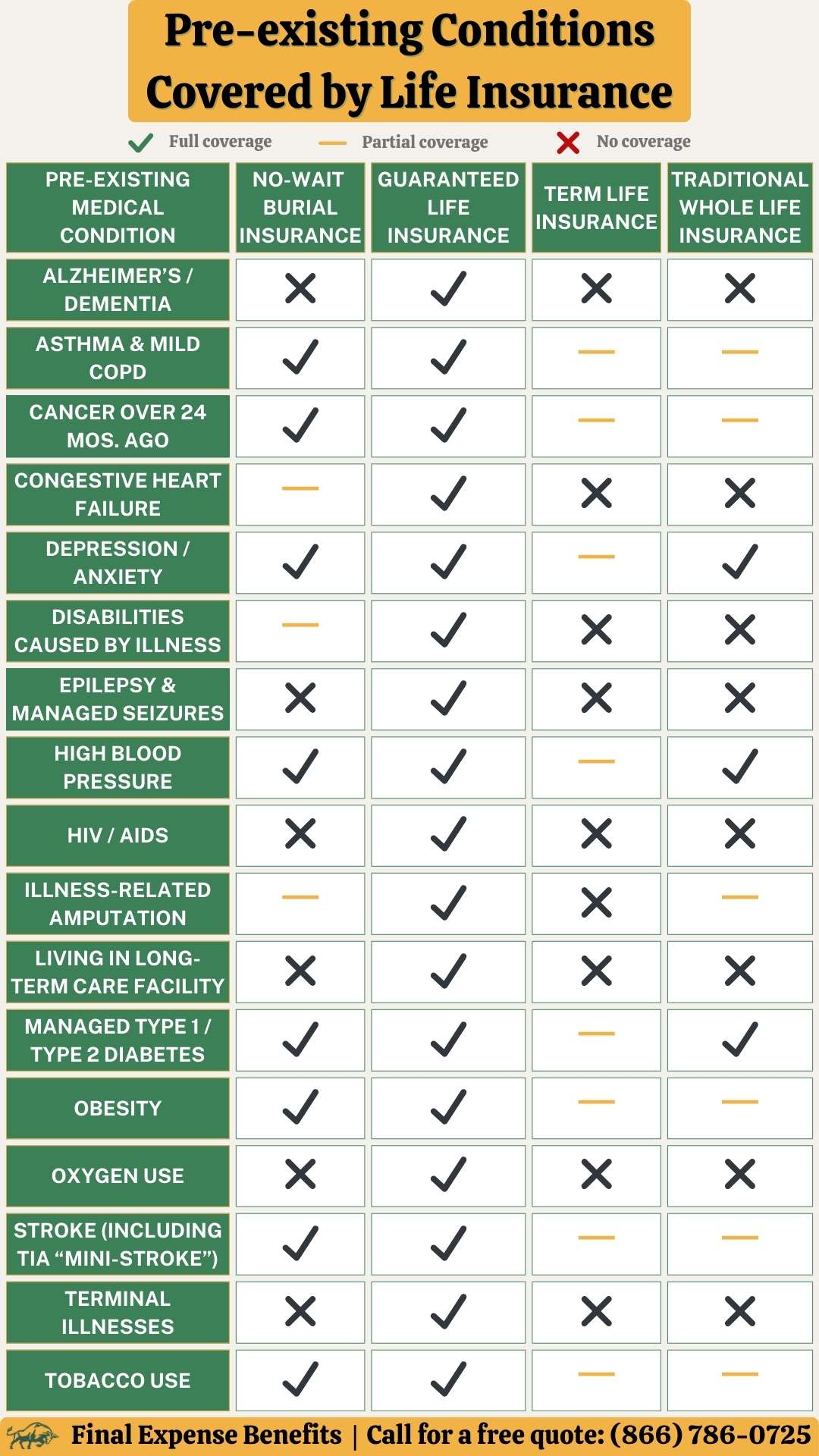

What Medical Conditions Disqualify You from Life Insurance?

While many pre-existing conditions would disqualify seniors from coverage under most life insurance, they wouldn’t be excluded from burial insurance.

Here is a chart with a list of health concerns that affect millions of seniors nationwide and what kinds of life insurance they could be eligible for:

If you’re looking for life insurance with pre-existing conditions, you should speak to a licensed agent from Final Expense Benefits to determine your eligibility. Everyone’s health is different, and we can help you find the best policy for your needs.

How Much Does Burial Insurance with Pre-existing Conditions Cost?

Life insurance rates vary based on your age, location, coverage value, tobacco use, and gender, but are largely decided by medical history. Pre-existing conditions heavily affect rates, though many seniors with minor health concerns are eligible for favorable level rates for burial insurance.

Below are charts depicting costs for level-benefit and guaranteed $10,000 benchmark final expense policies from some of our top providers for a non-smoking applicant with no specified health concerns. For an accurate, personalized estimate, check our free online quoting tool.

