Whole Life Insurance For Seniors: No Medical Exam Plans & More

Updated on June 9, 2025 • 8 min read

Planning for end-of-life expenses can be overwhelming, especially for seniors managing health conditions or living on a fixed income. Fortunately, whole life insurance provides steady, lifelong coverage to meet seniors’ needs. Whether you’re exploring options like burial insurance, final expense coverage, or simply looking for peace of mind, understanding your choices is the first step.

There are two main types of life insurance to consider: whole life and term life. Term life insurance offers protection for a set period, while whole life policies have lifetime coverage. Most seniors choose whole life insurance thanks to its reliability and affordability.

Final Expense Benefits can help you find quality whole life coverage at affordable prices. As experts in the life insurance market, our agents can help you find a great policy that fits your needs, even with pre-existing health concerns.

If you’re interested in these or any of our other life insurance options, call us at (866) 786-0725 to learn more. Be sure to check our free online quoting tool for personalized pricing estimates.

What is Whole Life Insurance?

Whole life insurance covers you for life, as long as monthly premiums are paid. It’s a popular, simple option for seniors who want simple, long-term protection.

In addition to a guaranteed death benefit payout, whole life plans build cash value over time. This means your policy protects your loved ones and acts as a financial asset you can use too. Whole life insurance rates are generally fixed for life, so your payments remain stable, which is especially important for seniors on a fixed income.

Most whole life policies are designed with seniors’ needs in mind, and payouts are typically used to cover funeral or cremation costs, burial plot bills, and other end-of-life expenses.

Whole Life Insurance Cash Value

Whole life insurance builds cash value by taking a portion of paid premiums and placing them into a savings account managed by the insurer. A major benefit to whole life policies, cash value grows at a guaranteed rate, offering tax-free savings within your policy. The longer you hold the policy, the more cash value it builds, which you can access in several ways.

You can borrow against the policy using a loan, withdraw a portion of the funds directly, or use the accumulated cash to pay your premiums. Some policyholders choose to use the cash value to purchase additional insurance coverage or an annuity for long-term payouts. This added flexibility makes whole life insurance not just a safety net for your family, but also a tool that you can utilize during your retirement years.

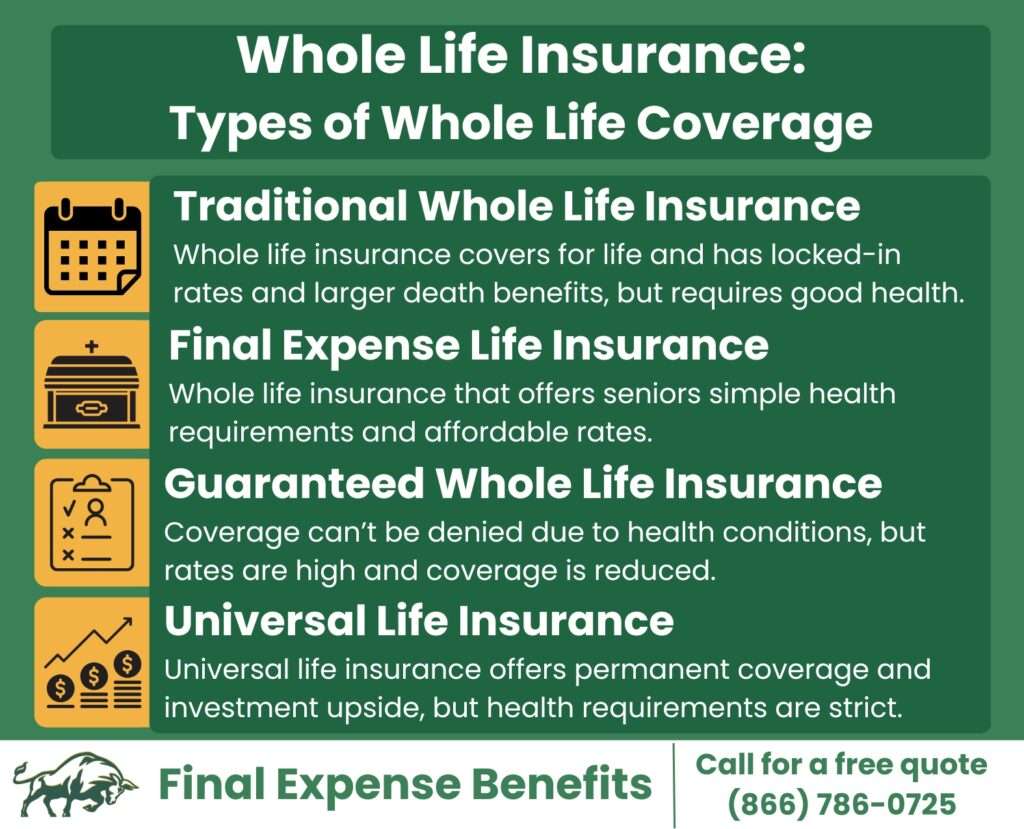

Types of Whole Life Insurance

Seniors can choose from a few permanent life insurance options, each designed to meet different needs and health profiles. Understanding the differences can help you choose the policy that best aligns with your personal and financial goals.

If you’d like to learn more about whole life policies, our expert agents are available at (866) 786-0725, or check our free online quoting tool for rate estimates.

1

Traditional Whole Life Insurance

Traditional whole life insurance is the most well-known type of permanent life coverage. These policies often offer high coverage amounts, usually ranging from $10,000 to $100,000, though some life insurance companies offer whole life policies covering over $1 million. Traditional whole life policies are best suited for people in relatively good health seeking long-term financial protection for their families or to provide an inheritance.

However, qualifying for traditional high-value whole life policies can be challenging for seniors, especially those with chronic or serious pre-existing health conditions. These policies typically involve full medical underwriting, which may include a physical exam, blood work, and detailed health questionnaires.

While the benefits are substantial, the application process can be more demanding. Some insurers now offer more accessible traditional policies with no medical exam, though with lower benefit amounts.

2

Whole Life Insurance with No Medical Exam

Seniors looking to avoid extensive medical underwriting processes can find permanent coverage with whole life policies with no medical exam. While many traditional whole life policies require medical exams, seniors willing to purchase policies with smaller benefit payouts can find whole life coverage without a medical exam with final expense insurance.

These plans usually offer faster approval and are easier to qualify for, making them popular choices for seniors.

3

Final Expense Whole Life Insurance

Final expense insurance, also known as burial insurance, is a specialized form of whole life coverage specifically designed for seniors. These policies cover the cost of funerals, cremation, medical bills, and other end-of-life expenses.

Unlike traditional life insurance policies, final expense insurance policies usually offer simplified underwriting, meaning approval is less dependent on health status, and applications have fewer health questions. Seniors in good health or with manageable health issues like diabetes or mild COPD have a better chance of approval for a final expense policy with no waiting period, which means coverage begins immediately after approval.

Most life insurance companies offer final expense insurance to seniors between 50 and 85, giving seniors an accessible way to provide their loved ones with quality benefits at affordable rates.

Final Expense Benefits specializes in final expense insurance. Call us today to learn more or check our free online quoting tool for a personalized estimate.

4

Guaranteed Whole Life Insurance

For seniors with more severe health conditions, guaranteed issue life insurance may be the best option. Guaranteed policies don’t ask medical questions and don’t require exams, but coverage is usually limited to $5,000 to $25,000. Rates hover around 25% to 40% higher than comparable simplified-issue final expense policies.

Guaranteed policies always have a waiting period, usually two to three years.

If the policyholder dies during this time, benefits may be reduced, replaced with a return of paid premiums, or paid in a modified payout structure.

Guaranteed issue insurance is ideal for seniors with serious health challenges such as:

Though rates are higher and benefits are lower, guaranteed issue policies ensure that everyone can receive some form of protection.

Term vs Whole Life Insurance

Differences between term and whole life policies are significant, especially for seniors. Term life insurance provides coverage for a set number of years, typically 10 to 30 years, and is generally used by young adults and other workers to replace lost income in the event of a premature death. These policies offer larger payouts at lower initial rates but come with an expiration date.

We don’t typically recommend that seniors purchase term life policies. Once the term ends, the policy expires, often at a time when it’s most needed. Renewing a term policy in your 70s or 80s can result in high rates or outright denial due to age or health status. Additionally, term life insurance medical requirements are stricter than whole life policies, making it difficult for seniors with health issues to qualify.

Whole life policies provide lifelong protection, fixed rates, and growing cash value, and are better for seniors than term life.

Universal vs Whole Life Insurance

While universal life insurance is another permanent policy type, it differs from whole life in some key ways. Universal life offers flexible premiums and death benefits tied to investment performance, which can appeal to younger or higher-income individuals looking to combine life insurance with long-term financial planning.

However, the flexibility of universal life comes with complexity.

Cash value is tied to market performance or interest rates, meaning the value of your policy could decrease if investments perform poorly. Seniors seeking financial stability and reliable returns will see this as a less appealing option.

Additionally, universal life insurance health restrictions are stricter than most whole life plans, and most seniors wouldn’t qualify due to age or health concerns. Whole life insurance is more predictable and accessible for seniors, especially those looking for straightforward, dependable coverage.

Whole Life Insurance Pros and Cons

Pros

- Tax-free benefit payouts

Payouts to beneficiaries are tax-free, ensuring they receive the policy’s full benefit. - Lifetime coverage

Unlike term life insurance, whole life policies last for life, as long as premiums are paid. - Tax-deferred cash value growth

Whole life cash value grows tax-deferred and can be accessed through withdrawals and loans or used to purchase an annuity, offering a financial safety net in retirement. - No medical exam policies available

Many whole life policies are available without needing to take a medical exam as part of the application process, making it easier for seniors to qualify and get coverage quickly.