Level Benefit Life Insurance with Managed Pre-existing Conditions Rate Chart

1

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$51 |

$41 |

$73 |

$58 |

|

|

$32 |

$27 |

$47 |

$38 |

$79 |

$61 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

|

|

$37 |

$31 |

$48 |

$37 |

$86 |

$64 |

|

|

$34 |

$29 |

$50 |

$40 |

$82 |

$57 |

These rates are estimates only, calculated for $10,000 level-benefit burial insurance with a non-smoking applicant.

Guaranteed Life Insurance for Serious Pre-existing Conditions Rate Chart

2

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$49 |

$39 |

$78 |

$60 |

$122 |

$89 |

|

|

$44 |

$36 |

$68 |

$57 |

$120 |

$99 |

|

|

$61 |

$42 |

$74 |

$59 |

$115 |

$87 |

|

|

$71 |

$68 |

$102 |

$85 |

$142 |

$110 |

|

|

$59 |

$56 |

$85 |

$76 |

$142 |

$110 |

These rates are estimates only, calculated for $10,000 guaranteed burial insurance with a non-smoking applicant.

If you’re interested in these or any of our other final expense insurance options, contact Final Expense Benefits.

How Do Providers Determine Life Insurance Rates with Pre-existing Conditions?

3

Life insurance companies determine rates using your health history. They get this information through your application. Some providers require a medical examination, though many only need you to answer a health questionnaire.

This information is verified using third-party medical databases like the Medical Information Bureau. Underwriters then use your health information to assign your health classification, which determines your rates.

Health classification is largely determined by life expectancy. That’s why seniors might have difficulty qualifying for many types of policies.

Best Life Insurance Providers for Pre-existing Conditions

All our top-rated providers are great options for seniors seeking life insurance with pre-existing conditions, but some offer more lenient underwriting, lower rates, and other benefits. Here are our top picks:

Aetna Accendo

1

- Underwriting for pre-existing conditions:

Aetna Accendo’s underwriting practices are notably lenient, allowing seniors with a wide range of pre-existing conditions to qualify for no-wait and level policies. - Premium rates:

Aetna Accendo offers competitive rates for all health classes. - Additional benefits:

Customer and third-party rating services consistently give Aetna’s service and claims departments high scores.

American Amicable

2

- Underwriting for pre-existing conditions:

American Amicable has an easygoing underwriting process that allows you to qualify for their level-benefit plans with some pre-existing conditions. - Premium rates:

American Amicable has competitive rates for level-benefit and guaranteed plans, in line with some of the market’s cheapest final expense providers. - Additional benefits:

American Amicable offers a wide range of life insurance riders that allow you to customize your coverage at an extra cost.

Mutual of Omaha

3

- Underwriting for pre-existing conditions:

Like our other top-rated providers, Mutual of Omaha offers simplified underwriting that doesn’t penalize seniors with pre-existing conditions. - Premium rates:

Mutual of Omaha’s burial insurance rates are among the lowest in the entire market for level-benefit and guaranteed policies. - Additional benefits:

Customers consistently praise Mutual of Omaha’s claims processing and service departments.

If you’re interested in these or any of our top-rated burial insurance providers, call Final Expense Benefits today.

Final Thoughts

Seniors can find plenty of options for life insurance with pre-existing conditions on the burial insurance market. Burial insurance is the most reliable choice, but when you’re shopping for life insurance with pre-existing conditions, it’s important to have good help.

Rates and eligibility can get complex when medical concerns are involved, so you should contact an expert brokerage like Final Expense Benefits for assistance. Our agents know the market thoroughly and can help you find coverage that fits your health needs and budget.

To learn more, call us at (866) 786-0725 Monday through Friday, 9 a.m. to 5 p.m. ET, or check our free online quoting tool for a personalized pricing estimate.

FAQ

Can you get life insurance with pre-existing conditions?

Yes, though eligibility for term life, universal life, and traditional whole life insurance may be tricky. However, final expense insurance is a reliable option for seniors seeking life insurance with pre-existing conditions.

What medical conditions disqualify you from life insurance?

While many chronic conditions may disqualify you from types of life insurance with stricter underwriting practices like term life and high-value whole life plans, few conditions disqualify seniors from final expense insurance. You’d be surprised at the number of conditions that don’t disqualify seniors from immediate coverage, including diabetes, high blood pressure, and obesity.

What is final expense insurance?

Final expense insurance is whole life insurance designed to help seniors cover end-of-life expenses like funerals and burial plot costs. It’s typically smart to purchase a policy early to secure favorable rates.

What is guaranteed life insurance?

Guaranteed life insurance is a type of final expense insurance that disregards medical conditions in the application process. It does cost about 40% more than standard final expense plans, but it may be the only way for seniors with some serious pre-existing conditions to secure life insurance coverage.

How much does a funeral cost?

The average funeral costs around $10,000, which is why we use $10,000 as the basis for our final expense insurance quotes. Thankfully, final expense life insurance can be an affordable choice for seniors looking to cover their end-of-life expenses ahead of time.