Cons

- Health requirements

Some high-value traditional whole life policies may have strict health requirements, making eligibility tough for seniors. This is a major reason why we recommend more accessible final expense plans to seniors. - Higher premiums

Traditional whole life insurance rates can be higher than term life policies. Final expense insurance offers a good middle ground, providing good coverage at low rates. - Limited payouts

Whole life payouts are lower than those of term life. However, since most seniors use life insurance to help loved ones cover specific expenses like funerals, medical bills, or small debts, this limitation is usually not an issue.

Best Whole Life Insurance Companies

Choosing the right insurance company can make a big difference. We partner with over 20 of the top life insurance providers, but here are some top recommendations based on affordability, ease of approval, and customer service.

If you’re interested in these or any of our other top-quality life insurance partners, call Final Expense Benefits today or check our free online quoting tool.

- Mutual of Omaha

Mutual of Omaha is a trusted name in life insurance. They offer low final expense rates and have a strong customer service reputation. Their policies often include immediate coverage and are available without a medical exam.

- Aetna Accendo

Aetna Accendo, backed by CVS Health, provides reliable and affordable whole life policies tailored to seniors. They offer simplified underwriting, competitive rates, and a user-friendly application process and come with the added benefit of the Aetna Senior Products catalog. - SBLI

SBLI (Savings Bank Life Insurance) offers whole life policies with customizable options, including a wide variety of policy riders. Their customer service is well-rated, and they are a strong choice for seniors who want more flexibility and control over their policy.

Whole Life Insurance Companies We Recommend Seniors Avoid

Not all life insurance providers offer good value. Here are some providers we recommend seniors avoid:

- Colonial Penn

Colonial Penn’s highly advertised $9.95 plan offers limited benefits and poor value. Seniors may end up paying much more for minimal benefits. - Lincoln Heritage

Known for high rates, pushy sales representatives, and less-than-stellar customer reviews, Lincoln Heritage often does not deliver strong value. - AARP

While AARP is a recognized name, their whole life policies tend to have higher premiums and limited flexibility, making them a poor choice for many seniors.

Whole Life Insurance Rates

Costs for whole life policies vary based on several factors, including your age, gender, health, and the amount of coverage desired. Here’s a look at sample monthly rates from some of our top providers for a benchmark $10,000 final expense insurance policy using a non-smoking applicant with no pre-existing health issues:

| Company |

Male 50y/o |

Female 50y/o |

Male 60y/o |

Female 60y/o |

Male 70y/o |

Female 70y/o |

|---|---|---|---|---|---|---|

|

$34 |

$27 |

$50 |

$40 |

$70 |

$56 |

|

|

$31 |

$26 |

$43 |

$35 |

$71 |

$53 |

|

|

$31 |

$24 |

$44 |

$33 |

$75 |

$53 |

|

|

$34 |

$29 |

$45 |

$35 |

$79 |

$59 |

|

|

$33 |

$26 |

$48 |

$36 |

$82 |

$58 |

These figures are estimates only, based on a $10,000 final expense insurance policy with no applicant pre-existing conditions.

If you’re interested in these or any of our other top-quality life insurance partners, call Final Expense Benefits today or check our free online quoting tool.

Final Thoughts

Whole life insurance is a reliable and flexible choice for seniors who want permanent, simple lifelong protection. With options ranging from traditional high-value or no-exam policies to guaranteed and final expense insurance, whole life plans can meet your needs.

Whole life polices offer reliable coverage for what seniors need at affordable rates. Whether you’re in perfect health or dealing with a medical condition, there is likely a policy that fits your situation.

Final Expense Benefits can help you get a quality policy at a great price. Contact our agents to find a policy that fits your needs and budget. Call us Monday through Friday, 9 a.m. to 5 p.m. ET, or check our free online quoting tool for a personalized pricing estimate.

FAQ

What is whole life insurance?

Whole life is a type of life insurance that covers the policyholder for life, as long as premiums are paid.

Are whole life insurance premiums fixed?

Whole life insurance rates are fixed at the policy’s start, as long as the policy remains in effect. This is a major reason why it’s best to open a policy early, as rates are generally cheaper for younger applicants.

Are whole life insurance payouts taxable?

Life insurance payouts are rarely taxable, a major benefit to providing an inheritance or cash for final wishes through life insurance rather than a will payout.

Can whole life insurance be cashed out?

Whole life cash value can be withdrawn, and policies can be surrendered to insurers or to companies that buy active life insurance policies.

Can whole life insurance lapse?

Whole life policies can lapse if premiums aren’t paid.

How much is whole life insurance?

Whole life policy rates vary by benefit value, age, health status, gender, and other factors. Final expense insurance, a specialized, cheaper type of whole life policy, usually ranges from around $30 to $150 monthly for $10,000 to $40,000 of coverage.

Where can I find life insurance quotes for whole life policies?

Final Expense Benefits has a free online quoting tool for accurate, personalized whole life insurance quotes.

What is the difference between term and whole life insurance?

Term life insurance only covers for specified periods, usually 10 to 30 years, while whole life insurance covers for life, as long as premiums are paid. Health requirements are stricter for term life insurance, and death benefits are larger. Whole life is typically used by seniors to pay for end-of-life expenses like funerals, burial plots, and cremation, while term life is used by working families to cover loss of income.